This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

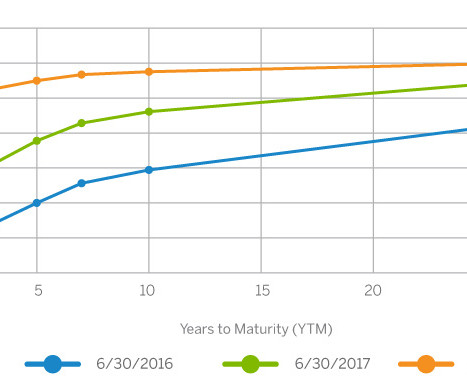

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. Take Europe, for instance.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. We maintain a model portfolio internally to track the results of our assetallocation stances. Thu, 06/01/2017 - 02:47.

It was developed a decade ago and is a key input into our assetallocation decisions. It declined ahead of the actual start of the 2001 and 2008 recessions. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financialservices.

2018 marked the 10-year anniversary of the depths of the 2008–09 financial crisis, an event that tested the strength of the global financial system, the will of the global body politic, and the mettle of everyday citizens throughout the world. This is also a fitting moment to review the intersection of risk and valuation.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to assetallocation decisions and recommendations.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. Our Investment Solutions Group spends considerable time trying to gauge the long-term outlook for stocks since it is central to assetallocation decisions and recommendations.

While the role of bonds since the financial crisis of 2008-09 has been more about reducing portfolio risk and less about producing incremental profit (although returns have generally been positive), that role may be changing in favor of relative returns. (Let’s hope we’re wrong, but we prefer to be surprised on the upside.)

While the role of bonds since the financial crisis of 2008-09 has been more about reducing portfolio risk and less about producing incremental profit (although returns have generally been positive), that role may be changing in favor of relative returns. (Let’s hope we’re wrong, but we prefer to be surprised on the upside.).

The background liquidity conditions for capital markets have changed substantively since the 2008-09 financial crisis, and to some extent these changes have contributed to the liquidity crunch in various segments of the market in the wake of the coronavirus outbreak. As we now know, this celebration was premature.

The background liquidity conditions for capital markets have changed substantively since the 2008-09 financial crisis, and to some extent these changes have contributed to the liquidity crunch in various segments of the market in the wake of the coronavirus outbreak. RECENT TRENDS AFFECTING LIQUIDITY.

And again, I ended up in the financialservices audit practice at KPMG. And then I moved back to London at the end of 2008, which was a really interesting pivot. At the end of 2008, we owned a lot of illiquid assets. And there was a problem with 168 of them at the end of 2008. I finished the three years.

You know, that’s one thing in Europe where London was, I actually think, still remains the one place where you want to get exposure when you join financialservices. RITHOLTZ: (LAUGHTER) CHABRAN: And find a reason why they would allocate there. Because London remains a critical business center for financialservices.

In late 2008, Dent published another book, The Great Depression Ahead: How to Prosper in the Crash Following the Greatest Boom in History , moving into the “doom and gloom” business. .” who became a professor at the University of Michigan before setting up his own asset management firm. He missed this one, too.

So Bernanke made that point back in 2008. DUTTA: So — RITHOLTZ: I recall deep into 2008, there was still an argument as to whether or not when we were in recession, when it started six, eight months earlier. DUTTA: Well, I can remember one analyst famously thinking that the Fed was going to be hiking in the back half of 2008.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content