This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Following the long run-up in the US equity markets since the bottom of the 2008–2009 financial crisis, many investors with taxable investment accounts have likely found themselves with high embedded gains in their portfolios. While the gains signal portfolio growth, they also create challenges for ongoing management.

I’m generally not a fan of completely rethinking your assetallocation just because you wish you would have invested in something else with the benefit of hindsight. The proliferation of black swan strategies following the 2008 crash comes to mind.

Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. For example during the 2008-2009 market debacle I looked at funds to see how they did in both the down market of 2008 and the up market of 2009.

He is the Chief Investment Officer of Asset and Wealth Management at Goldman Sachs. He co-chairs a number of the asset management investment committees. trillion in assets under supervision. JULIAN SALISBURY, CHIEF INVESTMENT OFFICER OF ASSET AND WEALTH MANAGEMENT, GOLDMAN SACHS: Thanks, Barry. And I think you will also.

The transcript from this week’s, MiB: Mike Greene, Simplify Asset Management , is below. We have to pay attention to this, and we have to understand why this is potentially a risky asset. Precisely because we look at it and we’re like, wait a second, if this risk goes wrong, not only do I lose my assets, but I lose my job.

The transcript from this week’s, MiB: Elizabeth Burton, Goldman Sachs Asset Management , is below. Elizabeth Burton is Goldman Sachs asset management’s client investment strategist. It depends on your assetallocation. And they took it out of their assetallocation in favor of other strategies.

The New York Giants (an old NFL team) won in 2008 and the market tanked in what was the start of the financial crisis. Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. In 1970 the Kansas City Chiefs shocked the Minnesota Vikings and the Dow Jones Average ended the year up slightly. Costs matter.

At some point we are bound to see a stock market correction of some magnitude, hopefully not on the order of the 2008-09 financial crisis. If so, this is a good time to revisit your assetallocation and perhaps reduce your overall risk. As someone saving for retirement , what should you do now? Review and rebalance .

Based on Cambria's other multi-asset funds, ENDW will probably have fixed income duration but that's a space I will continue to avoid. There were places to make money during that run, most notably foreign stocks and equal weight S&P 500, that ETF came out in 2003 and had very good years until 2008. The results.

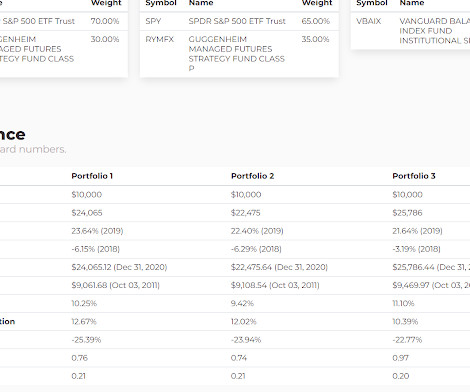

There's no fact sheet yet and while the holdings are available, the assetallocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly). And since the other funds came along, RYMFX has shown to not be such a great representation of the strategy even though it helped in 2008.

On one side you have optimists who have been saying that the US economy remains robust and on the other side you have pessimists who are worried about recession and a potential 2008 scenario. In a way both of these groups have been right. This is not a good risk adjusted return so being less aggressive in recent years has been the right move.

Over the past four weeks, money markets have added $300 billion, on par with surges in 2008 and 2020, bringing the total to a record $5.1 Fund managers remain historically conservative per Bank of America’s Global Fund Manager Survey showing assetallocators long cash and short equities.

Then, the market drops a lot perking up interest in All-Weather and the pendulum swings back to wanting a lot allocated to All-Weather, maybe everything into All-Weather. Reacting in the middle of 2022 after learning too much was allocated to risk assets?

We break down and assign each of the four regions with an asset class and then pick teams (stocks) that we think have the best chance at doing well relative to others. Bonds & Alternatives: The Golden Run Continues If there’s one asset that has stood the test of time, it’s goldand in this market, it has only gained strength.#1

After the subprime crisis in 2008, many developed countries’ Central Banks started printing money and flooding the global economies with cheap liquidity. The liquidity support since 2008 and massive stimulus post March 2020 has inflated all the asset prices be it equity, debt, or real estate. But first a quick recap.

In other words, if you’re 65 in 2007 and 100% invested in stocks and then 2008 happens then you end up going back to work until you’re at least 70. And the only way that disaster happens is if your financial planner is making irrational projections about asset returns and your assetallocation.

And suddenly you could buy index funds that cover all of the major asset classes. And then when I left the journal for the first time in 2008, they said, well, who should we hire to replace you? I did it in 2008 in oh nine. Oh, 00:13:20 [Speaker Changed] That’s hilarious. I said, Jason’s wife.

But the success of managed futures is drawing more and more attention and assets. It's new relative to the last couple of years, the performance has been lights out this year and assets are knocking on the door of $1 billion. It's tough to see on the chart but the stock got a take- under offer in 2008 for less than $4/share.

When all was said and done it fell 1.4%, making today the worst opening day since 2008. What the optimal assetallocation will be over the next twelve months. What the best asset class/sector/stock will be over the next year. The S&P 500 (SPY) opened down 1.66%, fell another 0.95% and then rallied 1.2% into the close.

This fierce competition amongst asset management companies is driving down expense ratios, but investor's are potentially paying higher costs. Large Cap ETFs with over $500 million in assets, which means there will always be something in that category doing better than what you've selected. There are 50 U.S.

Having that much in asset classes that are intended to not look like equities should mean that the long term result won't look anything like the stock market. A 25% allocation to equities for someone who needs equity market growth for their plan to work won't get it done. As bad as 2008 was, we're 3x from there.

Among those voices are Michael Burry, seer of the housing collapse that preceded the 2008-09 financial crisis, and Ray Dalio, who predicted that “the economy will be weaker than expected, and that is without consideration given the worsening trends in internal and external conflicts” in a recent LinkedIn post cited in the article.

Trend following is an investment approach that involves taking positions in positively trending assets. The basic premise is to buy assets that are showing an upward trend and sell or short those that are displaying a downward trend. What is Trend Following?

We break down and assign each of the four “regions” with an asset class and then pick teams (stocks) that we think have the best chance at doing well relative to others. We’ve historically actually been bearish of the shiny metal as it’s simply a non-yielding asset. Treasury Bond ETF ( GOVT ).

Having cash and investable liquid assets gives you flexibility for the unknown. A strong savings rate relative to your income can help you build reserves before retirement—and during retirement, the focus should be maintaining a reasonable and flexible withdrawal rate relative to your investable assets. Assetallocation.

GAA stands for Global AssetAllocation and it has been lagging for 15 years. We spend a lot of time here on how to diversify to try to smooth out the ride and how to hold up better when markets have a year like 2022 or 2008. Here's a great chart to illustrate the point. GAA consistently had smaller drawdowns.

We are currently experiencing one of the most volatile times in decades, on top of the start of the pandemic and the 2008-2009 recession. That’s why, when facing market volatility, stewards of long-term assets held at all types of nonprofit institutions recognize the importance of a well-thought-out investment process. .

For instance, if at the beginning of 2008, you knew that they would drop 77.5%, a 38.5% Make sure your assetallocation is appropriate. Strike the right balance of having enough risk assets that you don't chase in a good market, but also not too much that you sell in a lousy market. decline would have been avoided.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. Take Europe, for instance.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. We maintain a model portfolio internally to track the results of our assetallocation stances. Thu, 06/01/2017 - 02:47.

So it’s, 00:09:11 [Speaker Changed] You’ve become an enterprise, it’s 10 x what it once was in terms of headcount, it’s much bigger in terms of assets. I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular.

Today I want to talk about practical tactical assetallocation. Pretty much the same thing happened in 2008. The behaviorally aware investor has a plan in place to insulate themselves from their worst instincts, which is to sell everything when stocks decline and buy back only when "the dust has settled," whatever that means.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. Diversification does not protect against market risk.

Ahead of the first tightening by the Federal Reserve in nine years, we are shifting into less-traditional assets, anticipating that, at best, U.S. In anticipation of the policy switch, we have reallocated across a wide range of asset classes in an effort to limit risks and seize new opportunities. The Advisory | June 2015.

That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change. A lot changed over the course of 2007 and 2008 as the economy fell into the Great Financial Crisis. References to markets, asset classes, and sectors are generally regarding the corresponding market index.

We work with clients to create—either in writing or verbally—a “mission statement” detailing how they want their assets to serve their well-being in coming decades. The “core” allocation is made up of a mix of assets aimed at stability and growth. By Taylor Graff, CFA, AssetAllocation Analyst.

built up substantial reserve capital while recovering from the Great Recession in 2008-2009. By Taylor Graff, CFA, AssetAllocation Analyst. We are recommending that clients consider high-yield bonds and other asset classes that can offer the prospect of solid gains that diverge from the path of traditional stocks and bonds.

Low interest rates have also played a major role to push people towards speculative asset classes. Poor suffer the most from the impact of inflation since they have very low exposure to assets whereas food & fuel accounts for a major part of their household budget. The debt as a percentage of overall GDP has risen sharply.

But, as I said, there was something else, more critical and important, that I had never been able to articulate until I read a recent white paper by the nebo wealth organization ( www.nebowealth.com ) called “The Perils of Outsourcing AssetAllocation to a Risk Score.” You can actually test various bear markets and adjust accordingly.)

Here's a table of failure rates of various assetallocations and withdrawal percentages from an article at Return Stacked Portfolio Solutions. The funds offer 100% to the traditional asset and 100% to managed futures. Here's well known expert Wade Pfau calling for 3%.

It took the Nikkei over 34 years to surpass its previous record peak, which was last achieved in 1989 when Japan experienced a massive bursting of an asset bubble. What’s the big difference between these two indexes simultaneously surpassing a record 39,000 in the same month? The same concept holds true for investing.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Low rates are generally good for stocks, as they tend to drive investors into riskier asset classes with higher return potential.

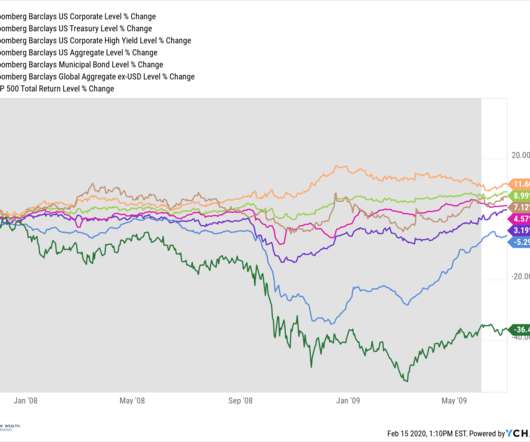

during the month, which was the best month for core bonds since December 2008. The Strategic and Tactical AssetAllocation Committee’s (STAAC) S&P 500 year-end fair value target of 4,000-4,100 is based on a price-to-earnings ratio of 17.5 Core bonds, as measured by the Bloomberg Aggregate Bond index, were up 3.7%

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content