This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The firm manages or advises on about $250 billion in advisor assets. Norton’s responsibilities include equity, alternative and fixed income research, assetallocation, and portfolio management. Before joining Morningstar in 2005, Norton was an economist with the Bureau of Labor Statistics and a research analyst at LECG LLC.

So Magnetar launches in 2005 with some capital, and you joined you, you weren’t one of the original founders, but you joined not long afterwards. So back then you, you probably remember in 2005, you know, there were a lot of what they called pod shops. So it’s, it’s assets like that.

Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains. Reassess assetallocation. Callan estimated that a portfolio in 2005 could achieve a 7.5%

That tops the inflation fears that surged in 2008, just before the financial crisis, and a previous peak in early 2005, when the housing market was out of control.” . This way, people can better identify the assets they need to take risks with in order to outpace inflation. bond market’s prediction of U.S. to 6% in interest.”.

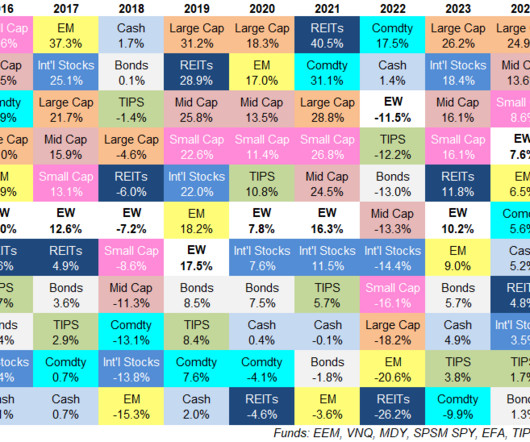

The first assetallocation quilt I created for this site covered the ten-year period from 2005-2014. Those returns look nothing like the last 10 years which is the whole point of this exercise. Treasury-inflation protected securities were up 2.1% annually over the sam.

No income, no job, no assets were exactly ninja, Sean Dobson : No pulse seems reasonable. We see it as, like I said, about 50 million assets and we’re modeling up the value of every home in the country, every, every week, basically. And in the 2000 at the 2005 conference, it’s kind of wild.

They run over $431 billion in global assets. Most of what they do are, are real assets, credit debt, middle market banking. But really in 2005 I made that, that shift to, to, to Babson and, and really still doing what I was doing focused on, on, you know, fundamental fixed income analysis. What a fascinating guest.

This was the era, 2005, 2006, all of my friends were looking to get banking roles. We were talking about luck earlier, got introduced to a local asset manager outside of Boston who saw what I was working on and said, this is really interesting. I mean, that’s why it gathered so many assets. It was truly a throwaway name.

Fisher, 1958 The Money Game - George Goodman, 1967 A Random Walk Down Wall Street - Burton Malkiel, 1973 Manias, Panics, and Crashes: A History of Financial Crises - Charles Kindleberger, 1978 The Alchemy of Finance - George Soros, 1987 Market Wizards - Jack Schwager, 1989 Liar's Poker - Michael Lewis, 1989 101 Years on Wall Street, An Investor's Almanac (..)

I think that the asset stripping that has also occurred, pensions, for instance, are sold off, overfunded pensions get sold off and that goes into the private equity firm instead of into the company itself. Or should this be kept out of private assetallocators’ hands? And this was back in 2005 or 2006.

I started that in 2005, after I graduated. And you know, the Fed can play a role in sort of backtracking sentiment in the short run, but the Fed can’t permanently increase the level of asset values. and so many different asset classes, and so many different types of constituents that they serve, right? RITHOLTZ: Really?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content