This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

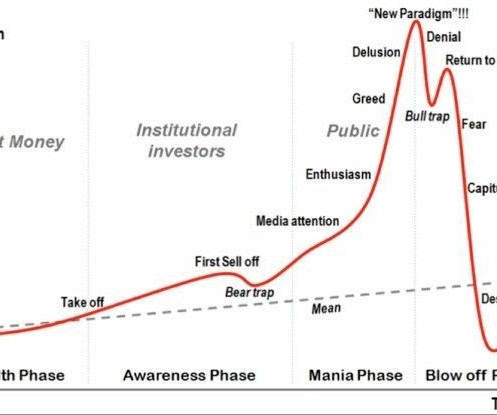

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

Equity markets corrected by more than 50% in 2000-01 and more than 60% in 2007-08 which lasted for 1.5-3 Like the circle of life, good times are followed by bad times, and bad times are followed by good times, stock markets also go through cycles of excessive greed/optimism to excessive fear/pessimism.

He is the Chief Investment Officer of Asset and Wealth Management at Goldman Sachs. He co-chairs a number of the asset management investment committees. trillion in assets under supervision. JULIAN SALISBURY, CHIEF INVESTMENT OFFICER OF ASSET AND WEALTH MANAGEMENT, GOLDMAN SACHS: Thanks, Barry. And I think you will also.

Between the 1970s and 2007, value investing—where investors identify stocks that are trading below their intrinsic value—reigned supreme for two generations of investors. Many investors hopped on his bandwagon and received outstanding returns for decades, until the financial crisis in 2007, the article relates.

This generation’s fortune-teller has been Michael Burry, who called the 2007-2008 housing bubble burst early on. Unlike a lot of pundits, Burry risked his own money on his 2007 housing call and other stock picks that delivered high rewards. His firm Scion bought puts on two popular index funds, betting on a looming downturn.

Canara Bank – Canara Robecco AMC Canara Bank is set to make waves in the asset management sector with the planned IPO of its mutual fund arm, Canara Robeco Mutual Fund. Canara Robeco Mutual Fund, a joint venture between Canara Bank and the Robeco Group since 2007, has shown impressive growth with assets under management worth ₹839.3

O’Shaughnessy Asset Management, became a leader in direct indexing, eventually was bought by Franklin Templeton, leading him to launch O’Shaughnessy Ventures, O’Shaughnessy Fellowships, infinite Loops podcast, just so many different things. Valuations tended to crash and burn very, very cheap valuations tended to do well.

Outside of the pandemic, the rate of sales were close to sales rates in 2007 and 2008, when the economy was in the depths of a housing crisis [Figure 3]. References to markets, asset classes, and sectors are generally regarding the corresponding market index. Sales of existing home in the West were hit hard in July.

So, so you’ve held analyst roles and a number of asset managers. And so I had a lot of contacts in Australia at that point, and one of them was the CEO of what was at the time called Colonial First State Global Asset Management. But there’s always gotta be some element of the valuation really being compelling.

So it’s, 00:09:11 [Speaker Changed] You’ve become an enterprise, it’s 10 x what it once was in terms of headcount, it’s much bigger in terms of assets. Then what enables that you have to have some asset ability capability that competitors can’t equally duplicate. I do keep a strong balance sheet.

The problem is the level of valuations. Popular investment sectors or themes gain momentum as more investors join, driving prices much higher than the worth of the underlying assets. Because it has been a popular narrative for quite some time. But, what’s the problem with investing in popular narratives?

No, I — the first thing I spoke at was a Goldman Sachs Asset Management conference, strange enough in a place called Carefree, Arizona. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. So — CHANCELLOR: Well, yes. CHANCELLOR: Yes and no.

The yield on the ten year Treasury note briefly passed 5% recently, the highest yield on the ten year note since before the financial crisis of 2007 – 2009. Stocks are a risky asset class, subject to periodic bouts of panic selling due to anything from recession-induced earnings fears or geopolitical uncertainty.

Smart investors are very careful about market valuations (prices) and investor behaviour. The chart below illustrates that the smart money enters when valuations are low and the majority of the investors aren’t looking at that asset class or security. How are they prepared for that? They use the principle of margin of safety.

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/31/2007 1.0% 12/31/2007 26.4% And with intangible assets rising in the economy, standard earnings calculations are becoming less and less accurate. By Jack Forehand, CFA, CFP® ( @practicalquant ) —.

As the economy is likely downshifting, investors should take heed that the Federal Reserve’s (Fed) current stance is eerily similar to early 2007. A Lot Can Change in a Few Quarters So, why bring up a Fed statement from 2007? A lot changed over the course of 2007 and 2008 as the economy fell into the Great Financial Crisis.

One equity market debate discussed frequently in the LPL Research Strategic & Tactical Asset Allocation Committee (STAAC) is the growth vs. value style reversal experienced the past 12 months. Since then, value has outperformed growth for the longest sustained period since 2003–2007. large cap S&P 500 Index. Conclusion.

tech in 2000, and more or less everything in 2007. Investor enthusiasm, coupled with high valuations, has preceded all major market bubbles. He writes: The one reality that you can never change is that a higher-priced asset will produce a lower return than a lower-priced asset. You can’t have your cake and eat it.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. Some might argue that the Fed’s policy could trigger another crisis as asset prices become overly inflated.

Large Cap Stocks were the best performing asset class of all nine categories three times and finished second twice. Large Cap was the next asset class under these foreign blue chips. Large caps gained and both international stock asset classes lost ground. large cap stocks in 2003-2007 and underperformance in 2019-2023.

Of course, getting that timing right is a challenge, but Arnott points to the Shiller price-to-earning ratios, which shows that equities are still expensive and the S&P 500, while trading below its recent peaks, is still well above the low it hit during the 2007-09 financial crisis.

While new highs were set before bear markets in 1987, 2000, 2007, and 2020 in recent memory, the market has also made spectacular gains following new highs. According to quarterly Federal Reserve data, money market assets were more than $6 trillion at the end of the third quarter of 2023, roughly double what they averaged from 2011 to 2017.

The yield on the ten year Treasury note briefly passed 5% recently, the highest yield on the ten year note since before the financial crisis of 2007 – 2009. Stocks are a risky asset class, subject to periodic bouts of panic selling due to anything from recession-induced earnings fears or geopolitical uncertainty.

Of course, getting that timing right is a challenge, but Arnott points to the Shiller price-to-earning ratios, which shows that equities are still expensive and the S&P 500, while trading below its recent peaks, is still well above the low it hit during the 2007-09 financial crisis.

While investing in unlisted shares involves higher risks due to limited liquidity and transparency, they often provide more stable valuations. Additionally, we examine the impact of market trends, regulatory changes, and upcoming IPOs on these companies valuations and growth prospects. What are the tax implications for unlisted shares?

And so we’ve grown from a very small company with 29 partners back in 1979 to, as you noted, over a trillion dollars of assets and it become very diversified. So fixed income is now a substantial percentage of our assets. For, for hedge fund or for, 00:06:29 [Speaker Changed] So that was actually Montgomery Asset Management.

So if you start with the S&P 500 or in this case stocks and bonds, you only have two asset classes, right. So the proper benchmark for those pools has to look a little bit like the underlying assets they’re investing in. If you look at the types of assets that Yale invests in, you can create a benchmark for each pool.

Changes in their assumed rate of return can impact decisions ranging from asset allocation to the spending level that a portfolio can rationally support. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential.

Changes in their assumed rate of return can impact decisions ranging from asset allocation to the spending level that a portfolio can rationally support. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential.

I want to get into that before we start talking about asset management. Then the volatility and, and the valuation makes an enormous difference. You joined in 2007, what led you there? We do have multi-asset strategy called balanced, which we launched in 2014 15. Barry Ritholtz] : So you have a fascinating background.

On the other hand, based on the normal relationship of earnings multiples to interest rates, stocks are meaningfully undervalued relative to bonds and appear to be one of the few asset classes offering the prospect of inflation-beating returns. And is there enough concern over such a prospect to seriously undermine investor confidence?

On the other hand, based on the normal relationship of earnings multiples to interest rates, stocks are meaningfully undervalued relative to bonds and appear to be one of the few asset classes offering the prospect of inflation-beating returns. And is there enough concern over such a prospect to seriously undermine investor confidence?

From telecommunications companies in 2000, to homebuilders in 2007, to coal mining companies in 2014, recent history offers plenty of cautionary tales for high-yield investors. When the Great Recession struck in late 2007, earnings evaporated and many companies could not pay off debt. for $45 billion. Energy Futures Holdings Corp.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Despite the U.S.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Source: BLOOMBERG. . Despite the U.S.

As head of asset allocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today. Source: Bloomberg.

As head of asset allocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today. Source: Bloomberg.

PowerGrid was listed in 2007, with GOI currently holding a 51.34% stake in the Company. 9,212 crore and capitalized assets of Rs. The Company currently trades at a PE valuation of 11.73x, which is slightly higher than its peer Maharatnas. It is also India’s largest electrical power Transmission Utility Company. 15,417 in FY23.

S&P500, United States The Standard and Poor’s 500 (S&P 500) is a stock market index used for the valuation of 500 of the largest firms on stock exchanges in the United States. The SSE Composite Index was currently trading at 2982.3755, which is below the all-time high of 6124.0439 reached on October 15, 2007.

Fundamental Analysis of Dixon Technologies : Have you heard about Foxconn, a company that manufactures iPhones for Apple since 2007? After a sixfold jump in two-and-a-half years, it has got a lofty valuation! However, its return on capital employed and return on assets fell short of the ideal requirement. Shareholding.

Tiger had gone from a peak of $21 billion in assets in August 1998 to $9.5 Rational measures of valuation had taken a backseat to “mouse clicks and momentum,” as Robertson put it, and he had no stomach for more punishment. Then the age of the manufacturer arrived and Citadel took off, so that its assets swelled to $13 billion by 2007.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) The United Nations Environment Program published a helpful review of key academic and broker reports on responsible investment and performance (UNEP, 2007). Deutsche Asset & Wealth Management White Paper. The Guardian. Available from [link]. Hoepner, A.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) The United Nations Environment Program published a helpful review of key academic and broker reports on responsible investment and performance (UNEP, 2007). Deutsche Asset & Wealth Management White Paper. The Guardian. Available from [link]. Hoepner, A.

Instead of investing in a productive asset, these speculators were just assuming the recent momentum would continue. True to form, she got back to me within just a few minutes with these thoughts: MMM: How should potential retirees think of the recent crash in valuation – has it really pushed out their retirement date, or not?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content