This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Dividends come from earnings, and so those are sort of anchors to valuation. It’s where tech bubble in 2000 is the classic example. Barry Ritholtz : He had a very famous Wall Street Journal piece In, like, late night fourteenth 2000. Present value of future cash flows, any asset is present value of future cash flows.

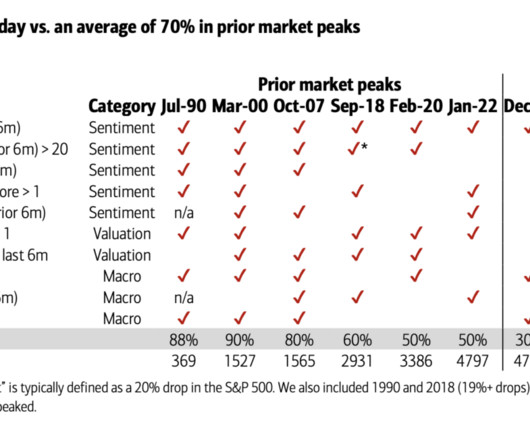

She observes it is less about the things investors tend to focus on — “technical analysis, geopolitics, behavioral finance and even skirt hemline trends” — and more about specific measures she tracks in sentiment, valuation, macro-economic areas. The table above shows the major market peaks going back to 1990.

Nvidia is not the first giant tech company to trade at a rich valuation. Irrelevant Investor ) see also “No matter how you cut it, you’ve got to own Cisco” (2000) 23 years ago, Fortune magazine’s cover story about networking gear maker Cisco was published. We can’t compare things to the future, so we look to the past.

This has made finding fundamentally sound stocks trading at reasonable valuations much easier in the small-cap space than in the S&P 500. Here are the current top 10 Russell 2000 stocks.

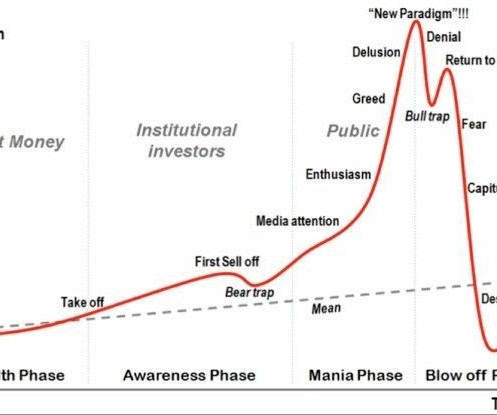

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

but the giveback off the highs was substantial: S&P 500 was down ~23%, Russell 2000 was off 27%, and the Nasdaq 100 came down 32%. But we won’t know how big a losing trade it might be until early 2024, when we see the updated valuations. Blame whatever you want – Too far, too fast? End of ZIRP? Too rapid rate increases? –

After lagging the S&P 500 for much of 2024, the Russell 2000 small cap index has staged an impressive rally in recent weeks. As smaller companies catch up to their large cap counterparts, investors may be wondering which Russell 2000 stocks look most attractive. over 10 years Manageable debt levels Projected 10-year return of 16.8%

from the most speculative level of valuations in U.S. history – exceeding even the 1929 and 2000 extremes, based on the valuation measures we find best-correlated with actual subsequent market returns in cycles across history. As of Friday, December 16, the S&P 500 Index is down -19.7%

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

No matter what metric you looked at, the peak valuations for growth stocks in mid-2021 were extreme. This is a chart of the valuation of the most expensive decile of our investable universe using the Price/Sales ratio. But even after that decline, the overall valuation remains about 30% above its average for the full period.

The economy, inflation, interest rates and market valuations drive the key questions facing advisors. Does the tech stock landscape mirror the boom of 1996 or the bust of 2000? What will be the impact of Meta's inaugural dividend payment? Is now the time to increase allocations to international Markets?

With our most reliable valuation measures more extreme than both the 1929 and 2000 market peaks, we continue to believe that the stock market is tracing out the extended peak of the third great speculative bubble in U.S.

Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. While some of that outperformance was due to improving fundamentals and earnings, most of it the returns came from the valuation investors assigned to these stocks. Source: [link].

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

On December 6, the S&P 500 set the most extreme level of valuations on record, exceeding both the 1929 and 2000 market peaks on measures that we find best-correlated with actual, subsequent 10-12 year S&P 500 total returns across a century of market cycles.

The Russell 2000® Index (which tracks small-cap stock performance) was up only 0.44%. Are the Russell 2000’s weak returns a sign of slowing economic growth, or is the recent underperformance of small caps reflecting investor sentiment about current market opportunities? times earnings over the same period.

A client said – I understand market valuations are expensive but it doesn’t seem that it will correct much. The fundamental driver of market peaks and exorbitant valuations is the perception that there is nothing to worry about – there is no investment risk. There is nothing to worry about.

The Russell 2000 has declined 32% from its November 2021 high through June 2022—worse than the S&P 500’s 24% drop. And the Russell 2000 is now up 14.3% With the Fed swiftly raising rates and the slowing of economic growth, small-cap stocks have gotten pummeled. But that could be about to change, portends an article in Barron’s.

The Russell 2000, an index of 2,000 small-cap companies widely used as a benchmark for U.S. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors. small-cap stocks, rose 4.50

Investors may find opportunities at more reasonable valuations when comparing different asset classes across the market. For example, small caps have lagged the NASDAQ 100 this year, with the Russell 2000® Index of small-cap stocks down nearly 10% year.

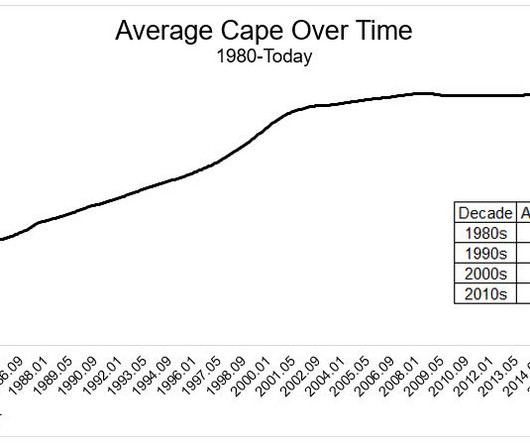

In it, he discusses the efficacy of using valuations, specifically the CAPE ratio, to help time the market. One thing Asness addresses is the valuation drift upward which U.S. while the average CAPE since the year 2000 has been over 25." He then addresses the oft-heard argument that this valuation drift is a secular change.

From 1995 until the peak in March 2000, these four added $1.768 trillion in market cap. The combined four companies were trading at 100x earnings and 26x sales by early 2000. There were plenty of people warning about valuations during the late 90s. Unlike the late 90s, you can justify the valuations.

In an interview with Bloomberg, Villalon said that the models used by AQR indicate that equities in emerging markets have the cheapest relative valuations since the year 2000, and will beat U.S. AQR takes “a valuations-based perspective,” Villalon says, so while the firm can’t predict “if the U.S. equities for the next 10 years.

returns over the past 12 months—the second best in the history of the Russell 2000 ® Index—and on the heels of one of the worst quarters since inception in 1984 (-30.6% The strong price appreciation has resulted in a commensurate rise in valuations and a tsunami of new deal issuance in these areas. GICS Sectors. The Smallest Lead.

returns over the past 12 months—the second best in the history of the Russell 2000 ® Index—and on the heels of one of the worst quarters since inception in 1984 (-30.6% The strong price appreciation has resulted in a commensurate rise in valuations and a tsunami of new deal issuance in these areas. Small Caps: The Big Picture.

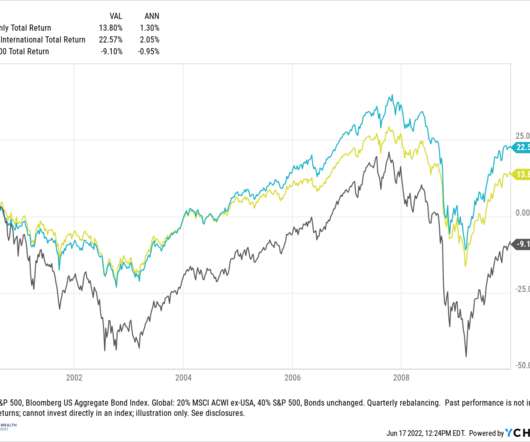

stocks that started in the early 2000s. Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% From 2000 to the end of 2009, the global allocation would have outperformed by nearly 8.8% Valuations. international stocks look much more attractive on a valuation standpoint. in total.².

Less than two years later, Palo Alto Networks purchased the company for $200 million—a more than 25-fold surge in valuation. In November 2015, Square, a San Francisco-based creator of mobile payment technology, went public at $9 per share and immediately rocketed 45% to a valuation of more than $4 billion. Not necessarily.

The index’s loss of 6.24% in 2018 was paltry compared to its 38% loss in 2008 and three consecutive double-digit down years of 2000-2002. This helps to illustrate the fact that market corrections are common over most periods of time and should be viewed as the market resetting stock valuations back to a more fundamental level.

The problem is the level of valuations. Why is that so? Because it has been a popular narrative for quite some time. But, what’s the problem with investing in popular narratives? Popular investment sectors or themes gain momentum as more investors join, driving prices much higher than the worth of the underlying assets.

And speaking of the.com implosion, like Microsoft via a case study where we, in previous strategies, we held Microsoft for a very long time, that’s where the valuation could help us in the.com bus. In 2000, right. So Microsoft now is on 30 times earnings. It was over 50 right? Yeah, yeah. It’s kinda our basic philosophy.

In his latest piece, Waiting For The Last Dance , he writes: "I believe this event will be recorded as one of the great bubbles of financial history, right along with the South Sea bubble, 1929, and 2000." tech in 2000, and more or less everything in 2007. stocks are based on traditional valuation metrics, via Michael Cembalest.

Whether you choose the CAPE ratio or a different valuation metric, they all say the same thing; Expensive markets leave investors with a smaller margin for error. Jumping in or out of stocks based on valuation can be extremely difficult, if not completely impossible. The more you pay, the less you get. Interest rates are extremely low.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations. Possible Signs.

But there’s always gotta be some element of the valuation really being compelling. But even in the book I wrote in 2014, you could see that the focus on competitive advantage can never be absolute, you always have to take valuation into consideration. But maybe second to valuation as a primary consideration.

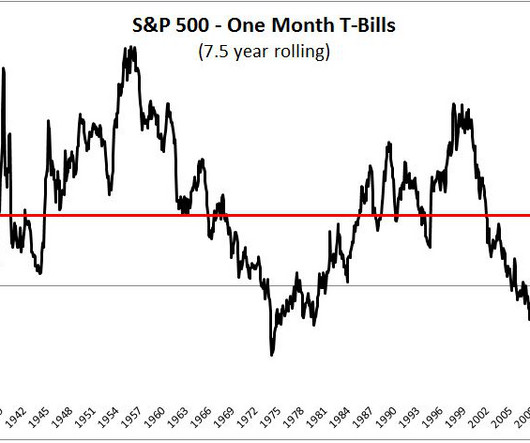

This range is determined by a number of factors, including but not limited to the business cycle, valuations, interest rates, inflation, and the collective mood of millions of investors. Since the top in March 2000, the S&P 500 has outperformed risk-free assets by just 2.7% a year, the largest spread over a 7.5

of the S&P 500 Are worth as much as the smallest 369 companies in the index Are three times as large as the entire Russell 2000 And yet, even with this massive growth, in terms of overall returns, the tech bubble makes this period look quaint by comparison. These 5 stocks now: Represent 23.3%

Small-cap stocks continued their month-to-date surge as the Russell 2000 Index rose to an all-time high. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

We also take a tour of the current major areas of innovation they are looking at including artificial intelligence, robotics, autonomous vehicles, fintech and the metaverse and discuss the opportunities they see in each of them.

We also take a tour of the current major areas of innovation they are looking at including artificial intelligence, robotics, autonomous vehicles, fintech and the metaverse and discuss the opportunities they see in each of them.

Valuation/Prices at which you invest (the difficult part) Now, if you do some thorough research and gain some insight to feel confident about better future growth prospects of any particular sector/theme you can still lose a significant amount of money or get poor returns even if your understanding was right. Let me share two examples: 1.

Needless to say, when stocks are going straight up, some funky things happen to valuations. In a Howard Marks memo from January 2, 2000, he wrote "It is reported that the average new issue of 1999, which on average is probably about six months old, is selling roughly 160% above its issue price. That is a divergence.

If we zoomed out to the top in 2000, then the S&P 500 went sideways for 14 years, and the bull market breakout didn't happen until 2013. I mean, given recent returns and where valuations and interest rates are, things can't possibly get any better, can they? What about if we measured it from the top in 2000?

For example, we found opportunity in small-cap stocks during their 2016 rally because of their relatively low valuations and limited vulnerability to flagging global economic growth. Indeed, with such a change in allocation, total asset valuation in any given year may swing in terms of standard deviation by as much as 17%.

Defining Free Cash Flow Yield Free cash flow yield is a valuation metric that compares a company’s free cash flow per share to its market price per share. A higher FCF yield generally indicates that a company is generating more cash relative to its valuation, potentially making it a more attractive investment.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content