This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

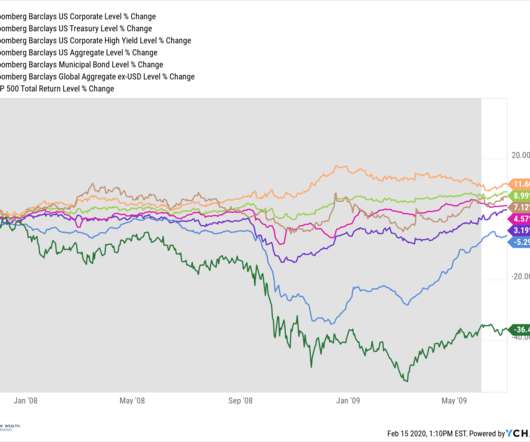

Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risktolerance. For example during the 2008-2009 market debacle I looked at funds to see how they did in both the down market of 2008 and the up market of 2009. Focus on risk.

For more years than I’d care to name, I’ve been trying to put my finger on exactly why I have a such a huge problem with the traditional (Think: Riskalyze, now Nitrogen) risktolerance assessments in the financial planning profession. You can actually test various bear markets and adjust accordingly.)

The New York Giants (an old NFL team) won in 2008 and the market tanked in what was the start of the financial crisis. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Perhaps it’s time to rebalance and to rethink your ongoing assetallocation. Costs matter.

At some point we are bound to see a stock market correction of some magnitude, hopefully not on the order of the 2008-09 financial crisis. If so, this is a good time to revisit your assetallocation and perhaps reduce your overall risk. Manage your portfolio with and eye towards downside risk. Click To Tweet.

And then I moved back to London at the end of 2008, which was a really interesting pivot. At the end of 2008, we owned a lot of illiquid assets. And there was a problem with 168 of them at the end of 2008. It was the year I made partner, actually, in 2008. I did that for a couple of years. SALISBURY: Absolutely.

The key to weathering the storm is having a diversified assetallocation that’s truly aligned with your risktolerance and appetite before there’s a personal financial problem or other negative event. Assetallocation. Don’t wait for volatility to get your investments in order!

Regardless, the goal of long-term investing is to master the art of maximizing returns and limiting taxes subject to your risktolerance. In a diversified portfolio that that takes account of your risktolerance, we strongly believe low-cost, tax-efficient, long-term investing is the best way to create your retirement masterpiece.

We work with clients to create—either in writing or verbally—a “mission statement” detailing how they want their assets to serve their well-being in coming decades. This includes articulating a policy with regard to investment risktolerance, long-term goals, cash flow needs and sector diversification.

My family and I moved to McLean, Virginia in, in 2008. So we were down the street and we were in a pretty interesting situation because we were the, we were one of the biggest, if not the only investment bank specializing in the core risk that the nation was facing. They’re assetallocation model driven folks.

But our belief is that this economic and profit environment is better than in the early 1990s, early 2000s, or 2008-2009 and therefore supports higher valuations. We continue to recommend an overweight allocation to equities and underweight to fixed income relative to investors’ targets, as appropriate.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content