This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At 50 though, you do need to have some context for how viable your idea of retirement is. My reasoning is as it has always been, my income is levered to the ups and downs of the stock market, I don't ever want to retire, we have been living below our means for ages and now all the more so having just paid off our mortgage.

Rams) won in 2000 and the market dropped. Approaching retirement and want another opinion on where you stand? Financial coaching focuses on providing education and mentoring on the financial transition to retirement. Related Posts: Five Things to do During a Stock Market Correction Is a $100,000 Per Year Retirement Doable?

As a Retirement Income Certified Professional and a Life and Annuities Certified Professional, John advises clients on retirementplanning, investment planning, and risk management. His primary focus is to help people align their financial decisions with their values and truths to live enriching lives.

As you would expect from an outstanding organization like Microsoft, it offers a very robust 401(k) to help employees save for retirement. This article will discuss the key features of the Microsoft 401(k) plan, and after reading it, you should leave with a clear game plan of how to: Maximize the match (free money! )

Brian shares what he tells clients about investing and retirementplanning. For instance, Tom Brady, the greatest of all time, was 199 th pick when he was drafted in 2000. Similarly, investors who want to plan their own retirement might pick stocks based on emotions that they later regret.

The mass media in the United States tends to oversimplify the transition from the career phase to the retirement phase of our lives. Apparently walking into the sunset on a beach or through a meadow leads directly to a rocking chair on a front porch and that is retirement? The term “retirement” seems somewhat antiquated.

Lending Tree posted a study showing how much people need saved to retire in/near 384 cities in the US. The averages you see from various reports are typically more akin to emergency funds than retirement funds. The cheapest are was Johnstown, PA which requires $779,000. As a generalization, we collectively have not saved any money.

Marketwatch posted an advice type of column where a reader asked about his retirement readiness as he just got laid off and now would like to be done with working. They have a combined $350,000 in qualified retirement accounts and $200,000 in taxable accounts. This list starts the year at about $9000 including $2000 for property tax.

Somewhere around 1999 and 2000, television started to change. Before Netflix and streaming services pumped out shows as 8-hour binges, the following shows of the early 2000s began to set the groundwork for popular shows like Game of Thrones and Stranger Things. They turned television into a medium for long-form, poetic storytelling.

Let’s take a deep look at both plans, and particularly at where each stands out. It’s one of the best strategies to supercharge your retirement savings, especially for early retirement. There's no time like the present to begin preparing for your retirement. of providing tax-free income in retirement.

Retirementplanning focuses on the steps you need to take to achieve your desired retired life, such as saving and investing wisely, creating a budget, and considering your healthcare needs. However, it is also essential to be aware of the potential pitfalls and things to avoid during the retirementplanning process.

Articles Analysts have the second highest set of future earnings expectations for growth stocks since 2000. By Patrick O'Shaughnessy Expecting companies to sponsor retirementplans is like demanding that a dog dance; it may comply, but neither well nor happily.

Most of us of course lived through that from 2000 through to 2009. The S&P 500 hit 1500 in March 2000, then again in the fall of 2007 and then the third and final time in January, 2013. That's a long time for a broad based index to not make any progress.

If you put 3% into Ariba Networks into a diversified portfolio in 2000 or bought a house you could comfortably afford in 2007 then you had a setback but weren't blown up. I posted the above joke on Bluesky a few days ago. This person will get blown up if anything bad ever happens, absolutely destroyed.

While retirement should ideally be a time of relaxation and enjoyment, the financial implications of increasing expenses pose significant challenges for those in their golden years. Additionally, the study found that from 2000 to 2023, benefits under Social Security COLA increased by 78% or 3.4%

While retirement should ideally be a time of relaxation and enjoyment, the financial implications of increasing expenses pose significant challenges for those in their golden years. Additionally, the study found that from 2000 to 2023, benefits under Social Security COLA increased by 78% or 3.4%

Bloomberg had an article titled As Gen-X Nears Retirement, Many Fear They Can't Afford It-Now or Ever. There was an odd and I believe inaccurate emphasis on workplace retirementplans pivoting from defined benefit plans (pensions) to defined contribution plans (401k) starting around the turn of the century.

Bloomberg did a survey and found that Generation-X does not feel like it will be "financially prepared for retirement." Anyone closer to the younger edge of Gen-X could probably benefit by cutting expenses now, the impact of that could compound over the next 20+ years as they approach a normal retirement age.

If we're thinking about risk planning for the next ten years, I might wonder about a lost decade for US equities like we had from 2000-2010 and whether that might mean foreign equities rotate back into favor like they were back in 2000-2010. It's good to start thinking about these things ahead of time.

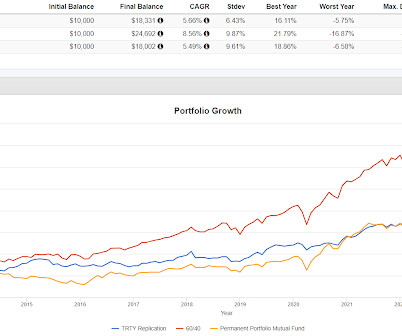

That period ending in May 2000 was relatively bad for PRPFX. I'd argue it all worked out in the end but imagine how you might handle being that far behind in early 2000. That would not have been easy of course there was no way to know how well gold was about to do to help PRPFX catch up over the next few years.

If you think about what Vanguard is all about, we sit there each and every day, figuring out how do we help people retire better, put their kids through college, afford that dream home? We were losing market share in the critical retirement, the 401(k) business. And everyone was talking about that ’99, 2000. RITHOLTZ: Really?

Forty years ago, the federal government lengthened Social Security’s full retirement age (FRA) from 65 to 67, and increased the delayed retirement credit. Since 1980 through 2014, workers with retirementplans that included a pension fell from 39% to 13%, a 200% decline. Is it the change we want?

There are less than 2000 people in India who have qualified CFP. RetirementPlanning Course – Retirementplanning is gaining huge popularity among Indians. High disposable incomes and high-spending lifestyles have been encouraging Indians to plan for their retirement to ensure they continue to live their dreams.

Let's say this person is 61, just retired, prefers to delay starting Social Security until age 70 and will take RMDs at 73 but could take IRA withdrawals earlier if the taxable account depletes. But what retirementplan doesn't need some level of resilience in the face of some sort of adverse market sequence?

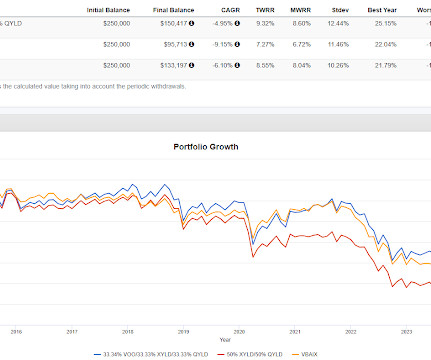

We've looked at these a couple of times over the years, back in the 2000's I accessed the space through a closed end fund that had a high yield, higher than what the space typically offers, thanks to the leverage inherent in the closed end universe.

If you've saved close to enough by the time you retire, so like you thought you needed $850,000 and you're at $810,00, then a conservative approach would be to manage the difference between 3% and 4% or using $850,000 you are managing for $8500, the difference between $25,500 and $34,000. and provided a chart. like maybe less than a month.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

What would that do to people's retirementplans? If 2000 was fool me once and 2008 was fool me twice, what would 2019 be? The United States has experienced just six distinct bear markets since The Great Depression: 1929, 1937, 1969, 1973, 2000, and 2008. What would happen if stocks crash?

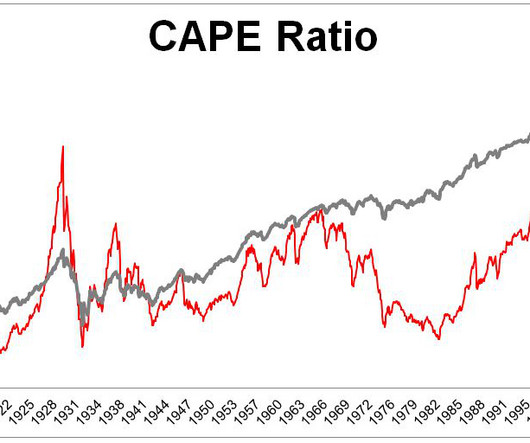

while the average CAPE since the year 2000 has been over 25." With millions of Americans shoveling money into their retirementplans every month, there is a much greater demand for stocks than their was in the first half of the twentieth century. The average CAPE for the decade immediately following WWII was 12.4,

Barron's dusted off the retirement bucket playbook in an article while also arguing that a 5% withdrawal rate in retirement can now be considered safe versus the more common 4%. I might argue longer than two years considering the bear market from 2000 took 30 months to find a bottom. Always read the comments.

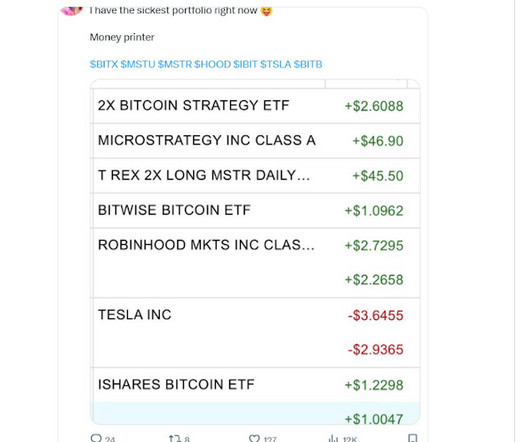

Unlike the decade long round trip to nowhere for equities in the 2000's, bond ETFs don't necessarily need to go back to where they were. I've seen a couple of references to a big, really big, round trip in price for fixed income ETFs. That image is from Stocktwits. Notice the CAGRs.

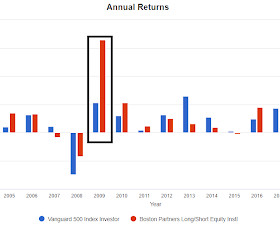

In 2000, BPLSX outperformed by 69%, in 2001 it outperformed by 37%, 22% in 2002 and 46% in 2009. That is not a bad result but might be less than you'd think when looking at the CAGR numbers. I outlined the four years that account for just about all of the long term outperformance.

With the HSA contribution we save $2000 in taxes. A follow up to a point I made a while back on this is how cheap Marketplace insurance might be for people close to my age, 50's through to mid-60's, who find themselves out of work unexpectedly possibly forced to retire. Will it be worth it?

Part G Medicare, the one I believe to be the most robust supplemental plan currently costs an average of $1517/yr with projections of 10+% increases over the next few years. Even $21,000 seems crazy high but getting close to $2000/mo for health insurance in your early 60's is about where the market is.

In the 80's and 90's domestic outperformed, for most of the 2000's foreign outperformed and we are now in a 12 or 13 year run of domestic outperforming. In the 2000's I was much heavier in foreign than I have been for the last 10 or 12 years.

This happens every so often, probably does not indicate a healthy market but as we saw in 2020, it can resolve by the rest of the market catching up, it doesn't have to result in a 2000-era bubble popping. I have no idea if the rest of the market will catch up or if this one will end very badly, we have no control over that.

A little exposure to something like TLH, that's merely unfortunate kind of like the person who put a little into Cisco Systems (CSCO) above $70 back in 2000 and still holds it today at $43. Small allocations don't become impediments to portfolio growth, simply they are laggards.

From the high in 2000 it took until 2019 to double. Or you could look at the 2007 high which was within a few points of the 2000 high and say it took 12 years to double. From the high in 1968, it took 18 years to double which is a very long time of course.

Back on October 20th, Willie Delwiche Tweeted about research he did showing that since 2000, all the net gains for the S&P 500 came with the VIX above 28.5. We'll see whether "sophisticated" leads to better nominal returns or better risk adjusted returns but these resonate.

The Technology Sector SPDR (XLK) peaked out in $60 in 2000 and it bottomed in 2002 at $12. Marketwatch had a useful summary of a paper from Emory University that concludes the optimal retirement portfolio allocation is 33% domestic stocks and 67% foreign stocks, so no bonds. The tech sector isn't going to zero. Bitcoin is all risk.

QQQY (personal holding that I am test driving) was down much less than the S&P 500 and the Invesco QQQ Trust, JEPY was down less than the S&P 500 and IWMY was down less than it's corresponding underlying iShares Russell 2000 ETF (IWM). As a first test maybe, these ETFs did just fine. world is a good first impression.

Looking back on Brown Advisory’s results in 1999 and early 2000, just before the technology bubble popped, our equity portfolios lagged the market, reflecting our discomfort with many of the high-flying “dot-com” stocks of the day. The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe.

Looking back on Brown Advisory’s results in 1999 and early 2000, just before the technology bubble popped, our equity portfolios lagged the market, reflecting our discomfort with many of the high-flying “dot-com” stocks of the day. The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content