This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The S&P 500 topped out in early October 2007 and bottomed in March 2009. On a price-only basis, the index didn’t reach those 2007 highs again until March 2013: ( Wealth of Common Sense ). • Economic Innovation Group ). • Let’s look at the 2008 scenario as an example. Is Private Credit a Bubble, or Just a Little Frothy?

The first bear I experienced was utterly meaningless economically but still felt bad. My economic future was uncertain, but I felt confident I could make a go of it. From a purely economic perspective, these first few crashes were meaningless. I had zero dollars in the market and was deep in student loan debt.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

How should investors view the relationship between trade policy and inflation in the current economic environment? Gwinn Professor of Economics Masters in Business (coming soon) ~~~ Find all of the previous At the Money episodes here , and in the MiB feed on Apple Podcasts , YouTube , Spotify , and Bloomberg. What was it about?

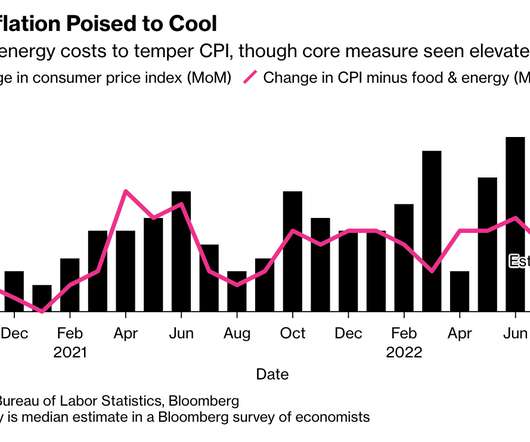

Economic Updates: October Consumer Price Index (CPI) came in at 2.6%. It’s important to consider not just debt but also assets and discretionary income when evaluating the overall financial health of consumers. Overall, consumer balance sheets are in strong shape , especially when compared to the Great Recession (2006-2007).

banks, one in which government bonds would be the “toxic asset” at the center of it all.That’s one of two scenarios being entertained by European global investment manager Eric Sturdza Investments, which managed $1.3 billion across eight funds as of January. The fund manager couldn’t immediately be reached for further comment.“It

They run over $800 billion in client assets, and Kristen’s group, the North American Group, is responsible for about half of the revenue that that massive organization generates. And so, coming out of school, I studied Economics and Spanish Literature, and I applied to a — a program that actually targeted Liberal Arts majors.

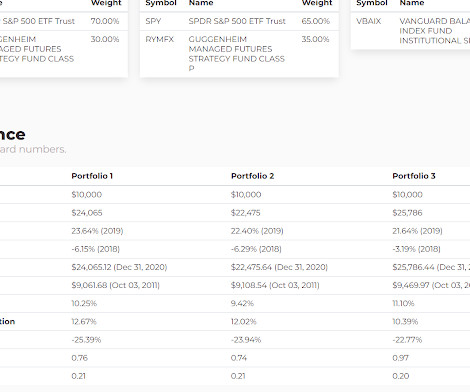

From the fund page : the goal is seeking stable returns across a variety of economic and financial market conditions, consistent with the preservation of capital. There's no fact sheet yet and while the holdings are available, the asset allocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly).

They’re about shaping India’s economic future. Canara Bank – Canara Robecco AMC Canara Bank is set to make waves in the asset management sector with the planned IPO of its mutual fund arm, Canara Robeco Mutual Fund. This IPO could open doors for more people to invest in India’s grassroots economic growth.

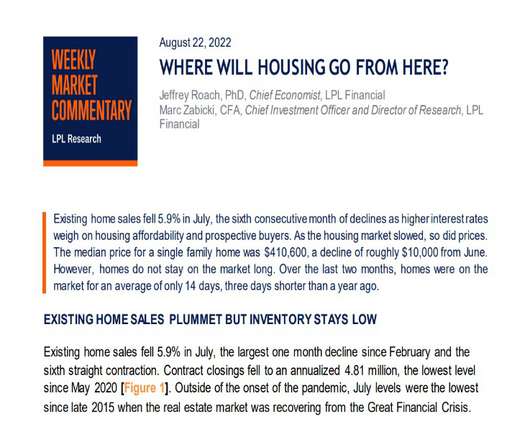

At this rate, home sales will likely continue to slow and residential investment could turn out to be a drag on Q3 economic growth. Outside of the pandemic, the rate of sales were close to sales rates in 2007 and 2008, when the economy was in the depths of a housing crisis [Figure 3]. Regional differences are profound.

When he began, PE was a little bit of a niche boutique sort of investment, and over the ensuing 25 years, it has grown to be really a major asset class with giant opportunities that have been expressed by then small, now very large companies, of which Blackstone is one of the largest. It is an institutionalized asset class.

The federal funds rate hasn’t been this high since 2007 when it peaked at 5.25%. So when the federal funds rate goes up, it can have an outsized impact on shorter term interest rates on assets like Treasury bills (T-bills). This has been the faster pace of rate hikes since the 1980-1981 cycle.

As the economy is likely downshifting, investors should take heed that the Federal Reserve’s (Fed) current stance is eerily similar to early 2007. That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change.

Over and over, Baron writes that he’s seen those companies weather any market storm, coming out better positioned once conditions normalized again, such as through the 1973-74 bear market, the crash of 1987, the 2000-01 dot-com bust, and the financial crisis of 2007-08. “[I]nvest

The chart below shows that the money supply has doubled since 2007, and while prices might be rising in certain areas of the economy like health care and education, nobody would argue that this has been an inflationary environment. Rapid increases or decreases in price lead to economic instability and caused all sorts of social problems.

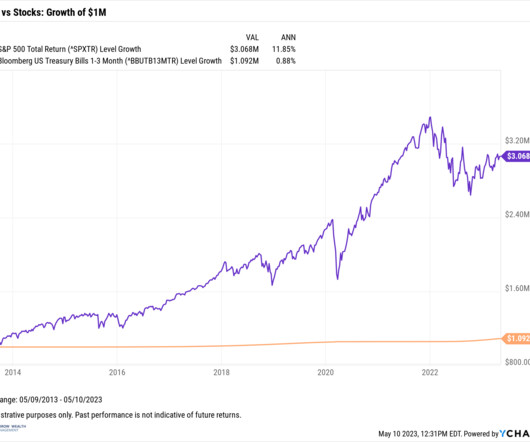

For long-term stock investors who have reaped the massive +520% rewards from the March 2009 lows, they understand this gargantuan climb was not earned without some rocky times along the way.

A bachelor’s in economics from Northwestern and then an MBA from University of Chicago. So, so you’ve held analyst roles and a number of asset managers. And so I had a lot of contacts in Australia at that point, and one of them was the CEO of what was at the time called Colonial First State Global Asset Management.

Through conservative, bottom-up analysis, we are taking advantage of current market dynamics to buy attractively priced debt in companies with solid revenues and limited vulnerability to an economic downturn. Debt in well-managed companies positioned to weather an economic slump return nearly three times the 2.3%

Carson’s leading economic index indicates the economy is not in a recession. We found there were two times during the tech bubble that stocks gained 20% and again moved to new lows, and it also happened during the global financial crisis of 2007-2009. It was developed a decade ago and is a key input into our asset allocation decisions.

So it’s, 00:09:11 [Speaker Changed] You’ve become an enterprise, it’s 10 x what it once was in terms of headcount, it’s much bigger in terms of assets. Then what enables that you have to have some asset ability capability that competitors can’t equally duplicate. I do keep a strong balance sheet.

One equity market debate discussed frequently in the LPL Research Strategic & Tactical Asset Allocation Committee (STAAC) is the growth vs. value style reversal experienced the past 12 months. Since then, value has outperformed growth for the longest sustained period since 2003–2007. large cap S&P 500 Index. Conclusion.

On the other hand, based on the normal relationship of earnings multiples to interest rates, stocks are meaningfully undervalued relative to bonds and appear to be one of the few asset classes offering the prospect of inflation-beating returns. This term refers to the possibility that the U.S. Low interest rates. Source: Bloomberg.

On the other hand, based on the normal relationship of earnings multiples to interest rates, stocks are meaningfully undervalued relative to bonds and appear to be one of the few asset classes offering the prospect of inflation-beating returns. This term refers to the possibility that the U.S. THE “JAPANIFICATION” QUESTION. Source: Bloomberg.

Late in an economic cycle, investors in corporate bonds tend to snap up securities that offer a comparatively high yield but understate the risks of default. From telecommunications companies in 2000, to homebuilders in 2007, to coal mining companies in 2014, recent history offers plenty of cautionary tales for high-yield investors.

While new highs were set before bear markets in 1987, 2000, 2007, and 2020 in recent memory, the market has also made spectacular gains following new highs. According to quarterly Federal Reserve data, money market assets were more than $6 trillion at the end of the third quarter of 2023, roughly double what they averaged from 2011 to 2017.

Of course, getting that timing right is a challenge, but Arnott points to the Shiller price-to-earning ratios, which shows that equities are still expensive and the S&P 500, while trading below its recent peaks, is still well above the low it hit during the 2007-09 financial crisis.

So if you start with the S&P 500 or in this case stocks and bonds, you only have two asset classes, right. So the proper benchmark for those pools has to look a little bit like the underlying assets they’re investing in. If you look at the types of assets that Yale invests in, you can create a benchmark for each pool.

Of course, getting that timing right is a challenge, but Arnott points to the Shiller price-to-earning ratios, which shows that equities are still expensive and the S&P 500, while trading below its recent peaks, is still well above the low it hit during the 2007-09 financial crisis.

The expected competitive forces don’t materialise, and we believe that superior economics can be maintained for a lot longer than our standard microeconomics mean-reversion frameworks would suggest. It is not just Asset Heavy Industries with Capital Cycles The capital cycle is not restricted to asset intensive industries.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. Some might argue that the Fed’s policy could trigger another crisis as asset prices become overly inflated.

Changes in their assumed rate of return can impact decisions ranging from asset allocation to the spending level that a portfolio can rationally support. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential. rather than the 5% that has prevailed since 1985.

Changes in their assumed rate of return can impact decisions ranging from asset allocation to the spending level that a portfolio can rationally support. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential. rather than the 5% that has prevailed since 1985.

As head of asset allocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today.

As head of asset allocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today.

And so we’ve grown from a very small company with 29 partners back in 1979 to, as you noted, over a trillion dollars of assets and it become very diversified. So fixed income is now a substantial percentage of our assets. For, for hedge fund or for, 00:06:29 [Speaker Changed] So that was actually Montgomery Asset Management.

The SSE Composite Index was currently trading at 2982.3755, which is below the all-time high of 6124.0439 reached on October 15, 2007. It is a critical platform for companies to raise financing and for investors to potentially develop their assets. This highlights its importance in reflecting overall economic growth and innovation.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha.

The market is expected to grow to USD 145 billion by FY 2028, driven by economic expansion, rising incomes, and increased gold demand. PNG has implemented BIS hallmarking for gold jewelry since 2007 and ensures certifications for diamond products. Other expenses form around 3.64% of the revenue. In FY23, the EPS was Rs.

Which has in turn triggered the more skittish stock investors to run for the exits and completely change their view of our economic future, flooding the financial news with red ink and scary headlines. Now that we’ve covered the background, we can get into some better news: This is all a normal, healthy part of the economic cycle.

Tiger had gone from a peak of $21 billion in assets in August 1998 to $9.5 He announced that Quantum was down 21 percent for the year and that assets at Soros Fund Management had fallen by $7.6 Druckenmiller "Druckenmiller understood the stock market better than the economists and understood economics better than the stock pickers." "In

I had just gotten married in the fall of 2007. He said, I overpaid for the asset. It’s hard to know which assets are going to have durable value. We’re all, I mean, it’s like a Bloomberg Stream, constantly sharing news analysis, politics, economics, company specific venture capital, because we care.

Obviously, if you’re an investor and you look at either one of these asset classes, and if one substantially looks better than the other, you’ll probably allocate more money to it. Well, what’s that’s set us up for is actually, I haven’t seen the bond market look this good probably since about 2007 or so.

O’Shaughnessy Asset Management, became a leader in direct indexing, eventually was bought by Franklin Templeton, leading him to launch O’Shaughnessy Ventures, O’Shaughnessy Fellowships, infinite Loops podcast, just so many different things. So, the reason I am an economics, I have a degree in economics.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content