This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. BARATTA: I think it was 2005, when we started to look at in China and in India, in particular, and also Japan. So we share themes and we share these economic signals.

And when I was studying in university economics, I did not really get the passion. ILMANEN: It’s always good to think of starting yields and valuation sort of two sides of the same coin. Those types of excess savings were sort of the culprit for the conundrum in 2005 or whatever it was. Explain that. RITHOLTZ: Right.

Rising economic and political risks— including weak global growth and increasing nativism and protectionism in several countries such as the U.S., For example, we found opportunity in small-cap stocks during their 2016 rally because of their relatively low valuations and limited vulnerability to flagging global economic growth.

We, we made in 2005, I believe. That 00:15:42 [Speaker Changed] Was first AI investment, 2005. It was about $170 million valuation. 00:59:32 [Speaker Changed] So, so in late 21, 20 22, valuations had gotten a touch frothy in, in both the public and the private markets. Fair Cast was an investment, a series B investment.

China: The Next Frontier In Venture ajackson Wed, 07/22/2020 - 11:37 In Thomas Friedman’s award-winning 2005 book, The World Is Flat , he highlighted how globalization had leveled the playing field, offering all competitors an equal opportunity. at that time. But California and the U.S. do not have a monopoly on academic talent.

In Thomas Friedman’s award-winning 2005 book, The World Is Flat , he highlighted how globalization had leveled the playing field, offering all competitors an equal opportunity. A 2016 study from the World Economic Forum showed that China now produces more STEM graduates each year than any other country—4.7 Wed, 07/22/2020 - 11:37.

Worst Performing Stocks in India – PC JEWELLERS PC Jewellers was founded by Mr. Padam Chand Gupta in 2005. Worst Performing Stocks in India – Jet Airways All of us remember flying in this economical airline. This made it the absolute worst-performing stock in India over the last 5 years.

So I switched to be an economics major. I graduated economics with, with a lot of coursework in accounting and finance. So Magnetar launches in 2005 with some capital, and you joined you, you weren’t one of the original founders, but you joined not long afterwards. I found out quickly that’s not what I wanted to do.

So I leave the Bureau of Labor Statistics and I move into economic consulting. So I applied and was hired as an ETF analyst in 2005. And so Morningstar coverage was really just getting started on ETFs, right in the 2005, period. NORTON: So 2005-2006 timeframe. And how do we think about them from a valuation perspective?

The emerging markets asset class outperformed all others in 2003, 2005, 2007 and 2009, while finishing second in 2004, 2006, and 2012. I could pull out some socio-economic Jenga pieces that include the high valuation of the U.S. dollar, relative valuations, political uncertainty, the national debt, the 2024 elections, etc.,

A degree in mathematics from Oxford, a doctorate in mathematical epidemiology and economics from Cambridge. And you do a lot of work with infinity [Barry Ritholtz] : 00:03:29 [Speaker Changed] And then economics, which is a little bit squishier. What made you add economics to your, to your graduate degree? What is that?

But thankfully, the next decade, things really accelerated in terms of the growth of the company and growth in the valuation, things like that. Initially, it was started in 2005 and it was called Revolution, but it was just my capital. We’ve been at it for coming on a decade, had only a couple 100,000 customers. RITHOLTZ: Right.

And we’d sort of turn that into a valuation business. MILLER: Well actually I thought, leading up to the great financial crisis, I thought to myself, we’re going to be out of business within a couple of years because nobody wanted an independent valuation. What are the, you know, I’d literally have it in my handheld.

MCCARTHY: I’d back up actually a little bit further in thinking about how did I get there, because I don’t think it was very obvious actually that I would come out of Yale with an ethics, politics and economics degree — RITHOLTZ: Perfect really, right? MCCARTHY: — and end up in M&A on Wall Street. RITHOLTZ: Right.

It was a wild ride because by the time you got, well, so in 2005, we went on a road show trying to tell people what we had learned, and there wasn’t a lot of reception. And in the 2000 at the 2005 conference, it’s kind of wild. Maybe the market hadn’t priced something properly. Sean Dobson : It was a wild ride.

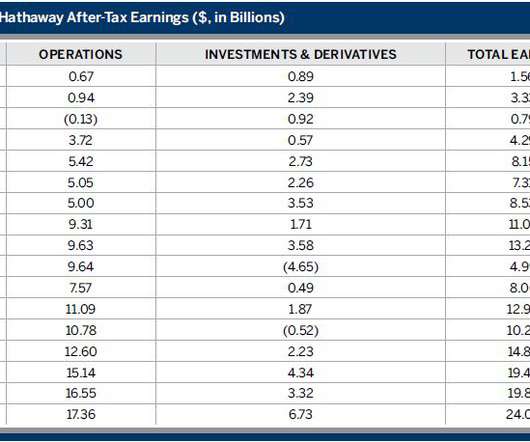

In the 51 years since Buffett took control, Berkshire Hathaway has grown from a small, economically challenged textile company to one of the largest U.S. Low rates also raise valuations for business acquisitions. Ruane passed away in 2005. Berkshire Hathaway. Berkshire is the fifth most valuable company in the U.S. in the bush.

This was the era, 2005, 2006, all of my friends were looking to get banking roles. There’s very few, I would argue probably no consistent predictors of, of any sort of economic or market cyclicality. I think ity economics would argue you have to protect your capital to survive. Barry Ritholtz : That’s hilarious.

WA was the career plan, always economics and finance. And I studied economics in university. And I spent a year in Princeton in the economics department in 95, 96 when Ben Panke was the chairman of the economics department. I’m curious how different studying economics is in Denmark versus United States.

When I look back at 2005, ’06, ’07, yeah, those growth stocks that collapsed from way too high, probably were too low. RITHOLTZ: Did you see the Liberty Street Economics research paper? SCHWARTZ: But even broad developed markets, they’re half the valuation of the U.S. But in the postwar period, we’ve had the cycles.

Valuations Are a Poor Short-Term Timing Indicator Do you like buying things when they are pricey? There is virtually no proof that high (or low) valuations can predict what stocks might do the following year. Rather than making investing decisions based on valuations, you are better off investing in days that end in y if you ask me.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content