This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By using the PEG ratio, Lynch sought to identify stocks that were not only growing quickly but also trading at valuations that made sense relative to that growth. Model Performance & Return History Since its inception on Validea in 2003, the 20-stock, monthly rebalanced Peter Lynch-based portfolio has delivered a 1,142.0%

Beyond Cheap: Quality Matters While valuation was crucial, Dreman wasn’t interested in just any cheap stock. A 10-stock portfolio based on his criteria returned 79.2% over five years from 2003-2008, nearly quadrupling the S&P 500’s gain. The portfolio maintained a beta of roughly 1.0,

His model is both conservative and disciplined, focusing on balance sheet strength and attractive valuations. Moderate Valuation (P/E 15) Limiting how much you pay for earnings ensures you dont overpay for future growth that may never materialize. Reasonable Price/Book Ratio (P/B P/E 22) A safeguard against excessive valuations.

A companys price-to-earnings (P/E) ratio must be in line with or lower than its earnings growth rate to ensure valuation remains attractive. Small Cap Growth Models Risk and Return Stats Since 2003, the ten stock, tax efficient portfolio has delivered a 13.5% annual return (477% cumulative).

And then in about 2003, we set up a group called the European Special Situations Group, which was a multi-asset class proprietary investing business. But what was interesting about that was the quick need to both separate the portfolio between the old stuff and the new stuff, because there were a lot of new investment opportunities.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. Initially I joined to help them manage their equity portfolio. She was based out in Los Angeles.

As these tables can take a while to be published or readily available, let’s for now break the past twenty years of available market data into two 10-year periods: 2003-2012 and 2013-2022. In the more recent decade not including 2023 (2003-2012), U.S. During the 2003-2012 period, U.S. Large Cap, Developed ex-U.S.

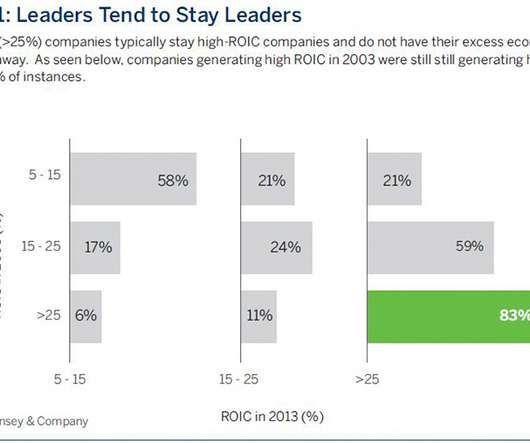

Companies generating ROIC of 25%+ in 2003 sustained that level a decade later 83 percent of the time. As seen below, companies generating high ROIC in 2003 were still still generating high ROIC in2013 in 83% of instances." as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition."

Companies generating ROIC of 25%+ in 2003 sustained that level a decade later 83 percent of the time. As seen below, companies generating high ROIC in 2003 were still still generating high ROIC in2013 in 83% of instances." as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition."

We’ve been running quantitative model portfolios since 2003. While many of our models were launched after that, our initial set of guru models actually went live in July of 2003, so this year we’ll hit the 20-year mark in terms of running systematic investment strategies. Guru Model Portfolios. in 2022 vs. a 19.4%

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. Second part of our framework is valuation fundamental work. Well, that means valuations are probably too high.

And my answer was, “Hey, not everybody wants to buy a passive index around the satellite of a core portfolio or even just, hey, I have an idea, I think this is going to change the world.” And I always use the exact same example, how will you invest in Google in 1998, or in Facebook in 2003? Is that the clients you’re aiming for?

Instead, they’ve turned to indexing their portfolios to the S&P 500 ® Index or some other relevant benchmark, thereby accepting “average” performance rather than trying for something better. Portfolios with greater active share could be said to reflect more independent thinking on the part of the managers.

Instead, they’ve turned to indexing their portfolios to the S&P 500 ® Index or some other relevant benchmark, thereby accepting “average” performance rather than trying for something better. Portfolios with greater active share could be said to reflect more independent thinking on the part of the managers. Manager Characteristics.

The Company initially began operations as an Original Equipment Manufacturer (OEM) back in 2003. These listed companies trade at a median valuation of 66.8x So what do you think of its PE valuation, do you think it’s a justified valuation or are the promoters being too optimistic about the Company?

This is achieved by investing in a concentrated portfolio of companies that, according to our analysis, generate durable levels of free cash flow, exhibit capital discipline and have attractive valuations. We do not take an exclusionary approach at Brown Advisory andinstead build portfolios from the bottom up. Source: FactSet.

Reflections for Five Years of Global Leaders ajackson Tue, 05/12/2020 - 09:38 The Global Leaders strategy is focused on delivering long-term performance by building a concentrated portfolio of market-leading companies from across the globe. We are saddened by the considerable impact and disruption this is having on society globally.

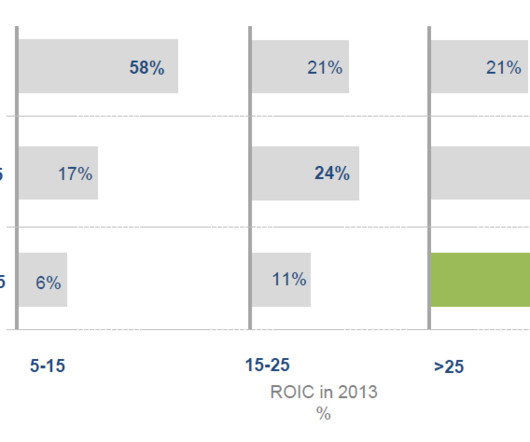

The Global Leaders strategy is focused on delivering long-term performance by building a concentrated portfolio of market-leading companies from across the globe. According to a decade-long study by McKinsey & Company, companies that produce a ROIC in excess of 25% in 2003 still produced a ROIC in excess of 25% a decade later.

Hundreds of academic studies and thousands of media commentaries have taken different angles on this issue, with the conversation centered on one key question: Does the incorporation of ESG factors in portfolios help, hurt, or do nothing to returns? Can we also generate predictable utility from managing portfolios around an "ESG factor?"

Hundreds of academic studies and thousands of media commentaries have taken different angles on this issue, with the conversation centered on one key question: Does the incorporation of ESG factors in portfolios help, hurt, or do nothing to returns? Can we also generate predictable utility from managing portfolios around an "ESG factor?"

MIAN: So Stray Reflections is a macro advisory and community that works with portfolio managers, CIOs around the world. The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. MIAN: Valuations are ebb and flow. Tell us a little bit about your research. RITHOLTZ: Right.

Then let us look at their recent Annual earnings and what valuation are they currently at. The Company has been a pioneer in the field, creating a portfolio of over 470 Products, all derived from Natural Plant-based oils. We have chosen small caps with a strong growth rate and strong return ratios. Cr EPS ₹34.66 Stock P/E (TTM) 19.74

When does crowd psychology take hope for economic return beyond what valuation can support? And why do markets irregularly detach fundamentals from valuation to their own detriment? as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition.” In his book “What is Time?

It conducted the Indian Readership survey for 10 years from 2003 – 2012, covering over 20 Lakh in-person interviews. The IPO valuation also seems expensive at the PE of 40x. A subsidiary of the Company Hansa Research focuses on brand equity, customer satisfaction, and market research. So what are your views on the upcoming IPO?

The company has diversified its business portfolio into broking, asset management, wealth management, private equity and real estate segment. The valuation of the company is undervalued compared to the industry with a PE of 8.71 With a market capitalisation of Rs 11,411 Cr, it is the second largest listed broking stock of 2022.

On Friday, May 24 th at 12pm Pacific time, Investment Advisor & Financial Planner Laurent Harrison, CFP® joined Bell Portfolio Manager Ryan Kelley, CFA® for an engaging discussion of the following topics: Stock & Bond Market Commentary Global Economic Update Inflation Concerns & the Federal Reserve Are Stocks Expensive?

Yes Bank was founded in 2003 by Rana Kapoor and Ashok Kapur. By utilizing the stock screener , stock heatmap , portfolio backtesting , and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks and make well-informed investment decisions.

The top performing Zweig-inspired portfolio on Validea is the 20 stock, tax efficient portfolio. Since 2003, this portfolio has returned 1,113.1% , outperforming the market by 642.2%. Its best year was 2013 , when the portfolio returned +57.1% , far outpacing the S&P 500s +29.6% gains, respectively.

00:44:11 [Speaker Changed] Kathy would may have her own valuation, so, but I can’t replicate it myself. So, so let’s talk a little bit about picking international stocks as an asset class has done fairly poorly, but it’s nearly a third of your portfolio and, and you continue to outperform. How big a position was this?

So that little detour was in 2003. So think about 2003 home prices had gone up a lot from 2000. So mortgage position in 2000 were way more valuable in 2003 than they were when they originated because they weigh less credit risk. So that’s an active part of portfolio trimming and opt and optimization.

And it was a 2003 and we lived in Paris. And we have 50, a little less than 50 portfolio companies talking to the CEOs of these portfolio companies. How do you think about valuations for both equities and fixed income here in the beginning of 2025? And this was in 2005. It was not our plan. We all enjoyed it.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content