This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Dividends come from earnings, and so those are sort of anchors to valuation. It’s where tech bubble in 2000 is the classic example. Barry Ritholtz : He had a very famous Wall Street Journal piece In, like, late night fourteenth 2000. Present value of future cash flows, any asset is present value of future cash flows.

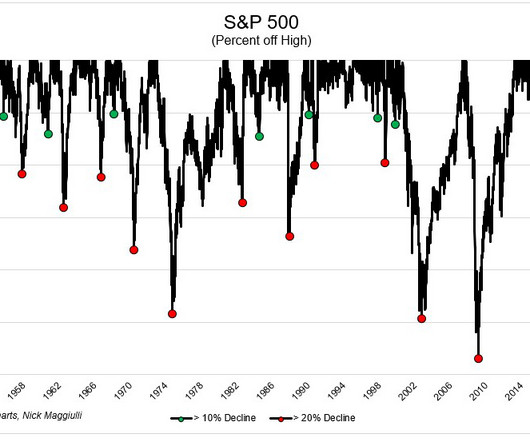

but the giveback off the highs was substantial: S&P 500 was down ~23%, Russell 2000 was off 27%, and the Nasdaq 100 came down 32%. But we won’t know how big a losing trade it might be until early 2024, when we see the updated valuations. Some folks who are more familiar with the numbers than I have suggested it will not be pretty.

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

And, and I kind of raised my hand and said, dad, uncle John, don’t you think it might be a better idea to look at it by the numbers? Valuations tended to crash and burn very, very cheap valuations tended to do well. The numbers are pretty bad. And they dismissed me. This is 1976. So I decided what’s a quant?

The Russell 2000, an index of 2,000 small-cap companies widely used as a benchmark for U.S. Tip adapted from Green Matters 9 Weekly Riddle… A palindrome is any word, phrase, or number that reads the same, either forward or backward. This trend was again on display last week. small-cap stocks, rose 4.50

What makes Graham so interesting is while everybody else in the world of private equity is focused on the analytics and crunching numbers and creating econometric models that will tell you where to invest, I think they’ve found a very different model that has been extremely successful for them, where the key focus is on talent.

Small-cap stocks continued their month-to-date surge as the Russell 2000 Index rose to an all-time high. Here’s what you’ll need to verify your identity: Social Security number Birthdate An Individual Taxpayer Identification Number if you have one instead of your SSN Your filing status Your prior tax return. Answer: NOON.

Barry Ritholtz : The the funny thing is, the behavioral aspect of mutual funds seems to have been when people finally learn about a manager who’s put up great numbers, by the time it makes to make makes it to Forbes, hey, most of that run is probably over and a little mean reversion is about to kick in. I did it in 2000, 2002.

Heather comes from with a fascinating background, having previously been in a number of other places, most notably Morningstar, and, and she has a very specific approach to investment management and thinking about stock selection. They do a number of things at Diamond Hill that many other investment shops don’t.

For example, if the house brings in $2000 per month ($24,000 each year) and the sale price is $240,000, the next investor is buying a business with a price-to-earnings ratio of 10, because 240k/24k=10. This year they came up with these numbers: Vanguards updated 10-year annualized return projections: Global bonds, non-U.S.:

From 1995 until the peak in March 2000, these four added $1.768 trillion in market cap. The combined four companies were trading at 100x earnings and 26x sales by early 2000. There were plenty of people warning about valuations during the late 90s. Unlike the late 90s, you can justify the valuations.

returns over the past 12 months—the second best in the history of the Russell 2000 ® Index—and on the heels of one of the worst quarters since inception in 1984 (-30.6% Exhibit 2: Nonearners as percentage weight and percentage of number of stocks in R2G Source: FactSet Research Systems; Russell Investment Group; Jefferies.

returns over the past 12 months—the second best in the history of the Russell 2000 ® Index—and on the heels of one of the worst quarters since inception in 1984 (-30.6% Exhibit 2: Nonearners as percentage weight and percentage of number of stocks in R2G. Exhibit 6: Dispersion in sector returns, Russell 2000 ® Index.

20,000 is not just a number; but happiness for many. Nifty 50 first hit 10,000 on July 26, 2017, and it took years to double that number. Amid all the noise surrounding geopolitical issues, global valuations, and FII selloff, the Nifty bulls might be feeling a bit clueless about their next moves. on July 20 of this year.

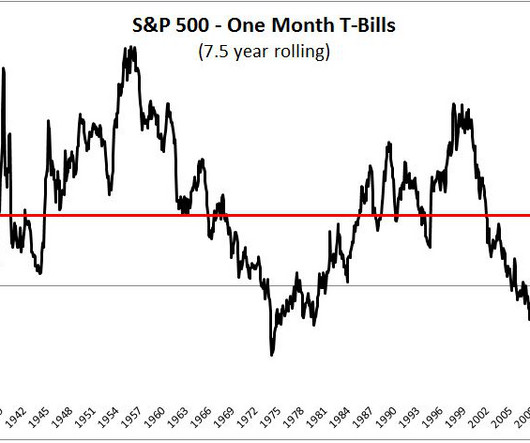

This range is determined by a number of factors, including but not limited to the business cycle, valuations, interest rates, inflation, and the collective mood of millions of investors. Since the top in March 2000, the S&P 500 has outperformed risk-free assets by just 2.7% a year, the largest spread over a 7.5

I had an amazing 99 in early 2000, and I had left a hedge fund, so I was probably one of the few people to leave a hedge fund and go to a larger institution in the middle of the tech bubble. The best example I always love to give is that Amazon’s last private round was at a $60 million post money valuation. It was April of 99.

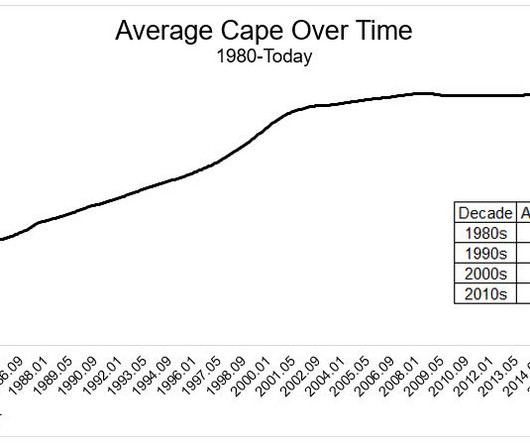

Whether you choose the CAPE ratio or a different valuation metric, they all say the same thing; Expensive markets leave investors with a smaller margin for error. Jumping in or out of stocks based on valuation can be extremely difficult, if not completely impossible. The more you pay, the less you get. Interest rates are extremely low.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. The Russell 2000 has 2000 out of the roughly 3,500 stocks available publicly traded.

In his latest piece, Waiting For The Last Dance , he writes: "I believe this event will be recorded as one of the great bubbles of financial history, right along with the South Sea bubble, 1929, and 2000." tech in 2000, and more or less everything in 2007. stocks are based on traditional valuation metrics, via Michael Cembalest.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Dot-com hangover/9-11 October 2000 December 2001 -16.5% Forward EPS is the ratio of projected earnings to number of outstanding shares of a company. by year-end. to nearly 3.9%

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. And then I developed this macro affinity starting in 2000, really? So that’s, that’s number one.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

And it worked out and had multiple job offers coming out of school from a number of different insurance companies. I had a number of relationships that I built up and had another job lined up in New York City. DAVIS: So when we think about how those teams are evaluated, it’s a three-year number. So how did you perform?

The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. The second, and what’s interesting about that period, is the fact that valuations actually peaked in 1961. MIAN: Valuations are ebb and flow. But number two is from a demographic standpoint.

Historical numbers should be taken with a grain of salt, but I do think it can help set baseline expectations. So, I had Nick Maggiulli run the numbers for me, and since 1950, the S&P 500 has declined 10% from its highs 25 times*. One in three stocks in the Russell 2000 have been cut in half. Or tech valuations.

Graham Foster] : 00:02:54 That was a number, that was number theory, pure number theory. And whether it’s all numbers or even numbers. Some people look at a casino as entertainment and hey, we’re gonna spend X dollars, pick a number, 500, 2000, whatever it is. Number one, longevity.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Many non-U.S. corporations.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. Concentration: Much of the U.S. Many non-U.S. corporations.

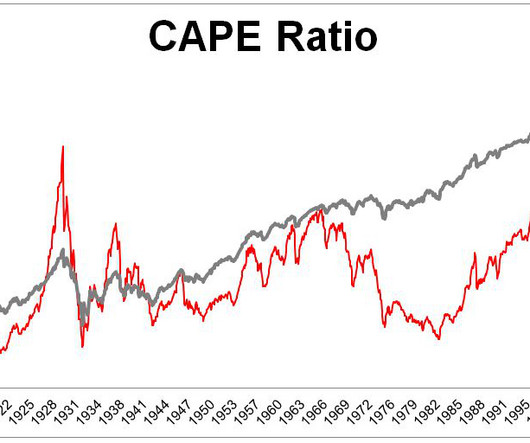

This visual tells a lot of stories, but for the purposes of this exercise, I want to focus on the two previous valuation spikes in red, which were followed by two stock market crashes in gray. If 2000 was fool me once and 2008 was fool me twice, what would 2019 be? Entering these numbers was an uncomfortable experience.

In other words, these investments (or “teams”) are ranked and seeded on a number of factors but one of the main drivers is how hot they recently performed within the past few months or recent year. IBM loses to QCOM based on valuation. We’re going to start backwards and share who wins the entire Small/Mid Cap region.

RITHOLTZ: 2000, right? CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. I don’t know. CHANCELLOR: Yes.

As I said there: This brings me to my conclusion: stock splits are a momentum effect, but it is larger when companies are still have a cheap valuation. Perhaps splits have no effect on stock performance — it is all momentum and valuation. In 2000, I had an email exchange with Kenneth Fisher (yes, the big guy of Fisher Investments).

Capital Market Magazine Capital Market is a fortnightly publication that analyses 2000 Companies and provides an in-depth analysis of the fundamental performance of the stocks, as well as their business operations. It generally covers the startup world concerning its business landscape, funding, and the valuation game.

However, this is actually a sustainable situation where market returns appear modest but are instead growing into their valuation. The health of the labor market is in focus with an increasing number of companies announcing intentions to reduce their workforce. To many, it may look like the market has stalled. What to Watch.

The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. The recent rise in dispersion may portend a better environment for active managers.

The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. The recent rise in dispersion may portend a better environment for active managers.

While new highs were set before bear markets in 1987, 2000, 2007, and 2020 in recent memory, the market has also made spectacular gains following new highs. We believe the first interest rate cut may come in May, unless inflation data over the next six weeks surprises to the downside or we get terrible payroll numbers.

By 2000 investors were rabid dogs ready to invest in anything that could be associated with the net. In the months to come those numbers will rocket higher as the media and CEOs push the technology as the next big thing. The first photo was shared on the internet a year later and the first webcams were introduced in 1991.

Nobody rang a bell in March of 2000 and told you the rules were about to change. All we have are numbers on a screen. Valuations don't matter. Of course valuations matter. Strong earnings can support high valuations. When something that worked for 30 years stops working, how long before we pick up on the shift?

Jim Top Tip’s “We're looking at a disruptive transformation from the animal-based protein to plant-based protein matter of fact, Bloomberg came back out came out and said by 2050 the valuation of the plant-based industry is going to be one $4.4 One, what goes into their body number two, is the very limited resources we have on planet Earth.

So there are a number of us heading in out of college into the BLS. And how do we think about them from a valuation perspective? You said earlier, valuations were historically high both stocks and bonds late 2021, right about now, what are we? MARTA NORTON, CHIEF INVESTMENT OFFICER, MORNINGSTAR INVESTMENT MANAGEMENT: Right.

Number of University Degrees in Science and Engineering 2000-2015 Source: National Science Board Science and Engineering Indicators A 2016 study from the World Economic Forum showed that China now produces more STEM graduates each year than any other country—4.7 and almost nine times the number of mobile payment users.

Number of University Degrees in Science and Engineering 2000-2015. The BBC reported in 2016 that China was building nearly one university per week , and projected that the number of 25-34 year old university graduates in China would quadruple by 2030. and almost nine times the number of mobile payment users.

When the current bull market inevitably turns, passive managers could be left holding stocks and sectors with poor fundamentals and inflated valuations. Being that we don't know when the bull market will "inevitably turn," why don't we look at some actual numbers. From 2000 to 2009, active outperformed passive nine out of 10 times."

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content