This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Meaning, you do not get the 8-10% long-term gains without living through a significant number of market events, ranging from cyclical drawdowns to longer secular bear markets, and full-on crashes. 2000-13 : Secular bear market did not make new highs until March 2013 2018 : ~20% pullback as the economy slowed, FOMC hiked.

Who we are financially is very different than who we become in middle age or after retirement. During the 2000 crash, I had no 401k, and my wifes 403B was tiny. Our experiences mashed up with three different personalities and three different outlooks on money. The ones that should have mattered the most I was blas about.

At 50 though, you do need to have some context for how viable your idea of retirement is. That's the number you need to cover. We have a handful of annual expenses like property tax that amortize out to about $600/mo plus maybe another $1000-$2000/mo in discretionary and one-offs. If not, then something has to give.

Lending Tree posted a study showing how much people need saved to retire in/near 384 cities in the US. The averages you see from various reports are typically more akin to emergency funds than retirement funds. One note about their process is the effective tax rate for the Prescott Valley numbers would be well under 22%.

Marketwatch posted an advice type of column where a reader asked about his retirement readiness as he just got laid off and now would like to be done with working. They have a combined $350,000 in qualified retirement accounts and $200,000 in taxable accounts. This list starts the year at about $9000 including $2000 for property tax.

Schroders ) • The Exact Age When You Make Your Best Financial Decisions There’s a magic number for when your expertise and cognitive powers align. If you’re depending on income to fund your retirement, 5% rates are a blessing. 2000-2003 Dotcom implosion 6. Savings rates have rocketed and UK savers can earn over 5% on deposits.

The value of the S&P 500 index of stocks, where most of us hopefully have a good chunk of our retirement savings stashed into index funds, is up about fifty seven percent in just the past two years. Does this make it more vulnerable to a huge crash in the future, and will it affect my retirement? 4.3% – 5.3%

If you think about what Vanguard is all about, we sit there each and every day, figuring out how do we help people retire better, put their kids through college, afford that dream home? We were losing market share in the critical retirement, the 401(k) business. And everyone was talking about that ’99, 2000. BUCKLEY: Yeah.

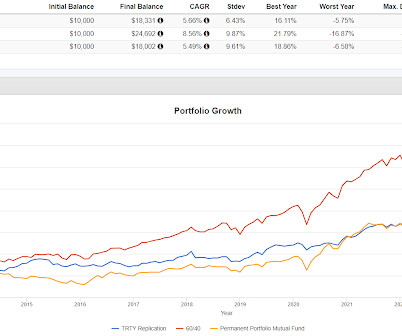

That period ending in May 2000 was relatively bad for PRPFX. I'd argue it all worked out in the end but imagine how you might handle being that far behind in early 2000. I don't know whether those weightings can vary but the numbers come off the home page for the fund.

As you would expect from an outstanding organization like Microsoft, it offers a very robust 401(k) to help employees save for retirement. Tax-Deferred Investment Growth : Dividends, Interest and Capital Gains are not taxed within your 401(k) until retirement allowing your investment returns to compound faster.

Forty years ago, the federal government lengthened Social Security’s full retirement age (FRA) from 65 to 67, and increased the delayed retirement credit. Since 1980 through 2014, workers with retirement plans that included a pension fell from 39% to 13%, a 200% decline. Is it the change we want?

00:27:54 [Speaker Changed] Let’s put some, some numbers, some mean on that bone. Well, when are you most likely to say, I need money out of my securities investment for life spending probably in retirement. And be sure and check out my new book, how Not to Invest the Bad Ideas, numbers, and Behavior that Destroys Wealth.

A couple of years ago, Wade Pfau drew some attention saying the 4% rule was no more, that t he new number should be 2.4%. Willie Delwichie Tweeted out that all of the S&P 500's gains since 2000 have come when the VIX was above 28.5 withdrawal rate, earning zero percent, your money would last for 41.6 and provided a chart.

After all, it was this overall life philosophy that earned me an early retirement 18 years ago, which provides all of the glorious freedom I enjoy now. How does that piece of wisdom apply to frugal living and enjoying a long life of early retirement? Running the Numbers: how ridiculously expensive is this car?

It’s one of the best strategies to supercharge your retirement savings, especially for early retirement. There's no time like the present to begin preparing for your retirement. This is always true when neither you nor your spouse are covered by an employer-sponsored retirement plan. Ads by Money.

Bloomberg had an article titled As Gen-X Nears Retirement, Many Fear They Can't Afford It-Now or Ever. There was an odd and I believe inaccurate emphasis on workplace retirement plans pivoting from defined benefit plans (pensions) to defined contribution plans (401k) starting around the turn of the century.

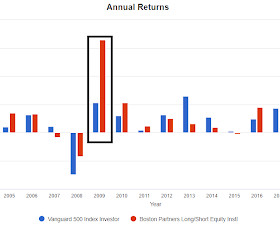

Based on those numbers alone which go back to 1999, yeah, I want to learn more. That is not a bad result but might be less than you'd think when looking at the CAGR numbers. In 2000, BPLSX outperformed by 69%, in 2001 it outperformed by 37%, 22% in 2002 and 46% in 2009. Here's the year by year though.

I was “The Man Who Retired at 30”, and it was so unusual that it would show up in news headlines all over the place. My story was a nine-year working career, and retirement at 30. This happens to be my personal definition of “retirement” , because the old definition of ceasing to work is obsolete.

To help you figure out what to do, here are 17 of the best strategies for investing $2000 to $3000. Best Ways to Invest $2000 to $3000: Final Thoughts. While investing $2,000 to $3,000 can help you make progress towards any number of financial goals, there are situations where you may need to access your money in the near term.

He has put together an amazing track record at Greenlight in the middle 2000 and tens. And since that happened, I don’t know, about four or five years ago, the fund has been putting up great numbers, outperforming doing really, really well. Then we stayed open until about 2000.

And generally speaking, we are sort of number one or number two in everything that we do, which, which again is a great privilege to work there from that perspective. So I have a recollection of the era following the.com ramp up and then the, the crash in 2000. 00:21:36 [Speaker Changed] Huh. Really, really interesting.

Why is the Russell 2000 worth 43% more in November than it was in February? I'd rather be doing literally anything else than having my retirement hinge on me being able to see the future." But people who sold are regretting that decision nine months later. The table below shows how far different U.S.

It laid out the threat and dug in with some numbers. There was mention of the potential pain for people who retire before they can start Medicare for having to find health insurance either through Healthcare.gov or some other way. Apparently, health insurance companies are asking for regulatory approval to increase premiums by 10-20%.

With the HSA contribution we save $2000 in taxes. I plugged in a number and was told I could max out with a $950 subsidy but I dialed it back (a feature of the Marketplace) to just $750. With the change to the Marketplace HSA we are paying $1175/mo so $4900 nominally more expensive for the year. Will it be worth it?

Let's say this person is 61, just retired, prefers to delay starting Social Security until age 70 and will take RMDs at 73 but could take IRA withdrawals earlier if the taxable account depletes. Talking generically, for someone for whom a depletion bucket makes sense, they are leaving their IRA alone for some number of years to keep growing.

SETHI: Well, everybody thought they were a genius including me in 1999, 2000. And they do that for 35 years tweaking numbers I go you won, you won the game. Number one, everybody has credit cards, everybody misunderstands how to use them, and there are actually some secret perks that people have no idea about. RITHOLTZ: Sure.

What would that do to people's retirement plans? If 2000 was fool me once and 2008 was fool me twice, what would 2019 be? The United States has experienced just six distinct bear markets since The Great Depression: 1929, 1937, 1969, 1973, 2000, and 2008. Entering these numbers was an uncomfortable experience.

I wasn’t that typical person that did a number of, you know, internships during the summer, had that …. BITTERLY MICHELL: … difficult situations for those who were retiring, right, and those …. RITHOLTZ: Whereas the — and the market when — essentially didn’t get above 2000 to like 2013 or so. RITHOLTZ: Yeah.

I have no idea if Blackrock has the correct numbers or not but it hits on what we talk about all the time here in terms of barbelling risk or volatility, depending on how you look at it, and understanding the role that various holdings offer to a portfolio. The tech sector isn't going to zero. Today, that fund is at $240. Bitcoin is all risk.

Let’s look at one tried-and-true way of multiplying your assets: retirement accounts. How to turn 10K into 100K through investing in retirement accounts. Although it may not sound glamorous, retirement accounts are a solid means of increasing your money. IRAs or Roth IRAs. without penalties. Similar to the 401(k) is a 403(b).

Even Mr. Money Mustache, as a person who retired 17 years ago, is still in this boat for the simple reason that my retirement income from dividends and hobby businesses is still greater than my annual living expenses (which still hover around $20,000 per year). (It’s Everything else is just silly noise.

Reg FD, which mandates that all publicly traded companies must disclose material information to all investors at the same time, did not exist until 2000! Perhaps people are putting a higher valuation on a shrinking number of public stocks. Retirement didn't exist. Interest rates are extremely low. Today there are just 4,500.

We believe that the current environment offers a number of strategic planning opportunities to improve your financial plan, enhance wealth transfers to heirs or charities, minimize the impact of income taxes and broadly help you advance your progress toward long-term goals. Deferral of required retirement plan distributions.

We believe that the current environment offers a number of strategic planning opportunities to improve your financial plan, enhance wealth transfers to heirs or charities, minimize the impact of income taxes and broadly help you advance your progress toward long-term goals. Deferral of required retirement plan distributions.

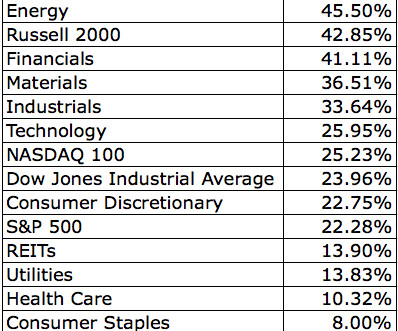

As I write this TBL, the S&P 500 is getting crushed and (using very rough numbers) is down 18 percent year-to-date. The Russell 2000 is off 21 percent. Based upon last week’s TBL , those hedge fund numbers sound high. Using very rough long-term return numbers (9.5% The Dow is down 8.5 I’ve had a few.

The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. The Russell 2000® Index measures the performance of the small-cap segment of the U.S.

The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. The Russell 2000® Index measures the performance of the small-cap segment of the U.S.

The Calmar Ratios are good for all of them but the kurtosis numbers are not which is a strike against relying on them as low vol, total bond replacements. So embedded in there is an expectation that stocks will look more like they did in the 2000's. Here's the year by year with 2022 highlighted. Next is looking at how they blend in.

One of these is matching your 401(k) contributions that you make towards your retirement savings. Which is where your employer contributes a certain amount towards your retirement account based on what you are already contributing each month. It’s not uncommon to retire electronics after a few years, even if they’re still functional.

Here in the US, our economy has grown by about 25% even after inflation, world economic output has grown even faster, and the number of people living in extreme poverty has been cut roughly in half. Yet even after adjusting for that inflation, the net output of our economy has grown by over twenty times – over 2000%”.

August 2000: SEC Rule 10b5-1. However, the 2000 rule also carved out an affirmative defense against this liability in the form of the 10b5-1 plan. To serve as a binding contract, the plan must be in writing and include: The number of shares to be bought or sold.

hour As you can see, the annual income remains constant at $50,000, but the hourly wage can vary greatly based on the number of hours worked. As mentioned, someone working 40 hours a week will spend over 2000 hours a year at work. . $50,000 ÷ 2,080 hours/year = $24.04/hour 50,000 ÷ 1,040 hours/year = $48.08/hour

Over my retirement I’ve seen it: written off as just a phenomenon of the lucky winners of the 2000 Tech Boom declared obsolete after the 2009 Financial Crisis dismissed as a temporary fluke of the spectacular stock market of the 2010s and explained away as a Covid-era side effect that came from the taste of freedom that people got from remote work.

It is not intended to look like equities, it is intended to differentiate so it probably won't keep up with equities or 60/40 unless there is run like the 2000's and of course even then there can be no guarantee. The six year numbers benefit from going down much less in 2022. The green rectangles hopefully isolate the effect.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content