This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In 2008, he received the George Polk Award for financial reporting. We discuss Chancellor’s history as an analyst interested in speculative bubbles, which led him to write a research paper on valuations and why the dotcom bubble looks a lot like other historical bubbles.

The sentiment is especially poignant when it comes to economic forecasting, as it's nearly impossible to get an accurate picture of the current state of the economy at any given moment. As a result, uncertainty about how the economy may unfold, even along the shortest time frames, is the default.

Markets Market valuations are a lot more attractive than they were a year ago. axios.com) Mortgage rates are at their highest level since October 2008. finance.yahoo.com) Economy Auto loan delinquencies are on the rise. blog.validea.com) Visualizing U.S. interest rates since 2020.

On one side you have optimists who have been saying that the US economy remains robust and on the other side you have pessimists who are worried about recession and a potential 2008 scenario. In our view we’re still in the “muddle through” camp as it pertains to the economy.

economy continues to look solid, with markets rallying Friday after a stronger-than-expected jobs report. Pockets of attractive valuations exist despite above-average valuations in some high-profile areas of the market. economy, and the job market is leading the way. Payroll growth picked up in recent months.

I led the Union Square Ventures investment in Etsy, I became a venture partner for that, and then became a GP in the 2008 fund. So along those lines, there are some venture firms that don’t really seem to care a lot about valuations and others seem to focus on a little bit. A year ago, late stage valuations had gone just bonkers.

Historically, this bracket has been dominated by the tech sector, but after years of outsized gains, big tech valuations are stretched. However, shifting economic conditions, a potential rate-cut cycle, and valuation opportunities have created a renewed focus on small and mid-cap stocks, particularly in financials and energy.

We believe the odds of a recession remain low, with continued income growth, a recovery in rate-sensitive cyclical areas of the economy, and untapped potential for productivity gains helping to support the expansion. Market participants, strategists, policymakers, and the economy rarely saw eye to eye. We continue to favor the U.S.,

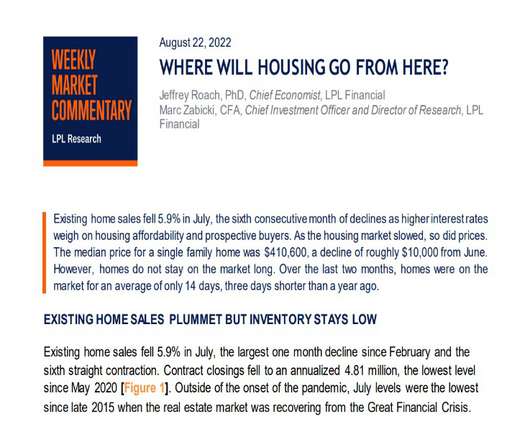

Given the lag between Federal Reserve (Fed) policy and the real economy, we have not likely seen the bottom in the housing market. Outside of the pandemic, the rate of sales were close to sales rates in 2007 and 2008, when the economy was in the depths of a housing crisis [Figure 3]. Regional differences are profound.

These recurring shifts in the composition of the benchmark stock Index can offer insight into how different factors, such as cyclicality, long-term growth potential, and valuation, may impact stock performance in the future. This is a significant increase from 1990, when the tech sector comprised just 6.3% of the Index.

No central bank has ever wound down such massive stimulus, so the potential impact on the economy and financial markets is not clear. The easing helped stabilize financial markets, reduced the risk of deflation and resuscitated the economy and job growth. equity market: With the economy stable, the investor mood remains sanguine.

Paul Singer, founder of Elliott Management and well-known for predicting the financial crisis of 2008, calls the current environment “an extraordinarily dangerous and confusing period,” in an interview with The Wall Street Journal. government debt which now has a solid return thanks to the inverted yield curve.

Articles If private equity suffers, the blow will reverberate throughout the entire economy By Bethany McLean No one runs a business on the assumption that that business won’t be there tomorrow By Tim Duy The government made more than $13 billion from its bailout of Citigroup, $5 billion on its stake in AIG, $4.5

What the naysayers miss is that each market downturn created lowered valuations that resulted in “above-average returns,” the article quotes Doug Foreman of Kayne Anderson Rudnick. And Jeremy Siegel, perennial bull, has long said that equities will always be a winner, no matter what is going on with the economy.

But that valuation, to be able to come up with the valuation, to be then able to work in a restructuring process, bankruptcy process, and say, Hey, I think at the end of this, we are buying debt at 50 cents. Or was it just generally across the economy? By the time 2008 came around, we had about $5 billion.

in Q4 ), generationally low unemployment (3.5%), and relatively stable earnings (see chart below) all point to a stable economy with the ability to navigate a soft landing. China’s new reopening of the economy and Europe’s seeming ability of dodging a recession provide additional evidence for a soft landing scenario.

This offering is expected to be one of the largest in India’s corporate history, with a potential valuation exceeding ₹9.3 Jio’s market debut could have far-reaching implications for India’s digital economy and telecom sector, potentially attracting global attention and investment. trillion ($112 billion).

After the subprime crisis in 2008, many developed countries’ Central Banks started printing money and flooding the global economies with cheap liquidity. The liquidity support since 2008 and massive stimulus post March 2020 has inflated all the asset prices be it equity, debt, or real estate. But first a quick recap.

However, since 2008, the stock market has generally been on a consistent tear racking up a record of 10 wins, 2 losses (2015 and 2018), and one tie (2011). Theoretically, QT should cause interest rates to move higher, all else equal, and thereby slow down growth in the economy, and help tame out-of-control inflation. Impeachment.

Since the 2008–09 credit crisis, market sentiment on European stocks has shifted back and forth, from despair to confidence, depending largely on sentiment regarding the EU’s prospects as a viable political and economic entity. Further, we see room for the European economy to grow. Take Europe, for instance. is much clearer.

Since the 2008–09 credit crisis, market sentiment on European stocks has shifted back and forth, from despair to confidence, depending largely on sentiment regarding the EU’s prospects as a viable political and economic entity. Further, we see room for the European economy to grow. Take Europe, for instance. is much clearer.

counterparts for months, fueled by a weakening dollar, appealing valuations, and the reopening of China’s economy, the article contends. And the divide between ETF sales and individual stock purchases this year is the widest it’s been since 2008, according to analyses from Bank of America that is cited in the article.

IBM loses to QCOM based on valuation. Obviously this rattled a lot of nerves and the way we see it is that it won’t be a 2008 “Lehman” type event, however there will be other casualties or at least some banks that get major pressure. Watch for those that have even worse financials and balance sheets than SVB did.

People forget that commodity prices approximately doubled after the 2008 Financial Crisis, only to experience a subsequent slow bleed over the next decade until prices were essentially chopped in half. The Fed’s goal is to increase the cost of borrowing, thereby slowing down the economy and reducing inflation. Source: Yardeni.com.

For a broad view of our expectations for the economy, stocks, and bonds in 2024, download our 2024 Market Outlook. That bear eventually ended in October 2022, and since then stocks have defied many experts, who continually (and incorrectly) touted a weakening economy, tapped-out consumer, and many other reasons to doubt the new bull market.

Such rate cuts have been de rigueur during the dot-com bubble burst and the 2008 financial crisis, but the Fed appears to finally be shifting the market away from Fed-put expectations. That, in turn, bloated stock valuations. Just days after the Federal Reserve Bank of New York orchestrated a $3.5

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/31/2008 2.1% 12/31/2008 24.9% And with intangible assets rising in the economy, standard earnings calculations are becoming less and less accurate. By Jack Forehand, CFA, CFP® ( @practicalquant ) —.

Memories of 2008-2009 are still vivid even though global banks, overall, are in much healthier shape due to stringent regulations put in place following the crisis. If an economy needs to see inflation easing, it makes little sense to stimulate the economy through tax cuts while tightening monetary policy by raising interest rates.

Mega-cap tech giants, a safe haven since the 2008 financial crisis, fell much more than the S&P 500 in 2022. There are many reasons for the tech sector’s woes aside from higher interest rates, from the potential energy crisis in Europe, wage pressures, and a slowdown in the global economy, as well as geopolitical tensions.

He brings a fascinating approach and a bit of an outlier, contrarian way of looking at the world that has allowed him to identify specific changes in what’s taking place in the economy, in the markets, and essentially provide a helpful sounding board to many of the world’s best investors. MIAN: Valuations are ebb and flow.

economy is in or about to enter recession, so we thought a piece on what a recession might mean for the stock market would be of interest. economy is not currently in recession, odds are still perhaps a coin flip or better that one may come in the next year. While Friday’s strong jobs report provides more evidence that the U.S.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. This is also a fitting moment to review the intersection of risk and valuation. Entering 2019, we face rising economic, political and market risks. In non-U.S.

As the economy is likely downshifting, investors should take heed that the Federal Reserve’s (Fed) current stance is eerily similar to early 2007. During that time, the Fed held a tightening bias since they believed the housing market was stabilizing, the economy would continue to expand, and inflation risks remained.

In Engines That Move Markets, a 2002 book about the cycles of technology investing, Alasdair Nairn defines “bubbles” as periods when investors appear to suspend rational valuation, much as they had during the dotcom craze shortly before the book was published. economy following the financial crisis. Possible Signs.

And so in the 1990s, I developed the, the late 1980s, early 1990s, I developed a skillset around valuation, in particular discounted cash flow or residual income type models, along with a couple of peers out of the consulting industry. There’s a continual, the economy continues to grow. It goes so far. Did you give me cash?

During the worst of the Financial Crisis (Q3 2008 through Q1 2009), more than 50% of S&P 500 companies hit their earnings targets each quarter. economy in mid-March, 62% of S&P 500 companies beat estimates, and aggregate earnings were within one percentage point of expectations. Quincy Krosby , Ph.D.

Topic 1: Economy Bull case: Consumer is resilient, the labor market is strong, wages are rising, and inflation is coming down steadily. Background: The global economy will likely slow from the upper-2% range in 2022 down to slightly above zero in 2023 ( Figure 1 ). Call us cautious bulls. If the U.S. Our take: The U.S.

I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular. You really like the long time where you have to hold to make up that valuation whole is so long that you just really shouldn’t be involved. 00:18:41 [Speaker Changed] Yep.

.: Grantham, who is well-known for identifying bubbles before they burst such as the dot-com bust in 2000 and the housing market crash in 2008, has been outspoken about his belief that the market was in a “super bubble” that has yet to truly burst. Valuations are still high, despite rampant inflation and an economic slowdown.

RIEDER: — there was — and then, you know, punctuating with obviously 2008. I try to analyze the economy from the top. the economy is stabilizing, China is growing. and maybe the economy is coming off, the central bank, not in ‘23, but will start to ease. Where do you want to be in sector? Probably not.

stocks have generally been clear outperformers since the 2008-09 financial crisis, and it hasn’t really been close: Over the ten years since the financial crisis, U.S. stocks have reigned since the global financial crisis of 2008-09. Equity valuations in Europe at the time were more attractive than those in the U.S.

stocks have generally been clear outperformers since the 2008-09 financial crisis, and it hasn’t really been close: Over the ten years since the financial crisis, U.S. stocks have reigned since the global financial crisis of 2008-09. Equity valuations in Europe at the time were more attractive than those in the U.S.

At the aggregate level the system actually relies on expansion of both sides of the balance sheet and in sustainable economies this results in real asset creation (ie, non-financial and financial net worth increases). As we mentioned before, you need balance sheets to expand for the economy to expand.

.: Grantham, who is well-known for identifying bubbles before they burst such as the dot-com bust in 2000 and the housing market crash in 2008, has been outspoken about his belief that the market was in a “super bubble” that has yet to truly burst. Valuations are still high, despite rampant inflation and an economic slowdown.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content