This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

He is the Chief Investment Officer of Asset and Wealth Management at Goldman Sachs. He co-chairs a number of the asset management investment committees. trillion in assets under supervision. JULIAN SALISBURY, CHIEF INVESTMENT OFFICER OF ASSET AND WEALTH MANAGEMENT, GOLDMAN SACHS: Thanks, Barry. And I think you will also.

Thinking about all this, I felt I had read about this and observed it in 2007. However, I would insist on following an assetallocation plan with discipline, which is unaffected by the emotions of greed and fear. Assetallocation should follow probabilities of future outcomes along with risk profile.

The analysis above highlights that we are in a rare regime when commodities are the only long asset with a positive trend. But we do know that post-1973 we entered a world where, for several decades (at least up to around 2007), both bonds and commodities were an important component of a diversified portfolio. Will this happen again?

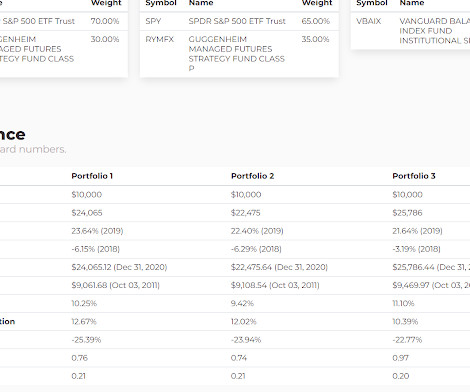

There's no fact sheet yet and while the holdings are available, the assetallocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly). To my knowledge, RYMFX was the first managed futures mutual fund and it had the space to itself for several years after in launched in 2007.

Based on Cambria's other multi-asset funds, ENDW will probably have fixed income duration but that's a space I will continue to avoid. The S&P 500 hit 1500 in March 2000, then again in the fall of 2007 and then the third and final time in January, 2013. The results. Most of us of course lived through that from 2000 through to 2009.

In other words, if you’re 65 in 2007 and 100% invested in stocks and then 2008 happens then you end up going back to work until you’re at least 70. And the only way that disaster happens is if your financial planner is making irrational projections about asset returns and your assetallocation.

Here's the latest about Harvard from Bloomberg that included this chart of the assetallocation. It's not that someone could not copy the asset class exposure, just that the return streams would not look the same and often, various forms of sophistication replication does not really work in fund form. Black is 2023.

First up, the Harvard Endowment which posted the following assetallocation. Here's an article at theStreet.com from 2007 where I bagged on PSP. Arguably neither one is very close in terms of how it replicates but borrowing the assetallocation from the top down yields what I would call a valid result. I used PSP.

They run over $800 billion in client assets, and Kristen’s group, the North American Group, is responsible for about half of the revenue that that massive organization generates. At Citi, in 2007, fantastic timing, you take over as Head of Structured Solutions. And so, 2007, I came over to Citi. BITTERLY MICHELL: Always risk.

Having that much in asset classes that are intended to not look like equities should mean that the long term result won't look anything like the stock market. A 25% allocation to equities for someone who needs equity market growth for their plan to work won't get it done. Then it more than cut in half but is now at 4400.

The federal funds rate hasn’t been this high since 2007 when it peaked at 5.25%. So when the federal funds rate goes up, it can have an outsized impact on shorter term interest rates on assets like Treasury bills (T-bills). This has been the faster pace of rate hikes since the 1980-1981 cycle.

This fierce competition amongst asset management companies is driving down expense ratios, but investor's are potentially paying higher costs. Large Cap ETFs with over $500 million in assets, which means there will always be something in that category doing better than what you've selected. There are 50 U.S.

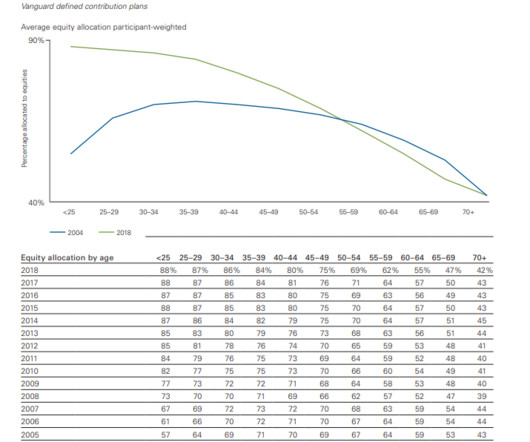

trillion in assets. They anticipate that by 2023 80% of all assets at Vanguard will be in an automatic investment program. Automatic enrollment has tripled since 2007. 18,500, $24,500 for people 50 or older) The chart below shows overall assetallocation in these plans. Here are some of their key findings.

Or you could look at the 2007 high which was within a few points of the 2000 high and say it took 12 years to double. The first is to build a portfolio that you have a reasonable basis to believe can get you to where you need to be can stick with emotionally and maintain an assetallocation that allows you to manage sequence of return risks.

The chart below illustrates that the smart money enters when valuations are low and the majority of the investors aren’t looking at that asset class or security. The important takeaway is that there should be an allocation plan prepared for asset class volatility and it shouldn’t be just an ad-hoc emotional buying or selling.

As the economy is likely downshifting, investors should take heed that the Federal Reserve’s (Fed) current stance is eerily similar to early 2007. A Lot Can Change in a Few Quarters So, why bring up a Fed statement from 2007? A lot changed over the course of 2007 and 2008 as the economy fell into the Great Financial Crisis.

One is we were securitizing the assets in the auto loan and selling them off to other asset managers because we weren’t able to buy them ourselves. The requirements for asset managers to have a bank were such that it would inhibit us a bit. JOHNSON: …for most assets. I also ran our credit card business at the time.

One equity market debate discussed frequently in the LPL Research Strategic & Tactical AssetAllocation Committee (STAAC) is the growth vs. value style reversal experienced the past 12 months. Since then, value has outperformed growth for the longest sustained period since 2003–2007. large cap S&P 500 Index. Conclusion.

So it’s, 00:09:11 [Speaker Changed] You’ve become an enterprise, it’s 10 x what it once was in terms of headcount, it’s much bigger in terms of assets. Then what enables that you have to have some asset ability capability that competitors can’t equally duplicate. I do keep a strong balance sheet.

No, I — the first thing I spoke at was a Goldman Sachs Asset Management conference, strange enough in a place called Carefree, Arizona. I was having lunch with Jeremy in the summer of 2007, just after the Bear Stearns hedge fund started blowing up. Jeremy called and said, “Would you like to join the assetallocation team?”

History offers many examples of investors beguiled and then burned by high-yield bonds sold by overleveraged companies, from telecommunications firms in 2000 to homebuilders in 2007 to coal mining companies in 2014. By Taylor Graff, CFA, AssetAllocation Analyst. Anchoring Expectations.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential.

For long-term stock investors who have reaped the massive +520% rewards from the March 2009 lows, they understand this gargantuan climb was not earned without some rocky times along the way.

We found there were two times during the tech bubble that stocks gained 20% and again moved to new lows, and it also happened during the global financial crisis of 2007-2009. It was developed a decade ago and is a key input into our assetallocation decisions.

On the other hand, based on the normal relationship of earnings multiples to interest rates, stocks are meaningfully undervalued relative to bonds and appear to be one of the few asset classes offering the prospect of inflation-beating returns. And is there enough concern over such a prospect to seriously undermine investor confidence?

On the other hand, based on the normal relationship of earnings multiples to interest rates, stocks are meaningfully undervalued relative to bonds and appear to be one of the few asset classes offering the prospect of inflation-beating returns. And is there enough concern over such a prospect to seriously undermine investor confidence?

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Despite the U.S.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Source: BLOOMBERG. . Despite the U.S.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. Some might argue that the Fed’s policy could trigger another crisis as asset prices become overly inflated.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today. Source: Bloomberg.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today. Source: Bloomberg.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) The United Nations Environment Program published a helpful review of key academic and broker reports on responsible investment and performance (UNEP, 2007). Deutsche Asset & Wealth Management White Paper. The Guardian. Available from [link]. Hoepner, A.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) The United Nations Environment Program published a helpful review of key academic and broker reports on responsible investment and performance (UNEP, 2007). Deutsche Asset & Wealth Management White Paper. The Guardian. Available from [link]. Hoepner, A.

The transcript from this week’s, MiB: Ken Kencel, Churchill Asset Management , is below. BARRY RITHOLTZ, HOST, MASTERS IN BUSINESS: This week on the podcast, I have an extra special guest, Ken Kencel of Churchill Asset Management, CEO, Founder, President. This is really a fascinating story. Ken Kencel, welcome to Bloomberg.

Had you invested in Sensex in Dec 2007, the next 10 years returns have been ~6.5-7% Similarly, in Example 5, Sensex was trading at a PE of 28x in Dec 2007, much higher than its long term average of 18x-19x. Investors just earned dividends while capital appreciation was zero. Source: Moneycontrol.com.

No income, no job, no assets were exactly ninja, Sean Dobson : No pulse seems reasonable. We see it as, like I said, about 50 million assets and we’re modeling up the value of every home in the country, every, every week, basically. We’re we’re the quant shop in real estate, in the quant shop in physical assets.

We were talking about luck earlier, got introduced to a local asset manager outside of Boston who saw what I was working on and said, this is really interesting. And so as those assets grew, I’m now a young 20-year-old going out trying to go to other asset managers saying, Hey, I have this quantitative research.

Fisher, 1958 The Money Game - George Goodman, 1967 A Random Walk Down Wall Street - Burton Malkiel, 1973 Manias, Panics, and Crashes: A History of Financial Crises - Charles Kindleberger, 1978 The Alchemy of Finance - George Soros, 1987 Market Wizards - Jack Schwager, 1989 Liar's Poker - Michael Lewis, 1989 101 Years on Wall Street, An Investor's Almanac (..)

In 2007, firms extracted — the private equity firms extracted $20 billion from companies in the form of dividend recapitalizations. Or should this be kept out of private assetallocators’ hands? I think in 2007, we had 24 square feet per capita versus Europe, which was like 14, and Japan, which was like 9.

Recall in 2007, the polls had a head-to-head featuring Rudy Giuliani and Hillary Clinton (neither became their party’s 2008 nominee). Highly dependent on precise phrasing of questions That’s just about basic market, economic, and assetallocation questions. November 2023 polls showed Biden vs Trump.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content