This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This means that the expansion of valuation multiples, like price-to-earnings (P/E), has played a big role.2 For current valuations to be justified for the Mag 7 and large growth stocks more broadly, very large earnings growth will have to continue. 3 So, as investors, what can we do about it within our portfolios?

Coming into 2022, the 60/40 stock/bond portfolio had been a stalwart strategy for your balanced investor. Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. at the start of the year) things are looking brighter for this simple portfolio. Source: [link].

There are about 13 different portfolio managers each focused on a different sub-sector. And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. Since then, it’s grown to about $7 billion. Your next stop is Millennium.

The index’s loss of 6.24% in 2018 was paltry compared to its 38% loss in 2008 and three consecutive double-digit down years of 2000-2002. This helps to illustrate the fact that market corrections are common over most periods of time and should be viewed as the market resetting stock valuations back to a more fundamental level.

You would offer three of their stock picks where they were probably touting stocks they wanted to unload from their portfolio. 00:12:41 [Speaker Changed] If nothing in your portfolio is performing badly, you’re not diversified. I did it in 2000, 2002. And the managers you selected were all based on past performance.

And so even though current portfolio values might be down, the expected future returns are higher. Over the last 25 years, we have seen four bear markets (1999-2002, 2008-2009, 2020, 2022) and numerous market corrections (10% losses). Take 2022 and 2023 as an example.

Treasury Department recently issued proposed regulations that would virtually eliminate valuation discounts on the transfer of shares in family businesses and investment pools held in Family Limited Partnerships or Limited Liability Companies, collectively known as FLPs.

Treasury Department recently issued proposed regulations that would virtually eliminate valuation discounts on the transfer of shares in family businesses and investment pools held in Family Limited Partnerships or Limited Liability Companies, collectively known as FLPs.

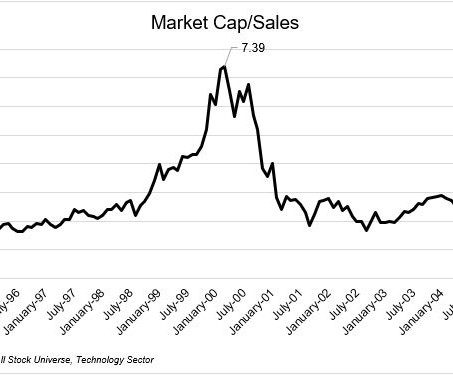

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. Unsurprisingly, as volume has increased, so have valuations.

Today the Global Leaders portfolio cash flow duration in real terms is in the 15 to 17-year range using this calculation. Our standard valuation framework looks out over a 10-year cash flow forecast ending with zero % real growth in the terminal cashflow (technically we use 3% nominal terminal growth).

In this article, our head of asset allocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. As a result, our portfolios currently seek exposure to asset classes and holdings with less dependency on foreign trade. We need to build portfolios on a foundation of facts.

In this article, our head of asset allocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. As a result, our portfolios currently seek exposure to asset classes and holdings with less dependency on foreign trade. We need to build portfolios on a foundation of facts.

And then in ‘94 and ’98, you know, all had a different stream to 2002. But you know exactly how they’re going to interplay within a portfolio, hugely powerful. You know, it’s not the equity market, and I run some big equity portfolios, you know, different. Last year, it’s in our tactical portfolios.

I started with a diversified portfolio that eventually went the way of FAANG; however, over the past 3-4 years I’ve gravitated around the highest growth companies out there.If Stocks flooded the market, and valuations stretched into the stratosphere. Amazon continued to grow between the peak in 99 through the end of 2002.

But that valuation, to be able to come up with the valuation, to be then able to work in a restructuring process, bankruptcy process, and say, Hey, I think at the end of this, we are buying debt at 50 cents. So in 2002, when we start, it’s not the.com debris we are looking through. It could be worth 80, 90 cents.

That’s a really easy portfolio to create. It allows you to understand, generally speaking, what is a reasonable beta for that whole portfolio. By the time I got there in ’92, they had a great venture portfolio and almost nobody else even understood what venture capital was. That allows you to do two things.

It’s quite similar to owning a portfolio of rental houses spread throughout the world: while house prices fluctuate all the time in different cities, the total rent paid by a group of thousands of tenants will tend to remain pretty stable and just rise at the rate of inflation.

At its height spanning 14 years between 2002 and 2016, the company went on an acquisition spree. Not only this the company also had services spanning 17 international locations. But Then How did it All Go Wrong for Cox & Kings? They successfully acquired 9 major business units across the world. Sounds all good right? Happy Investing!

00:44:11 [Speaker Changed] Kathy would may have her own valuation, so, but I can’t replicate it myself. 00:49:30 [Speaker Changed] I bought it around 2000 and it crashed around 2002. Why is there such a spread between US domestic and overseas companies in terms of you’re a value investor in terms of straight up valuation?

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. And so, that didn’t happen until 2002. I mean, you know, this is probably 2002. Valuations go up and you saw it, of course, in the late ‘90s, in the tech sector.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. to a grantor trust) similarly remain attractive because of low interest rates and potentially low valuations.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. to a grantor trust) similarly remain attractive because of low interest rates and potentially low valuations. Outright Gifting.

The transcript from this week’s, MiB: Aswath Damodaran: Valuations, Narratives & Academia , is below. You’re known as the dean of valuation. He said, oh, dean of valuation, it’s easier to say. So let’s start with the question, what led you to focus on valuation? RITHOLTZ: Right. And I said, why?

I graduated Columbia 2002, and I’m the only person I know who stayed in the same job for the last 23 00:08:35 [Speaker Changed] Years. Or, or people start out with a CFA and they decide, you know, I would rather manage the portfolio than tell I’d rather be a PM than advise the pm.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content