This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The sentiment is especially poignant when it comes to economic forecasting, as it's nearly impossible to get an accurate picture of the current state of the economy at any given moment. Moreover, historically extreme valuations in a small handful of mega-cap stocks that account for about 30% of the market weight in the S&P 500 (i.e.,

stock market has, on average, outperformed international equities over the last 15 years since emerging from the Great Recession of 2008, many investors argue that international diversification is a poor allocation of dollars that would otherwise be earning more in the U.S. Given the current (as of March 2023) economic positions for the U.S.

Since 2008, the Census Bureau has included government transfers in its Supplemental Poverty Measure. Or is anything economic Phil Gramm touches simply destined to be a dumpster fire of lies, foolishness, and incompetency? ” In 2008. It is untrue. Sheer stupidity? You may remember Phil Gramm.

Articles Ultra-low interest rates make the economics of using cheap debt to buy small companies at a low valuation and selling them at a higher one look pretty attractive. By Howard Lindzon) Millennium has generated an average calendar-year return of 14% for the past 33 years, with only one loss year in 2008. (By Marc Rubins.

Historically, this bracket has been dominated by the tech sector, but after years of outsized gains, big tech valuations are stretched. However, shifting economic conditions, a potential rate-cut cycle, and valuation opportunities have created a renewed focus on small and mid-cap stocks, particularly in financials and energy.

His model is both conservative and disciplined, focusing on balance sheet strength and attractive valuations. Low Debt Levels (Long-Term Debt Net Current Assets) Limiting debt helps safeguard a companys financial health, especially during economic downturns. Example : A P/B ratio of 1.3 combined with a P/E of 11.1

Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. While some of that outperformance was due to improving fundamentals and earnings, most of it the returns came from the valuation investors assigned to these stocks. Source: [link]. The yellow metal then saw two positive years.

Paul Singer, founder of Elliott Management and well-known for predicting the financial crisis of 2008, calls the current environment “an extraordinarily dangerous and confusing period,” in an interview with The Wall Street Journal. But for long-term prosperity in the U.S.

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

DOWNLOAD OUR 2024 MARKET OUTLOOK The Macroeconomic Backdrop As we look to the year ahead, our proprietary Leading Economic Index (LEI) indicates even lower odds of a recession than 2023. Our Market Views This economic environment should support solid earnings growth and improved margins, leading to a good year for markets.

At this rate, home sales will likely continue to slow and residential investment could turn out to be a drag on Q3 economic growth. Outside of the pandemic, the rate of sales were close to sales rates in 2007 and 2008, when the economy was in the depths of a housing crisis [Figure 3]. Regional differences are profound.

Pockets of attractive valuations exist despite above-average valuations in some high-profile areas of the market. These include some of the worst years in stock market history, including 1973, 1974, the tech bubble, 2008, and 2022. Following the huge 11.2% The full year and the following three quarters’ returns were much weaker.

With the Fed swiftly raising rates and the slowing of economic growth, small-cap stocks have gotten pummeled. That’s positive news for small-caps, especially as the pattern of underperforming before a recession and outperforming as a recession wanes is one that small-caps have followed in 1990, 2001, 2008, and 2020.

TROPIN: And then we meet every day at 9:30 and have since 2008, to look at every trader’s portfolio, how has it changed since the previous day? How do you contextualize the economic data and the broad stamp recession when you’re thinking about managing risk? How does this impact global trade and other economic factors?

By Joe Nocera Entering into a crisis is not the time to figure out what you want to be By Jamie Dimon This burgeoning mass of defined-contribution assets will be ground zero for the upward redistribution of equity assets By William Bernstein The scars of 2008 run deep, not just for economic policymakers but also for their critics By George Pearkes (..)

Since the 2008–09 credit crisis, market sentiment on European stocks has shifted back and forth, from despair to confidence, depending largely on sentiment regarding the EU’s prospects as a viable political and economic entity. Take Europe, for instance. is not particularly notable. stocks since the middle of 2004. is much clearer.

Since the 2008–09 credit crisis, market sentiment on European stocks has shifted back and forth, from despair to confidence, depending largely on sentiment regarding the EU’s prospects as a viable political and economic entity. Take Europe, for instance. is not particularly notable. stocks since the middle of 2004. is much clearer.

The Fed has held the benchmark federal funds rate at zero—a record low—since December 2008 and further reduced borrowing costs through so-called quantitative easing, a bond-purchase program that more than quadrupled its balance sheet to $4.5 The economic expansion is weak and inflation is still below the central bank’s 2% target.

Commentators continue to shout the doom-and-gloom forecasts of a hard landing recession, but after an economic hurricane in 2022 there are some signs the financial clouds have begun to lift this year. Investors Waiting for Another Flood While the calls for a hard economic landing remain, healthy GDP growth ( +2.9% 1, 2023).

So far, this year hasn’t seen a full-blown crisis like 2008–2009 or 2020, but the ride has been very bumpy. Understandably, rising prices, slowing economic growth, and a challenging first half for both stocks and bonds have many investors on edge, and fatigue from more than two years of COVID-19 measures doesn’t make it any easier.

Later in the year, markets became anxious about other topics, such as a potential economic slowdown, a new level of dysfunction in Washington (including unusual executive challenges to the Fed's independence and an extended partial government shutdown), and escalating trade disputes between the U.S. equity exposure.

The hangover from COVID has created significant supply chain disruptions and widespread economic shortages. Source: Trading Economics. The rising Baker Hughes drilling rig count below reflects the miracle of supply-demand economics operating in full force. Source: Trading Economics. Source: GasBuddy.com.

After the subprime crisis in 2008, many developed countries’ Central Banks started printing money and flooding the global economies with cheap liquidity. The quantum of money printing jumped massively after Corona-led economic shutdowns. But first a quick recap. US Fed increased its balance sheet size from ~$4-4.5 trillion to ~$8-8.5

They’re about shaping India’s economic future. This offering is expected to be one of the largest in India’s corporate history, with a potential valuation exceeding ₹9.3 This IPO could open doors for more people to invest in India’s grassroots economic growth. trillion ($112 billion).

However, since 2008, the stock market has generally been on a consistent tear racking up a record of 10 wins, 2 losses (2015 and 2018), and one tie (2011). stock market by China with its zero-COVID policy, which has essentially shut down the world’s 2 nd largest economy and further delayed the full reopening of the global economic game.

Most valuation models start and end with the risk-free rate and any movement or even the perception of a change in future policy has an enormous impact on multiples and with-it equity prices. Morningstar is on record saying they expect 2023 to end with a fed funds rate of 1.75% well below where the rest of the street. and today is over 41%.

The challenges are many, with intense cost pressures and slowing economic growth at the top of the list. These headwinds include slower economic growth, cost pressures amid high inflation, ongoing supply chain issues, geopolitical instability in Europe and Asia, and significant currency drag from a very strong U.S. Numerous Headwinds.

Memories of 2008-2009 are still vivid even though global banks, overall, are in much healthier shape due to stringent regulations put in place following the crisis. The British pound had been weakening for some time amid a backdrop of dollar strength and a poor economic outlook as the U.K. has been wracked by rising energy costs.

That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change. Along with the statement, the Committee updated the Summary of Economic Projections (SEP), which is arguably more important than the brief monetary policy statement.

I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular. You really like the long time where you have to hold to make up that valuation whole is so long that you just really shouldn’t be involved. 00:18:41 [Speaker Changed] Yep.

I had my first child in June of 2008. Now, the first half of 2008, I was doing pretty well in the fund. But of course, I didn’t know the world was gonna meltdown in 2008. I bought Priceline on November 1st, 2008. And we would go on to sell that business to Microsoft in 2008. I think I was up 20 or 25%, right?

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. It’s remarkable how far the markets have come in the five years since then. Possible Signs. Then and Now.

Market strategists and pundits make the relationship between recessions and the stock market seem binary, but each economic contraction is different and has different effects on earnings. First, keep in mind that stocks tend to look forward by four to six months and can provide warnings of changing economic conditions. How can this be?

And when I was studying in university economics, I did not really get the passion. But it was — on the other hand, it was just a great place, well, first to try it but the second thing is when 2008 came along, it was one of the few places that we’re making money. But it just didn’t become a great success.

Get money rich (GMR) blog is run by Mani (founded in 2008). He teaches MBA students (at MDI Gurgaon) two popular courses: “Behavioral Finance & Business Valuation” and “Financial Shenanigans & Governance”. You can also learn about stock market investing in Trade Brains’ recently launched android mobile app.

.: Grantham, who is well-known for identifying bubbles before they burst such as the dot-com bust in 2000 and the housing market crash in 2008, has been outspoken about his belief that the market was in a “super bubble” that has yet to truly burst. Valuations are still high, despite rampant inflation and an economic slowdown.

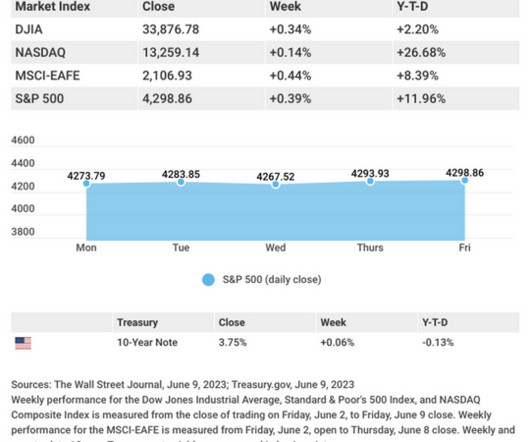

6 This Week: Key Economic Data Tuesday: Consumer Price Index (CPI). Source: Econoday, June 9, 2023 The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. So, in 2008, the U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. From an economic perspective, growth in the U.S.

We tend to be strategic rather than tactical in our approach to investing, but a combination of recent fundamental developments and valuation changes has caused us to add a note of caution in conversations with clients and in the management of their portfolios. From an economic perspective, growth in the U.S. Incremental Equity Risks.

falls into recession, the chances are it would occur during the first half of 2023 and will not likely be as deep as the 2008 recession, which was initiated by a fundamentally flawed financial market. Much depends on China’s growth path now that it has largely abandoned its overzealous Zero-COVID-19 policy. If the U.S.

The median performance, at 25.4%, is a better representation of where stocks might normally be at this stage because it takes out the ferocious V-shaped rebounds coming out of the 2008-2009 Great Financial Crisis and the early stages of the pandemic in March 2020. At the same time, the resilience of the U.S. All index data from FactSet.

This is not good for economic growth. The sharp market decline of 2022 was pricing in a potential 2008 type outcome, but a lot of the economic data has come in better than expected. This isn’t 2008, but it also isn’t a return to the boom period. Of course, this doesn’t mean you should abandon ship.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. While no two downturns are the same, we believe this approach can again be effective in the current period. Intra-family Note Refinance.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets. While no two downturns are the same, we believe this approach can again be effective in the current period. Outright Gifting.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content