This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

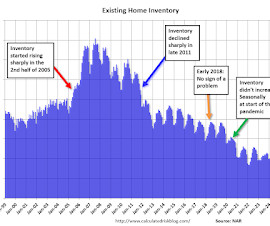

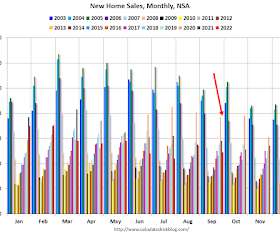

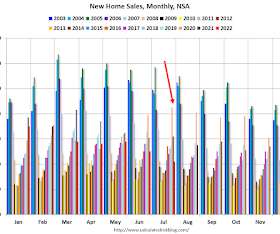

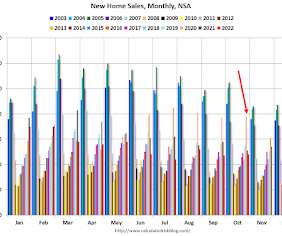

Watch Inventory Here are a few examples of when inventory helped me call some turning points for house prices (this section is an update to a previous article): Starting in January 2005, I was very bearish on housing , but I wasnt sure when the market would turn. Speculative bubbles can go on and on.

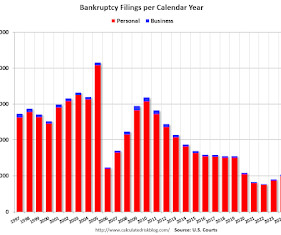

The sharp decline in 2006 was due to the so-called "Bankruptcy Abuse Prevention and Consumer Protection Act of 2005". This graph shows the business and non-business bankruptcy filings by calendar year since 1997. 2024 was the 4th lowest year for bankruptcy filings, and 33% below the pre-pandemic level in 2019.

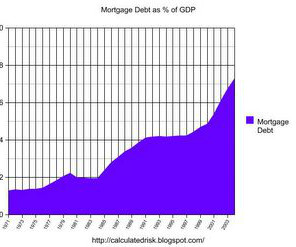

In a 2005 post , I included a graph of household mortgage debt as a percent of GDP. First, from February 2005 (20 years ago!): The bottom line remains the same: There will not be cascading price declines in this cycle due to distressed sales. Several readers asked if I could update the graph.

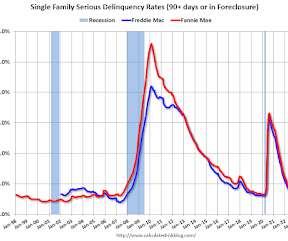

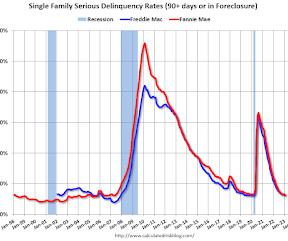

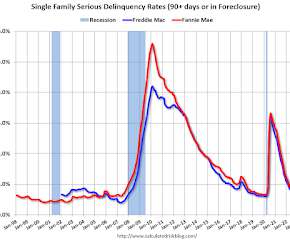

For loans made in 2005 through 2008 (1% of portfolio), 3.83% are seriously delinquent (down from 3.95%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.55% are seriously delinquent (down from 0.57%).

For loans made in 2005 through 2008 (1% of portfolio), 3.49% are seriously delinquent (down from 3.71%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.52% are seriously delinquent (down from 0.53%).

Starting in January 2005, I was very bearish on housing , but I wasn’t sure when the market would turn. However, the increase in inventory in late 2005 (see red arrow on graph below) helped me call the top for house prices in 2006. Here is an update to that post with a few additional comments. Speculative bubbles can go on and on.

For loans made in 2005 through 2008 (1% of portfolio), 3.11% are seriously delinquent (down from 3.31%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.48% are seriously delinquent (down from 0.51%).

For loans made in 2005 through 2008 (1% of portfolio), 3.49% are seriously delinquent (unchanged from 3.49%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.53% are seriously delinquent (up from 0.52%).

The sharp decline in 2006 was due to the so-called "Bankruptcy Abuse Prevention and Consumer Protection Act of 2005". (a This graph shows the business and non-business bankruptcy filings by calendar year since 1997. a good example of Orwellian named legislation since this was more a "Lender Protection Act").

Kudos to Ibbotson and Sinquefield for their work, and to Justin Fox for reminding us of their contributions (in 2005!). By Justin Fox Fortune Magazine, December 26, 2005 _ 1. Such was the case with a Justin Fox article “ 9% Forever? ” 2.

For loans made in 2005 through 2008 (1% of portfolio), 3.71% are seriously delinquent (down from 3.83%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.53% are seriously delinquent (down from 0.55%).

Today, in the Calculated Risk Real Estate Newsletter: The Housing Bubble and Mortgage Debt as a Percent of GDP A brief excerpt: In a 2005 post , I included a graph of household mortgage debt as a percent of GDP. First, from February 2005 (18 years ago!): Several readers asked if I could update the graph.

Starting in January 2005, I was very bearish on housing , but I wasn’t sure when the market would turn. However, the increase in inventory in late 2005 (see red arrow on graph) helped me call the top for house prices in 2006.Several Here are a few times when watching existing home inventory helped my analysis.

I entered the workforce in 2005. I’m on vacation for Thanksgiving this week. Here’s one of the most popular posts on the blog from the past year. * That means I’ve been working in the investment business for 20 years now.

The all-time high for August was 110 thousand in 2005, and the all-time low for August was 23 thousand in 2010. The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate). In August 2022 (red column), 55 thousand new homes were sold (NSA). Last year, 55 thousand homes were sold in August.

Starting in January 2005, I was very bearish on housing , but I wasn’t sure when the market would turn. However, the increase in inventory in late 2005 (see red arrow on graph) helped me call the top for house prices in 2006.Several Here are a few times when watching existing home inventory helped my analysis.

The sharp decline in 2006 was due to the so-called "Bankruptcy Abuse Prevention and Consumer Protection Act of 2005". This graph shows the business and non-business bankruptcy filings by calendar year since 1997. 2023 was the 3rd lowest year for bankruptcy filings, and 42% below the pre-pandemic level in 2019.

For loans made in 2005 through 2008 (1% of portfolio), 4.11% are seriously delinquent (down from 4.45%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.60% are seriously delinquent (down from 0.63%).

The all-time high for June was 115 thousand in 2005, and the all-time low for June was 28 thousand in 2010 and in 2011. The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate). In June 2022 (red column), 49 thousand new homes were sold (NSA). Last year, 61 thousand homes were sold in June.

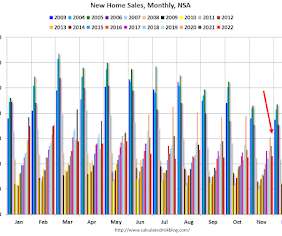

The all-time high for November was 86 thousand in 2005, and the all-time low for November was 20 thousand in 2010. The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate). In November 2022 (red column), 46 thousand new homes were sold (NSA). Last year, 54 thousand homes were sold in November.

The following scatter graph is for the years 2005 through 2023 and compares October retail hiring with the real increase (inflation adjusted) for retail sales (Q4 over previous Q4). Note that in the early '90s, retailers started hiring seasonal workers earlier - and the trend towards hiring earlier has continued.

The following graph shows new home sales for three periods: 1978-1982, 2005-2020, and current (red). Here is a graph to illustrate this point. The prior peak in sales is set to 100. When the Fed took their foot off the brake in 1982, new home sales recovered fairly quickly (blue). The same is true for the 1989 -1991 bust (not shown).

For loans made in 2005 through 2008 (1% of portfolio), 3.95% are seriously delinquent (down from 4.11%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.57% are seriously delinquent (down from 0.60%).

For loans made in 2005 through 2008 (1% of portfolio), 3.31% are seriously delinquent (down from 3.40%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.51% are seriously delinquent (down from 0.52%).

He was President and Director of the Society of FSP Central Indiana Chapter from 2002 through 2005. Previously, he served terms on the FSP National Board of Directors from 2011 through 2016.

January 2008) Lose the News (June 2005) Manage Your Media Diet The post Peak Substack? I have no idea whether its a long-term staple or a flash in the pan, but it feels to me like I am now at peak Substack… Previously : Things I Don’t Care About (January 15th, 2013) What Do You Control? (May appeared first on The Big Picture.

For loans made in 2005 through 2008 (1% of portfolio), 4.45% are seriously delinquent (down from 4.67%), For recent loans, originated in 2009 through 2021 (97% of portfolio), 0.63% are seriously delinquent (down from 0.69%).

Black and light Purple are the maximum sales per month during the bubble (2005) and the minimum sales during the bust (2008 - 2011). The third graph shows existing home sales for each month, Not Seasonally Adjusted (NSA), for a few selected periods. The most recent four years are shown (2019 through 2022). Sales NSA in July (453,000) were 22.4%

Breakaway : For only the 25 th time since World War II (an average of once every 3 1/2 years), the Dow Jones Industrials registered what technician Walter Deemer calls “breakaway momentum” (or “breadth thrust”).

Professor Jeremy Siegel at the University of Pennsylvania, where he is frequently voted Best professor at Wharton, and is the author of Stocks for the Long Run , Jeremy Schwartz is CIO at Wisdom Tree Asset Management , where he has worked since May 2005.

Previously : Earnings Ex -Inflation, There is No Inflation (September 26, 2005) Inflation Ex-Deflation (this time, INCLUDING energy) (June 22, 2012) CPI: Imperfect But Useful (May 24, 2022) The post What Earnings Recession? appeared first on The Big Picture.

The all-time high for September was 99 thousand in 2005, and the all-time low for September was 24 thousand in 2011. In September 2022 (red column), 49 thousand new homes were sold (NSA). Last year, 58 thousand homes were sold in September. I'll have more later today.

The all-time high for December was 87 thousand in 2005, and the all-time low for December was 23 thousand in 2010. The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate). In December 2022 (red column), 47 thousand new homes were sold (NSA). Last year, 61 thousand homes were sold in November.

I used to track this quarterly back in 2005 and 2006 to point out that households were taking on excessive financial obligations. The Fed's Household Debt Service ratio through Q4 2022 was released last week: Household Debt Service and Financial Obligations Ratios.

The all-time high for July was 117 thousand in 2005, and the all-time low for July was 26 thousand in 2010. The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate). In July 2022 (red column), 42 thousand new homes were sold (NSA). Last year, 62 thousand homes were sold in July. I'll have more later today.

In a 2005 post , I included a graph of household mortgage debt as a percent of GDP. First, from February 2005 (19 years ago!): The bottom line remains the same: There will not be cascading price declines in this cycle due to distressed sales. Several readers asked if I could update the graph.

Here is a table of the annual change in real GDP since 2005. Real GDP Growth Year Annual GDP Q4 / Q4 2005 3.5% Also note that the sharp decline in 2010 was related to the housing tax credit policy in 2009 - and was just a continuation of the housing bust. Prior to the pandemic, economic activity was mostly in the 2% range since 2010.

The all-time high for October was 105 thousand in 2005, and the all-time low for October was 23 thousand in 2010. The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate). In October 2022 (red column), 48 thousand new homes were sold (NSA). Last year, 51 thousand homes were sold in October.

The founder and CEO of Hermitage Capital Management, which was the investment adviser to the largest foreign investment fund in Russia until 2005, Browder is also the author of “ Red Notice: A True Story of High Finance, Murder and One Man’s Fight for Justice.”

For loans made in 2005 through 2008 (1% of portfolio), 2.44% are seriously delinquent (down from 2.53%). Mortgages in forbearance are being counted as delinquent in this monthly report but are not reported to the credit bureaus.

Before joining Morningstar in 2005, Norton was an economist with the Bureau of Labor Statistics and a research analyst at LECG LLC. The firm manages or advises on about $250 billion in advisor assets. Norton’s responsibilities include equity, alternative and fixed income research, asset allocation, and portfolio management.

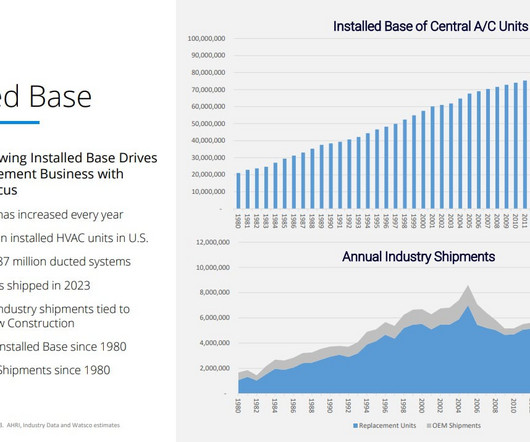

Earlier this year, Lennox’s Geoff Dethlefsen commented on the opportunity: “You look at the [commercial] installed base from that 2000 to 2005 time period, there was a massive installed base put into service. The opportunity is just as strong on the commercial side as it is with residential units.

billion in client assets, and has created over $11 billion of net P&L across all strategies since its 2005 inception. The firm is a multi-strategy and multi-product alternative investment management firm, managing $14.9

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content