This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By using the PEG ratio, Lynch sought to identify stocks that were not only growing quickly but also trading at valuations that made sense relative to that growth. Model Performance & Return History Since its inception on Validea in 2003, the 20-stock, monthly rebalanced Peter Lynch-based portfolio has delivered a 1,142.0%

Beyond Cheap: Quality Matters While valuation was crucial, Dreman wasn’t interested in just any cheap stock. over five years from 2003-2008, nearly quadrupling the S&P 500’s gain. The strategy showed particular strength in 2003, 2004, and 2006, with returns exceeding 30% in each of those years.

His model is both conservative and disciplined, focusing on balance sheet strength and attractive valuations. Moderate Valuation (P/E 15) Limiting how much you pay for earnings ensures you dont overpay for future growth that may never materialize. Reasonable Price/Book Ratio (P/B P/E 22) A safeguard against excessive valuations.

A companys price-to-earnings (P/E) ratio must be in line with or lower than its earnings growth rate to ensure valuation remains attractive. Small Cap Growth Models Risk and Return Stats Since 2003, the ten stock, tax efficient portfolio has delivered a 13.5% annualized return (1,455% cumulative) , far outpacing the S&P 500s 8.4%

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

As these tables can take a while to be published or readily available, let’s for now break the past twenty years of available market data into two 10-year periods: 2003-2012 and 2013-2022. In the more recent decade not including 2023 (2003-2012), U.S. During the 2003-2012 period, U.S. Large Cap, Developed ex-U.S.

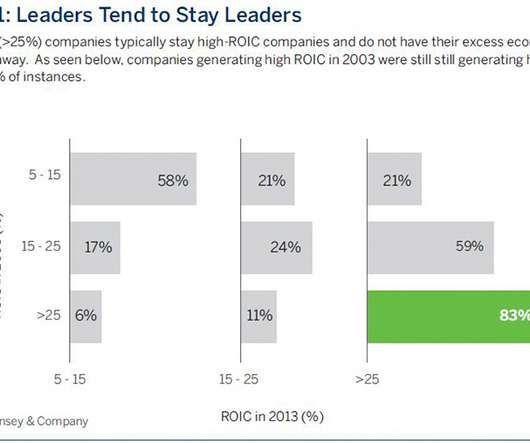

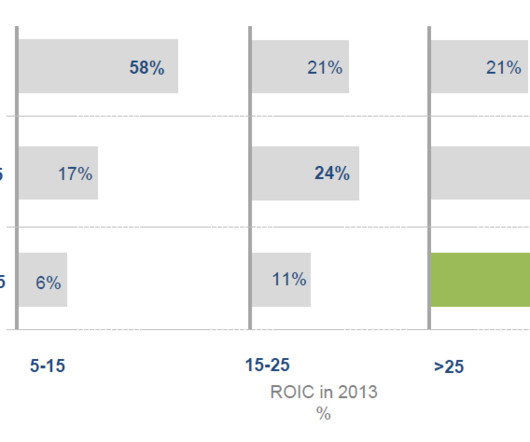

Companies generating ROIC of 25%+ in 2003 sustained that level a decade later 83 percent of the time. As seen below, companies generating high ROIC in 2003 were still still generating high ROIC in2013 in 83% of instances." as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition."

Companies generating ROIC of 25%+ in 2003 sustained that level a decade later 83 percent of the time. As seen below, companies generating high ROIC in 2003 were still still generating high ROIC in2013 in 83% of instances." as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition."

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. Second part of our framework is valuation fundamental work. Well, that means valuations are probably too high.

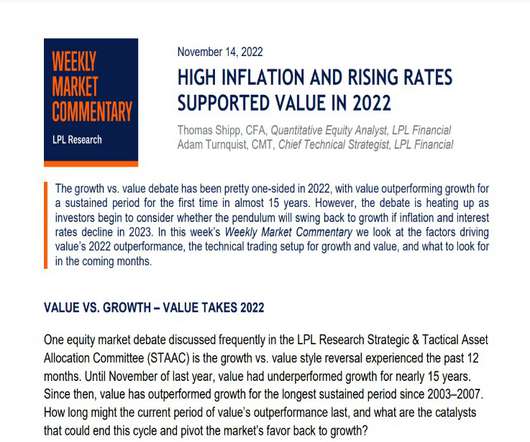

Since then, value has outperformed growth for the longest sustained period since 2003–2007. The monetary factor is the factor we are focused on, as the two periods of sustained value outperformance in the last 20 years (now, and 2003-2007) coincide with the last two periods when both market interest rates (measured by the 10-year U.S.

The Company initially began operations as an Original Equipment Manufacturer (OEM) back in 2003. These listed companies trade at a median valuation of 66.8x So what do you think of its PE valuation, do you think it’s a justified valuation or are the promoters being too optimistic about the Company?

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. It pushes valuations higher over time. 00:04:02 That’s what value add software was originally.

We’ve been running quantitative model portfolios since 2003. While many of our models were launched after that, our initial set of guru models actually went live in July of 2003, so this year we’ll hit the 20-year mark in terms of running systematic investment strategies. By Justin Carbonneau ( @jjcarbonneau ) —.

When does crowd psychology take hope for economic return beyond what valuation can support? And why do markets irregularly detach fundamentals from valuation to their own detriment? as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition.” In his book “What is Time?

On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. Reasons for this tendency are varied.

According to a decade-long study by McKinsey & Company, companies that produce a ROIC in excess of 25% in 2003 still produced a ROIC in excess of 25% a decade later. 6th Edition, 2015. 6th Edition, 2015. ROIC is calculated as percentage without goodwill. The selected sample is the S&P 500® Index. “We

On the upside, active managers are often reluctant to overweight or “chase” the leading stocks in the market because those stocks typically sell at premium valuations. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations. Reasons for this tendency are varied.

According to a decade-long study by McKinsey & Company, companies that produce a ROIC in excess of 25% in 2003 still produced a ROIC in excess of 25% a decade later. S&P 500® Index, ROIC, 2003-2013 Data based on a McKinsey & Company study, “Valuation: Measuring and Managing the Value of Companies”. 6th Edition, 2015.

And I always use the exact same example, how will you invest in Google in 1998, or in Facebook in 2003? And we’re having very good conversations with clients that I think, at current valuation levels, they remain, you know, very interested in the market and they see some opportunities. BERRUGA: This is 2003.

And then in about 2003, we set up a group called the European Special Situations Group, which was a multi-asset class proprietary investing business. One, when people have asked me to compare and contrast today versus 2007, 2008, what you hear from a lot of people is, yes, there’s some fairly heady valuations.

This is achieved by investing in a concentrated portfolio of companies that, according to our analysis, generate durable levels of free cash flow, exhibit capital discipline and have attractive valuations. They have been chosen for their capital discipline and durable fundamental cash flow, together with an attractive valuation.

It conducted the Indian Readership survey for 10 years from 2003 – 2012, covering over 20 Lakh in-person interviews. The IPO valuation also seems expensive at the PE of 40x. A subsidiary of the Company Hansa Research focuses on brand equity, customer satisfaction, and market research.

Then let us look at their recent Annual earnings and what valuation are they currently at. Operating Profit Margin (%) 44.00% Net Profit Margin (%) 26.55% Best Small Cap Chemical Stocks #3 – Clean Science & Technology Clean Science is a chemical manufacturing Company established in 2003. Cr EPS ₹34.66 Stock P/E (TTM) 19.74

The valuation of the company is undervalued compared to the industry with a PE of 8.71 MCX India started its operations in November 2003 under the regulatory framework of the Securities and Exchange Board of India (SEBI). The profitability of the company has also increased from Rs 829 Cr in FY18 to Rs 1,616 Cr in the same period.

Stock Valuations Stretched Once Again 21:24 Ryan Kelley: We’ll look on the next slide. It’s about valuation on stocks. There are a lot of ways to measure valuation. That compares unfavorably to the historic median, which is 16x, and that’s measuring back to 2003. Slide 13: U.S. Slide 17: Questions?

Yes Bank was founded in 2003 by Rana Kapoor and Ashok Kapur. Worst Performing Stocks in India – Yes Bank The story of Yes Bank is the perfect example of a success story gone wrong in the banking industry. It began its operation in 2004. The bank network spanned 1120 locations across all 29 states in India.

ESG information helps with broader due diligence, providing insight into a company’s sustainability strategies alongside their fundamental strengths, the competitive environment, and, of course, stock valuation at the time of buy or sell decisions. John Wiley and Sons. Sustainability and Performance." Sloan Management Review 44(2): 65-70.

ESG information helps with broader due diligence, providing insight into a company’s sustainability strategies alongside their fundamental strengths, the competitive environment, and, of course, stock valuation at the time of buy or sell decisions. Broader Application and Paths for Future Research. John Wiley and Sons. Henderson, R.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. And so, Crispin and I were having lunch in late 2003.

Since 2003, this portfolio has returned 1,113.1% , outperforming the market by 642.2%. Valuation discipline keeps investors from overpaying for even the fastest-growing companies. His model aims to ensure that a companys success is driven by genuine business strengthnot by cost-cutting or accounting gimmicks.

The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. The second, and what’s interesting about that period, is the fact that valuations actually peaked in 1961. MIAN: Valuations are ebb and flow. Legal immigration has been trending lower since the Gulf War in 2003.

00:44:11 [Speaker Changed] Kathy would may have her own valuation, so, but I can’t replicate it myself. Why is there such a spread between US domestic and overseas companies in terms of you’re a value investor in terms of straight up valuation? That’s the value that I am looking for. So you could definitely bury that.

So that little detour was in 2003. So think about 2003 home prices had gone up a lot from 2000. So mortgage position in 2000 were way more valuable in 2003 than they were when they originated because they weigh less credit risk. Barry Ritholtz : Most people rarely hear it described that way.

And it was a 2003 and we lived in Paris. How do you think about valuations for both equities and fixed income here in the beginning of 2025? So Sheila Cyclically adjusted so-called cape ratio at 37 is and 38 and approaching 40 is indeed a very, very elevated level of valuation. And this was in 2005. It was not our plan.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content