This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

From the fund page : the goal is seeking stable returns across a variety of economic and financial market conditions, consistent with the preservation of capital. There's no fact sheet yet and while the holdings are available, the assetallocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly).

The federal funds rate hasn’t been this high since 2007 when it peaked at 5.25%. Consider your objectives Before making an assetallocation decision, always keep in mind what you’re trying to accomplish. In fact, the Federal Reserve has raised the upper limit federal funds rate by 5% since the beginning of 2022.

As the economy is likely downshifting, investors should take heed that the Federal Reserve’s (Fed) current stance is eerily similar to early 2007. That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change.

And so, coming out of school, I studied Economics and Spanish Literature, and I applied to a — a program that actually targeted Liberal Arts majors. At Citi, in 2007, fantastic timing, you take over as Head of Structured Solutions. And so, 2007, I came over to Citi. It was at Bank One, at the time. BITTERLY MICHELL: Yeah.

Carson’s leading economic index indicates the economy is not in a recession. We found there were two times during the tech bubble that stocks gained 20% and again moved to new lows, and it also happened during the global financial crisis of 2007-2009. It was developed a decade ago and is a key input into our assetallocation decisions.

Through conservative, bottom-up analysis, we are taking advantage of current market dynamics to buy attractively priced debt in companies with solid revenues and limited vulnerability to an economic downturn. Debt in well-managed companies positioned to weather an economic slump return nearly three times the 2.3%

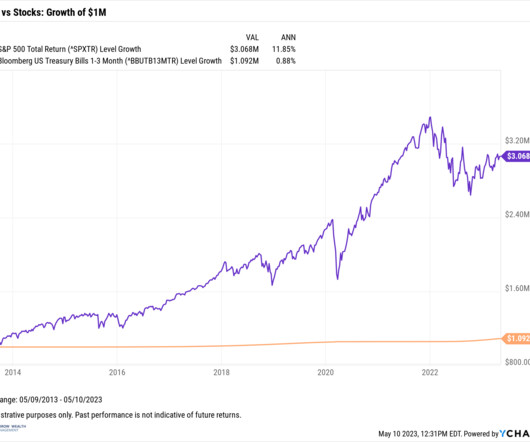

For long-term stock investors who have reaped the massive +520% rewards from the March 2009 lows, they understand this gargantuan climb was not earned without some rocky times along the way.

One equity market debate discussed frequently in the LPL Research Strategic & Tactical AssetAllocation Committee (STAAC) is the growth vs. value style reversal experienced the past 12 months. Since then, value has outperformed growth for the longest sustained period since 2003–2007. Conclusion.

I was having lunch with Jeremy in the summer of 2007, just after the Bear Stearns hedge fund started blowing up. Jeremy called and said, “Would you like to join the assetallocation team?” So he wanted a sort of non-quanty view input into the assetallocation process. CHANCELLOR: Well, I said no initially.

could fall victim to long-term economic stagnation, similar to the fate that befell Japan starting in the 1990s. Japan’s GDP had grown by an average of more than 5% per year from 1950 to 1989—a true post-War economic miracle. As important, however, is the contrast in how the two countries have dealt with financial or economic crises.

could fall victim to long-term economic stagnation, similar to the fate that befell Japan starting in the 1990s. Investors who were active in the late 1980s will recall that asset prices in Japan reached extreme levels as money poured into the country from all over the world, propelled by extraordinary economic growth.

There’s also quantitative metrics that we look at Those have evolved, but always within that capa, that cluster of high returns on investment stability across the economic cycle are consistent and strong balance sheets. And actually Ben Inker is the head of our assetallocation group. We, we call assetallocation at GMO.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to assetallocation decisions and recommendations.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to assetallocation decisions and recommendations.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today.

While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha. Resource and Energy Economics 41:103-121. Journal of Financial Economics.

While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha. Resource and Energy Economics 41:103-121. Journal of Financial Economics.

It’s actually great and especially because you can do some basic kind of assetallocation models, so the robo-advisor… RITHOLTZ: Right. India seems to be like a perennial next economic powerhouse after China and it just always seems to be not catching that next bid. We actually acquired in 2007 a local asset management.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. trillion last year, roughly the same as during the 2007 peak. Then and Now.

So a very different dynamic than we saw back in 2007, 2008, 2009. You raised another $11 billion in capital, despite the economic environment. KENCEL: So I was actually speaking at a conference, the Greenwich Economic Forum last week, where your folks interviewed me, actually. That being said, we stuck to our knitting.

So in this, in this context of, of a mortgage now being clear to everyone that this default risk is present, it’s real, and it’s hard to price because following the borrower’s economic profile, there, there are defaults that are related to just life events, but there’s also defaults related to a macroeconomic event.

And there was one conversation very early in my career, this was actually 2007, where I was interviewing with an asset manager and I pre-meeting, asked them what they thought of the market. There’s very few, I would argue probably no consistent predictors of, of any sort of economic or market cyclicality.

In 2007, firms extracted — the private equity firms extracted $20 billion from companies in the form of dividend recapitalizations. Or should this be kept out of private assetallocators’ hands? I think in 2007, we had 24 square feet per capita versus Europe, which was like 14, and Japan, which was like 9.

Recall in 2007, the polls had a head-to-head featuring Rudy Giuliani and Hillary Clinton (neither became their party’s 2008 nominee). Behavioral economics provides insight into both surveys and modern polling errors). Indeed, polling a year ahead of elections frequently focuses on candidates who do not end up on the ballot.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content