This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Given the lag between Federal Reserve (Fed) policy and the real economy, we have not likely seen the bottom in the housing market. Outside of the pandemic, the rate of sales were close to sales rates in 2007 and 2008, when the economy was in the depths of a housing crisis [Figure 3]. Regional differences are profound.

Between the 1970s and 2007, value investing—where investors identify stocks that are trading below their intrinsic value—reigned supreme for two generations of investors. Many investors hopped on his bandwagon and received outstanding returns for decades, until the financial crisis in 2007, the article relates.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. And then I was having lunch with Jeremy in Boston.

For a broad view of our expectations for the economy, stocks, and bonds in 2024, download our 2024 Market Outlook. That bear eventually ended in October 2022, and since then stocks have defied many experts, who continually (and incorrectly) touted a weakening economy, tapped-out consumer, and many other reasons to doubt the new bull market.

As the economy is likely downshifting, investors should take heed that the Federal Reserve’s (Fed) current stance is eerily similar to early 2007. During that time, the Fed held a tightening bias since they believed the housing market was stabilizing, the economy would continue to expand, and inflation risks remained.

Canara Robeco Mutual Fund, a joint venture between Canara Bank and the Robeco Group since 2007, has shown impressive growth with assets under management worth ₹839.3 This offering is expected to be one of the largest in India’s corporate history, with a potential valuation exceeding ₹9.3 billion as of December 2023.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Great Financial Crisis October 2007 April 2009 -39.0% at the beginning of the year to 16.6x by year-end. The rise in the 10-year Treasury yield from 1.5% to nearly 3.9% company.

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/31/2007 1.0% 12/31/2007 26.4% And with intangible assets rising in the economy, standard earnings calculations are becoming less and less accurate. By Jack Forehand, CFA, CFP® ( @practicalquant ) —.

for the first time since 2007, while mortgage rates hit 8%–the highest level since mid-2000. Economic Strength, Housing Weakness The economy continued to evidence surprising strength according to data released last week. Yields rose after traders speculated that strong economic data might persuade the Fed to raise rates.

Since then, value has outperformed growth for the longest sustained period since 2003–2007. The monetary factor is the factor we are focused on, as the two periods of sustained value outperformance in the last 20 years (now, and 2003-2007) coincide with the last two periods when both market interest rates (measured by the 10-year U.S.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. economy following the financial crisis. Possible Signs.

And speaking of the.com implosion, like Microsoft via a case study where we, in previous strategies, we held Microsoft for a very long time, that’s where the valuation could help us in the.com bus. 00:21:26 [Speaker Changed] In isolation quality on average gives you downside protection, certainly did in 2007, eight for example.

Of course, getting that timing right is a challenge, but Arnott points to the Shiller price-to-earning ratios, which shows that equities are still expensive and the S&P 500, while trading below its recent peaks, is still well above the low it hit during the 2007-09 financial crisis.

I accept that rising rates means stock valuations have to go lower. this year so at the very least much of the valuation correction is behind us. Growth vs Value March 2000 – December 2007. Growth vs Value October 2002 – December 2007. I accept that U.S. I accept that globalization is likely over.

Of course, getting that timing right is a challenge, but Arnott points to the Shiller price-to-earning ratios, which shows that equities are still expensive and the S&P 500, while trading below its recent peaks, is still well above the low it hit during the 2007-09 financial crisis.

From telecommunications companies in 2000, to homebuilders in 2007, to coal mining companies in 2014, recent history offers plenty of cautionary tales for high-yield investors. The trap often appears when the economy is at the end of its cycle and nearing a downturn. Here are our thoughts on how to avoid such “value traps.”.

stocks powered out of the toxic storm of ever-rising interest rates and inflation into a the spectacular market rebound of 2023 as the prospects of a soft(er) landing for the economy grew more probable. The emerging markets asset class outperformed all others in 2003, 2005, 2007 and 2009, while finishing second in 2004, 2006, and 2012.

Then the volatility and, and the valuation makes an enormous difference. You joined in 2007, what led you there? Their randomness and, and you know, they hit, had a few hits also all the, all the valuation went up right to, to fairly extreme levels. So this is more like the real economy, slower growth businesses.

We know that equity valuations in the U.S. CURRENT VALUATION PREMIUMS, S&P 500 INDEX Metric Most Recent Long-Term Average Premium vs. Average Timeframe Trailing P/E 19.4 CBOE S&P 500 Implied Correlation Index, 1/1/2007-8/30/2019 Source: Chicago Board Options Exchange (CBOE). 17% 3/31/1954- 9/30/2019 Price/Book Value 3.4

We know that equity valuations in the U.S. CURRENT VALUATION PREMIUMS, S&P 500 INDEX. In the years after the 2008-09 financial crisis, securities tended to trade in lockstep with each other as the market focused most of its attention on the big-picture health of the economy. Most Recent. Long-Term Average. Premium vs. Average.

Among the concerns breeding skepticism about the economy and the markets are on-again/off-again trade negotiations, disruption of supply chains, declines in manufacturing activity, and sluggish capital spending. economy that may restrain the country's ability to grow at rates considered normal over the last several decades.

Among the concerns breeding skepticism about the economy and the markets are on-again/off-again trade negotiations, disruption of supply chains, declines in manufacturing activity, and sluggish capital spending. economy that may restrain the country's ability to grow at rates considered normal over the last several decades.

It covers 13 sectors of the Indian economy. S&P500, United States The Standard and Poor’s 500 (S&P 500) is a stock market index used for the valuation of 500 of the largest firms on stock exchanges in the United States. Conclusion In conclusion, The stock market remains a dynamic and vital part of the global economy.

One can argue that today’s low interest rates merit even higher valuations, but there’s no disputing that the increase in price/earnings ratios has been an important driver of stocks since the lows of the early 1980s. Following the 2007–2008 financial crisis, some observers began referring to the “new normal.” company.

One can argue that today’s low interest rates merit even higher valuations, but there’s no disputing that the increase in price/earnings ratios has been an important driver of stocks since the lows of the early 1980s. Following the 2007–2008 financial crisis, some observers began referring to the “new normal.” company.

Liquidity in Public Markets: A Decade of Decline Equity trading volume has declined markedly since the financial crisis (top chart); meanwhile, dealer trading volume relative to the size of the corporate bond universe has fallen from 60% in 2007 to less than 10% today (bottom chart). An index constituent must also be considered a U.S.

Equity trading volume has declined markedly since the financial crisis (top chart); meanwhile, dealer trading volume relative to the size of the corporate bond universe has fallen from 60% in 2007 to less than 10% today (bottom chart). Source: BLOOMBERG. . Source: Federal Reserve Bank of New York. ILLIQUIDITY IMPACTS. company.

And just to amplify everything even further, China has launched a batshit crazy (and medically impossible) “zero covid” policy, locking down hundreds of millions of its own people who can no longer produce or export the things that the rest of the world’s economy had grown to rely upon. the current blowup) -20% so far What’s your guess?

housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today. Additionally, the Australian economy has not experienced a recession since 1991. Valuations are elevated but nowhere near the bubble levels of the late 1990s. GDP than it was 100 years ago.

housing in 2007) or a spike in oil prices (1973, 1980 and 1990)—conditions that are not present today. Additionally, the Australian economy has not experienced a recession since 1991. Valuations are elevated but nowhere near the bubble levels of the late 1990s. GDP than it was 100 years ago.

But at the same time, you can imagine that if rates are going higher because the economy is really good and our profits on our stocks are going up, that effect of higher profits can actually overwhelm the suppressive effect of higher rates. economy actually grew three and a half times. 23:57 So, over this time period, the U.S.

In the last 10 years, 2007 through 2016, Berkshire’s shareholders’ equity per share and share price compounded at roughly 9.3% Since May 2007, Buffett estimated Berkshire had compounded its intrinsic value at roughly 10%, but he thought 10% would be difficult to achieve in the next decade if interest rates stay as low as they are currently.

In the last 10 years, 2007 through 2016, Berkshire’s shareholders’ equity per share and share price compounded at roughly 9.3% Since May 2007, Buffett estimated Berkshire had compounded its intrinsic value at roughly 10%, but he thought 10% would be difficult to achieve in the next decade if interest rates stay as low as they are currently.

I found this to be just a masterclass in everything you need to know about distressed credit investing, private credit, the role of the economy, the fed interest rates, inflation, bottoms up, credit picking, and how to manage a firm and a fund in light of just massive dislocations in your space, as well as the overall economy.

And we’d sort of turn that into a valuation business. MILLER: Well actually I thought, leading up to the great financial crisis, I thought to myself, we’re going to be out of business within a couple of years because nobody wanted an independent valuation. What are the, you know, I’d literally have it in my handheld.

MCCARTHY: And that’s because real estate in strong economies can generate a basically very strong alpha in weaker times or in an inflationary environment we’re in right now. Let’s talk about things that it doesn’t matter necessarily what the economy is doing. RITHOLTZ: Right. Let’s talk about warehouses.

The initial optimism over a Fed pivot has shifted following strong economic data, elevated inflation, and hawkish Fed commentary, sending interest rates higher and valuations lower. The short-covering rally has stalled, as pessimism remains near-universal for institutional investors, and a surge in rates drove skepticism over valuations.

In the short run, there can be distortions in public market valuations as we saw in 2001 and we saw prior to that in 2007, and prior to that in 2000, in ‘99. BARATTA: Wind, solar, electrifying the economy, getting off of oil and gas, and it’s all kinds of companies engaged. BARATTA: Yeah. In the long run. RITHOLTZ: Right.

And we’ve automated the, the appraisal process for valuation, both intrinsic value, meaning like, where would we pay it, where would we buy it, and where is the fair market price that asset from that level, from price and from consumer behavior now. We’ve gathered up all the information you would need to do an appraisal.

The transcript from this week’s, MiB: Aswath Damodaran: Valuations, Narratives & Academia , is below. You’re known as the dean of valuation. He said, oh, dean of valuation, it’s easier to say. So let’s start with the question, what led you to focus on valuation? RITHOLTZ: Right. And I said, why?

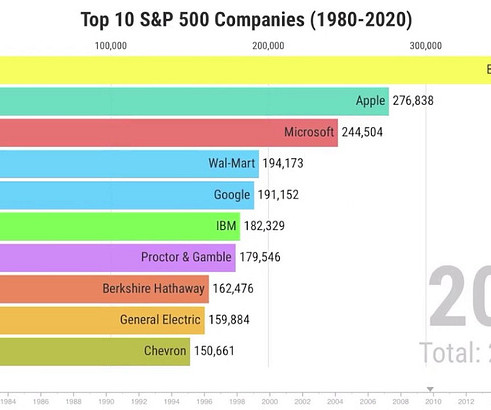

From the tech sector, the top ten included four names, including the entry of Apple (the first-generation iPhone was announced by then–Apple CEO Steve Jobs on January 9, 2007) and Google (which had only come to market in 2004). The broader economy matters. We’ll see what 2030 and beyond bring. Here are ten to start.

My Two-for-Tuesday morning train reads: • Into Perspective: The US Auto Labor Dispute and Recession Worries : Partial work stoppages can impact local economies, but the national effect should be minimal. ( Investors are looking with renewed skepticism at valuations commanded by market leaders. Blame Covid.

I would say the thing that connects them is just voracious curiosity about the world of politics and, you know, economies and trying to make sense out of it. I had just gotten married in the fall of 2007. It was about $170 million valuation. I do think when I look for analysts today, I look for interesting backgrounds.

Patience Investors are generally not a patient breed but the overriding challenge for the broad market is the following: Bloomberg Data Stocks don’t live in a vacuum and most valuation models start with the risk-free rate which is now the highest since 2007. And therein lies the bullish case.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content