This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Since 2002, overall carloads on Union Pacific’s network have declined by a bit less than 1% per year, but Union Pacific’s revenues per car have increased 4% per year. railroads have vastly outperformed the broader stock market over the last five-, ten-, and twenty-year periods?

Barry Ritholtz : The the funny thing is, the behavioral aspect of mutual funds seems to have been when people finally learn about a manager who’s put up great numbers, by the time it makes to make makes it to Forbes, hey, most of that run is probably over and a little mean reversion is about to kick in. I did it in 2000, 2002.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: Yes. And that’s problematic. RITHOLTZ: Right.

Felix outlines a number of ways to combat the cost of pessimism, including checking your investments less frequently and finding ways to automate your investing contributions, among others. Over the last 25 years, we have seen four bear markets (1999-2002, 2008-2009, 2020, 2022) and numerous market corrections (10% losses).

They have a number of businesses that they’ve taken over through the debt side of the equation. But that valuation, to be able to come up with the valuation, to be then able to work in a restructuring process, bankruptcy process, and say, Hey, I think at the end of this, we are buying debt at 50 cents.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations.

We remain highly dubious of price-to-earnings ratios as a proxy for value given earnings can be distorted by “creative” accounting and the measure embeds a range of factors into a single number. By this valuation method, the portfolio cashflow duration is in the 16 to 17-years range. We inherently prefer actual cash flow.

And then in ‘94 and ’98, you know, all had a different stream to 2002. And like I say, that’s part of why it’s translated to a number of people coming to BlackRock and be with me today. RIEDER: So I had known Larry Fink and Rob Caputo, our CEO and president, for a number of years. So yeah, man, that was the idea.

They run long short across each of these, and they’ve put up some pretty impressive numbers over the past couple of years. And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. It’s beta neutral, market neutral.

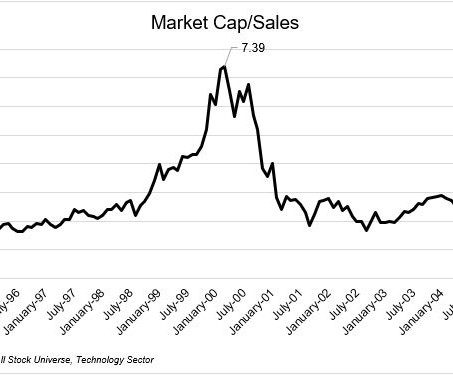

Stocks flooded the market, and valuations stretched into the stratosphere. The number of tech stocks exploded from under 300 at the beginning of 1995 to 952 at the bubble's peak. Amazon continued to grow between the peak in 99 through the end of 2002. Sound familiar? Their quarterly revenue growth averaged a whopping 48%!

To give you a fun story, we launched Protégé Partners in 2002. Or at least the top, pick a number, 30, 40%. And in 2002, the bucket of the largest hedge funds was those north of $1 billion. SEIDES: Before 2002, there were no capacity issues with whoever you thought the best hedge funds were. Less, 20, 30%? RITHOLTZ: Sure.

Or are the steel tariffs of 2002 a better indicator of what we should expect—an orderly, low-impact process resolved by the WTO in fairly short order? At a company-specific level, a number of firms have already sold off on fears of tariff impact. The media is focusing a lot of attention on tariffs proposed by the U.S.,

Or are the steel tariffs of 2002 a better indicator of what we should expect—an orderly, low-impact process resolved by the WTO in fairly short order? At a company-specific level, a number of firms have already sold off on fears of tariff impact. The media is focusing a lot of attention on tariffs proposed by the U.S.,

True to form, she got back to me within just a few minutes with these thoughts: MMM: How should potential retirees think of the recent crash in valuation – has it really pushed out their retirement date, or not? It’d be like retiring at the bottom of 2009 with still-decent numbers.

And because my mother and grandmother were looking at these trying to figure out what was going on, I was curious about the sea of numbers. And 00:28:03 [Speaker Changed] That’s an amazing number. 00:44:11 [Speaker Changed] Kathy would may have her own valuation, so, but I can’t replicate it myself.

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. And so, that didn’t happen until 2002. I mean, you know, this is probably 2002. Valuations go up and you saw it, of course, in the late ‘90s, in the tech sector.

We believe that the current environment offers a number of strategic planning opportunities to improve your financial plan, enhance wealth transfers to heirs or charities, minimize the impact of income taxes and broadly help you advance your progress toward long-term goals. We are working to help you take those steps forward.

We believe that the current environment offers a number of strategic planning opportunities to improve your financial plan, enhance wealth transfers to heirs or charities, minimize the impact of income taxes and broadly help you advance your progress toward long-term goals. We are working to help you take those steps forward.

The transcript from this week’s, MiB: Aswath Damodaran: Valuations, Narratives & Academia , is below. You’re known as the dean of valuation. He said, oh, dean of valuation, it’s easier to say. So let’s start with the question, what led you to focus on valuation? RITHOLTZ: Right. And I said, why?

So it’s got this math angle where it, you know, it’s all numbers, but then there’s this behavioral angle and psychological angle where, you know, it’s, it’s kind of a fun problem to tackle. It’s kind of a silly number, but people are going to think you’re smart or dumb based on that number.

I said a number of dis drive companies, pc, I mean, we did actually invest in Compact during that period. They’re a number of technologists that are now interested in healthcare. And where we’ve made the least number of investments, the fewest number of investments is in hospital systems because Epic owned it.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content