This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

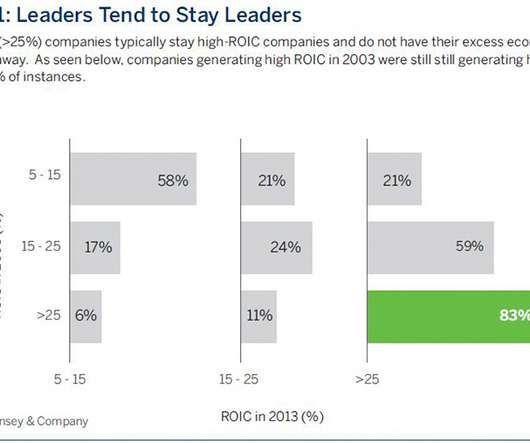

Companies generating ROIC of 25%+ in 2003 sustained that level a decade later 83 percent of the time. As seen below, companies generating high ROIC in 2003 were still still generating high ROIC in2013 in 83% of instances." as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition."

Companies generating ROIC of 25%+ in 2003 sustained that level a decade later 83 percent of the time. As seen below, companies generating high ROIC in 2003 were still still generating high ROIC in2013 in 83% of instances." as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition."

Since then, value has outperformed growth for the longest sustained period since 2003–2007. The monetary factor is the factor we are focused on, as the two periods of sustained value outperformance in the last 20 years (now, and 2003-2007) coincide with the last two periods when both market interest rates (measured by the 10-year U.S.

And I always use the exact same example, how will you invest in Google in 1998, or in Facebook in 2003? Conviction, so we look at, you know, whether or not a specific theme is something that we have a high degree of conviction that will be a trend, that will definitely have an impact in the economy over the next two or three decades.

Ryan is going to talk about the global economy and what’s going on both here and abroad. And it looks like they could drop rates if there was the right kind of economy and the right kind of stability in our economy. What I’m showing here is the annualized rate of growth of different economies. I have the U.K.

This is achieved by investing in a concentrated portfolio of companies that, according to our analysis, generate durable levels of free cash flow, exhibit capital discipline and have attractive valuations. They have been chosen for their capital discipline and durable fundamental cash flow, together with an attractive valuation.

It conducted the Indian Readership survey for 10 years from 2003 – 2012, covering over 20 Lakh in-person interviews. This increase was supported by growth in marketing spending of Indian corporates, a rise in the revenue of companies, and an increase in the gross domestic output in the economy.

On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. Reasons for this tendency are varied.

According to a decade-long study by McKinsey & Company, companies that produce a ROIC in excess of 25% in 2003 still produced a ROIC in excess of 25% a decade later. BRI is a crucial lender to the informal economy in these rural regions and leads the Indonesian microfinance market. 6th Edition, 2015. 6th Edition, 2015.

On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. Reasons for this tendency are varied.

According to a decade-long study by McKinsey & Company, companies that produce a ROIC in excess of 25% in 2003 still produced a ROIC in excess of 25% a decade later. S&P 500® Index, ROIC, 2003-2013 Data based on a McKinsey & Company study, “Valuation: Measuring and Managing the Value of Companies”. 6th Edition, 2015.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. And so, Crispin and I were having lunch in late 2003.

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. Second part of our framework is valuation fundamental work. Well, that means valuations are probably too high.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. There’s a continual, the economy continues to grow. She was based out in Los Angeles.

stocks powered out of the toxic storm of ever-rising interest rates and inflation into a the spectacular market rebound of 2023 as the prospects of a soft(er) landing for the economy grew more probable. In the more recent decade not including 2023 (2003-2012), U.S. During the 2003-2012 period, U.S. Large Cap, Developed ex-U.S.

He brings a fascinating approach and a bit of an outlier, contrarian way of looking at the world that has allowed him to identify specific changes in what’s taking place in the economy, in the markets, and essentially provide a helpful sounding board to many of the world’s best investors. MIAN: Valuations are ebb and flow.

So that little detour was in 2003. So think about 2003 home prices had gone up a lot from 2000. So mortgage position in 2000 were way more valuable in 2003 than they were when they originated because they weigh less credit risk. Barry Ritholtz : Most people rarely hear it described that way.

The transcript from this weeks, MiB: Apollo’s Torsten Slok on the US Economy & Trump 2.0 , is below. You know, most of the economists that you’re probably familiar with haven’t really had a good handle on the state of the economy over the past couple of years. And it was a 2003 and we lived in Paris.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content