This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook mhannan Fri, 03/18/2022 - 06:42 Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe.

CIO Perspectives Webinar, 2022 AssetAllocation Outlook. Markets have been unsteady at the start of 2022, driven by geopolitical tensions, inflation, and concerns about equity valuations. CIO Perspectives Webinar, 2022 AssetAllocation Outlook . Fri, 03/18/2022 - 06:42. Download transcript. Watch the Video.

A client said – I understand market valuations are expensive but it doesn’t seem that it will correct much. The fundamental driver of market peaks and exorbitant valuations is the perception that there is nothing to worry about – there is no investment risk. Certainly not if you are sticking to your assetallocation.

Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains. Reassess assetallocation. small-cap funds outperformed the Russell 2000® Index for the five years ending Sept.

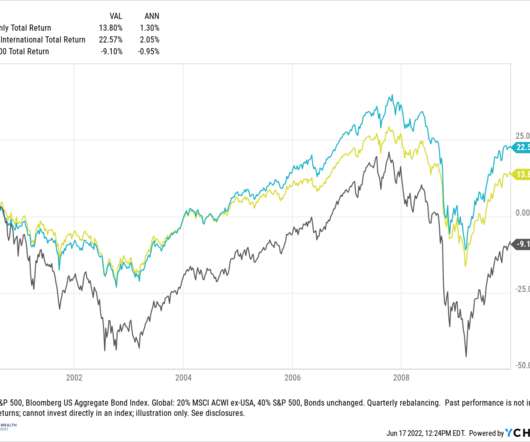

stocks that started in the early 2000s. Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% Since trying to time regime changes is very difficult in real time without the benefit of hindsight, there are reasons to consider allocating both U.S. equities to an assetallocation.

Valuation/Prices at which you invest (the difficult part) Now, if you do some thorough research and gain some insight to feel confident about better future growth prospects of any particular sector/theme you can still lose a significant amount of money or get poor returns even if your understanding was right. Let me share two examples: 1.

Instead, we got a shockingly fast collapse of a financial institution with over $200 billion in assets, which turned the market’s focus toward the stability of the banking system and what systemic risks banks might be facing. But valuations strongly favor value over growth. The S&P 600 small cap index has returned about 1.5%

And speaking of the.com implosion, like Microsoft via a case study where we, in previous strategies, we held Microsoft for a very long time, that’s where the valuation could help us in the.com bus. In 2000, right. And actually Ben Inker is the head of our assetallocation group. It was over 50 right? Yeah, yeah.

RITHOLTZ: 2000, right? CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. I don’t know. CHANCELLOR: Yes.

The LPL Research Strategic and Tactical AssetAllocation Committee is increasing its recommended interest rate exposure in its tactical allocation from underweight to neutral. Since 2000, the average increase in the 10-year yield during major moves higher is around 1.8%. Core vs Core Plus Bond Implementation.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

IBM loses to QCOM based on valuation. Sticking back to the balancing theme of quality businesses, great valuations, meshed with the reward of a dividend, you get Ford yielding 4.62% and Conoco only at 2.16% but trading for a bargain P/E of 7. We’re going to start backwards and share who wins the entire Small/Mid Cap region.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Risks in Bonds.

You, you wrote at the journal through the.com implosion as well as the whole runup to 2000 September 11th, the great financial Crisis. I did it in 2000, 2002. So, so the 20 years you spent at the Journal really is a fascinating couple of decades. What era of finance did you find the most intriguing as a journalist?

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. The Russell 2000 has 2000 out of the roughly 3,500 stocks available publicly traded.

On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. In short, every situation is different.

On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. In short, every situation is different.

Public-sector debt has expanded every year since 2000, hitting 100% of gross national product at the end of fiscal year 2014. Among our holdings in sectors backed by clear flows of revenues, we maintain an overweight in health care and transportation and remain focused on credit stability, valuations and opportunities for price gains.

So there’s been a big push for folks to get the appropriate level of assetallocation in a highly diversified, low cost way. DAVIS: Where international equities, because of valuations, probably 7% to 7.5%. RITHOLTZ: So let’s talk about that, because that gap in valuation has persisted for a long time.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Source: BLOOMBERG.

We believe that the investment return needed to achieve that objective should be the most important guidepost for a portfolio’s assetallocation. With traditional assets like stocks and bonds at high valuations, the implications for future returns of those assets may be underwhelming. Source: BLOOMBERG.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Optimists point out that every recession in the last 45 years was preceded by either a large financial bubble (technology stocks in 2000, U.S.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. Optimists point out that every recession in the last 45 years was preceded by either a large financial bubble (technology stocks in 2000, U.S.

Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” The Russell 2000® Index is a market-capitalization weighted equity index that provides exposure to the small-cap segment of the U.S. stock market.

Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” The Russell 2000® Index is a market-capitalization weighted equity index that provides exposure to the small-cap segment of the U.S. stock market.

This projection, however, assumes that participation, currently 63.0%, will continue its decline from its peak of 67.3%, reached in early 2000—a view that strikes many economists as overly conservative. Given the growth of the U.S. population and its age distribution, the labor force is estimated to grow at an annual rate of just 0.6%

This projection, however, assumes that participation, currently 63.0%, will continue its decline from its peak of 67.3%, reached in early 2000—a view that strikes many economists as overly conservative. Given the growth of the U.S. population and its age distribution, the labor force is estimated to grow at an annual rate of just 0.6%

” Dent called for “ the collapse of our lifetime ” – an 86 percent loss for the S&P 500; 86 percent on the Russell 2000; 92 percent on the Nasdaq – by June 2023. 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.”

Below is the price chart of HUL from Jan 2000 to Jan 2009. If you do not have requisite skill-set or don’t have time, then you should hire an investment adviser who has the expertise to evaluate fair investment valuation and has the experience, temperament and skill-set to alter assetallocation with changing market dynamics and cycles.

He wasn’t tactical assetallocator. I went out and bought a bunch of QQQ calls and spider calls just to play around and Russell 2000 calls, spiders did well, Russells did nothing. 00:42:14 So when Schwab acquired US Trust in 2000, it was only 10 months after I had joined us Trust Chuck. It wasn’t the case.

He launched his own firm right into the teeth of the collapse in ’09, which turned out to be quite a fortuitous time to launch an asset management shop. RITHOLTZ: That whole irrational exuberance era from ’96, from the speech to 2000, that could be the best four-year run in market history. So we do a lot of valuation work.

And that’s, that’s the predecessor to Amherst, which we bought in 2000 and had been running it since then. So think about 2003 home prices had gone up a lot from 2000. So mortgage position in 2000 were way more valuable in 2003 than they were when they originated because they weigh less credit risk. Anything else?

Outlook for 2017 | Balance in an Uncertain Time achen Fri, 02/03/2017 - 14:19 With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. Provide our assetallocation perspective as it stands at the beginning of 2017—also based on a longer-term view.

With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. In writing this report, we set out to accomplish two goals: Provide a window into our assetallocation philosophy and process, which emphasize a long-term view. Fri, 02/03/2017 - 14:19.

So I think the balance of those two and marrying those two together, and while we’re a large company, we’re around 200, 2000 people, again in, in over 2020 countries, it’s big enough where it requires, you know, certain process. The parent company handles all the asset liability management side of things.

And I think that helped fuel the smart beta boom of the 2000 tens. 00:21:21 [Speaker Changed] So this story came out that, oh, value is defensive because it has this valuation buffer to it 00:21:28 [Speaker Changed] In that one example. I can let you keep your stocks and bonds and I’m gonna add a 10% allocation on top.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content