This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives.

The only other years with a higher reading since 1990 were 2008 when the S&P fell 38%, and 2002, when it fell 23%. Why Jack Welch Wouldn’t Cut It Today : Bill George, a legendary CEO in his own right, says good quarterly numbers aren’t necessarily indicative of strong leadership. Wealth of Common Sense ). • Wall Street Journal ).

In the mid-20th century, the first phone call for a person who needed guidance on saving or planning for retirement was likely to be to a stockbroker or a mutual fund or insurance salesperson. As a result, in 1973, a group of 35 planners became the inaugural recipients of the CFP marks.

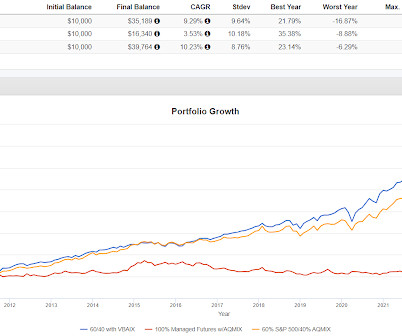

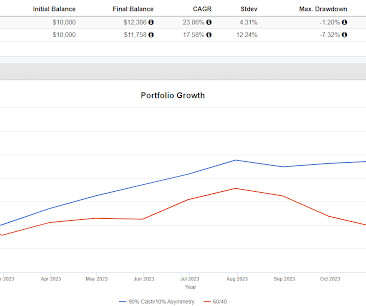

Looking at AQMIX on your statement kind of going nowhere for 10 years could be difficult but clearly a portfolio with the allocation in Portfolio 3 would have kept up just fine and if they had focused on the bottom line number and not the line items, it would not have been difficult. 90/40 was down 1.56% and Portfolio 3 was up 3.25%.

The Wall Street Journal ran an article titled Here's What It's Like To Retire On Almost Nothing But Social Security. He said " he was unprepared for sudden retirement, financially or otherwise." Being unprepared in his context doesn't have to just be about retirement account balances. Think about that.

In fact, we’ve been vocal that this isn’t a repeat of 2008. If you adjust it for only the working age and retired population then inventory is even higher. Of course, this data is highly localized and we generally measure “inventory” by the number of units that are actually for sale.

MLB was last to the instant replay party, finally adding it to check on home runs on August 28, 2008, nine years after Frank Pulli dipped his toe into the water. ” According to long-time umpire Joe West (now retired), “[t]hree ways you can miss a call: lack of concentration, lack of positioning, lack of timing.”

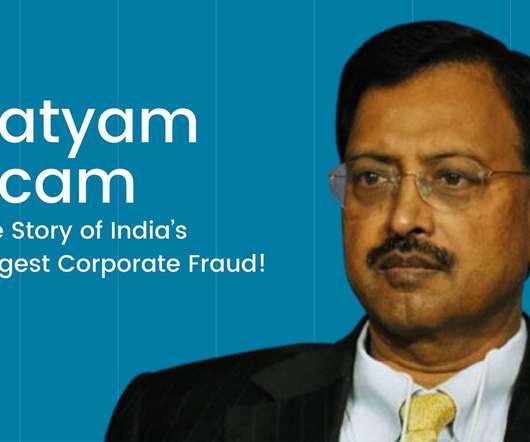

A Case Study on ‘Satyam Scam’ Accounting Scandal: When the 2008 recession hit the world, India was not only going through a financial crisis but also an ethical crisis. Satyam soon went on to cross the $2billion mark in 2008. 544 in 2008. This was what happened with Satyam Computer Services. The shares fell to Rs.11.50

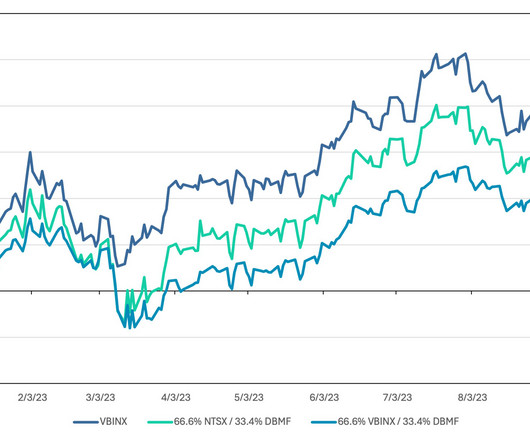

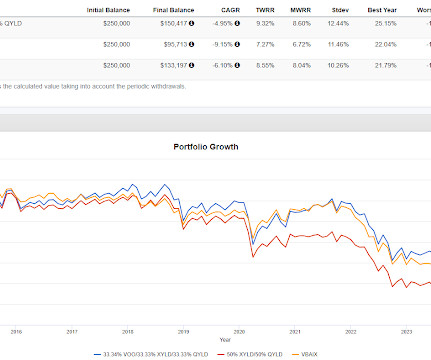

First on Monday's post about using return stacking to slightly increase the retirement withdrawal rate, I forgot about the WisdomTree Core Efficient Plus Fund (NTSX) which is leveraged up such that 67% in that fund equals 100% into a 60/40 portfolio like the Vanguard Balanced Income Fund (VBAIX). A couple of follow ups.

If you think about what Vanguard is all about, we sit there each and every day, figuring out how do we help people retire better, put their kids through college, afford that dream home? We were losing market share in the critical retirement, the 401(k) business. So that’s a number I hadn’t seen before. BUCKLEY: Yeah.

These numbers can and will be revised, and so it helps to look at the 3-month average. That number has been trending down since earlier this year, but it’s at a healthy 177,000 right now, above the 166,000 average pace in 2019. Not exactly weak (the hiring rate collapsed below 3% during the 2008-2009 recession), but not too hot either.

Studies by the American College of Financial Services show that 90% of special needs family members and caregivers admit that caring for their loved ones is more important to them than planning for their own retirement. Only a Canadian resident with a social insurance number and eligible for DTC can apply for CDSG.

However, risk capacity is a numbers game. Hardly: don’t forget the unexpected and shocking financial crisis of 2008 in the United States which crippled the economy. Investments with a short-term time horizon are best suited for those who would require a large amount of cash in the near future or will be approaching retirement soon.

RPAR has only been around since 2019 but the replication allows us to go back to 2008. It was down a little less in 2008 and 2022. If there was some number of shares and the index went to zero but shares still existed then when the index came back, the shares would have value again. Maybe it would be that simple?

The reader back then didn't specify which funds but since 2008, Hussman's two most prominent funds have compounded at -4.15% and 3.16% versus 7.52% for Vanguard Balanced Index Fund (VBAIX). I don't know whether those weightings can vary but the numbers come off the home page for the fund.

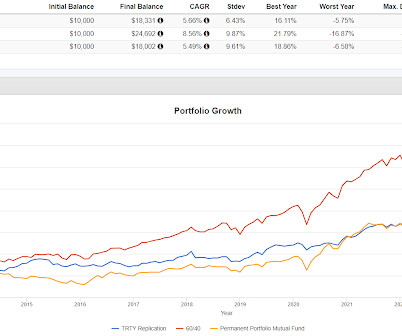

PRPFX outperformed 60/40 in 2008 by almost 12 percentage points and in 2022 by 11 1/2 percentage points. For the last ten years, 60/40 has blown away PRPFX and the standard deviation numbers for PRPFX in that time were only so so. Bank loan funds are mostly lower risk but the space did blow up in 2008.

We can backtest this back a good number of years on Portfolio Visualizer. Two of the three where Portfolio 1 outperformed were 2008 and 2022 which supports the idea of managed futures offering a form of crisis alpha. 70% then becomes an overweight versus a more typical 60% so ok a little more risk in the face of a 2008 type of decline.

He also hosts the Stay Wealthy Retirement Show , which has been ranked on Forbes Top 10 Retirement Podcasts. Back in 2008, CFP® professional Jeff Rose set out with one intention: create the best financial planner blog in the world. Learn more about Grace on LinkedIn. Taylor Schulte . Guess what? Aaron Klein. Brittney Castro.

Starting back in 2007 or 2008 I wrote about his barbell portfolio idea that goes very high risk with 10% of the portfolio in search of asymmetric returns and then very conservative with the other 90%. The numbers for Portfolios 1 and 3 add up to 105% because I am replicating 5% into a 2x bitcoin fund.

I remember when I entered the job market in the 70s (yes, I’m a boomer) we bemoaned our fate of being boomers because we were being spewed out of college and into the labor force in unprecedented numbers, driving competition for jobs up and wages down. And BTW, competition to get into college was very rough because of our numbers.

’cause then I figure I could always be employed either managing the numbers or doing law and get those two degrees. And I got to see firsthand what Bain was doing in strategic consulting and understand their view of business separate from the numbers. So he wanted me to work with him and then he’d retire.

The way that number went up though, I don't know if it was a real number or not. My highlight appearance was one of my early ones in the spring of 2008, I was very bearish on domestic financials. There were articles that may have been written just by Seeking Alpha staff or friends of founder David Jackson.

Let's say this person is 61, just retired, prefers to delay starting Social Security until age 70 and will take RMDs at 73 but could take IRA withdrawals earlier if the taxable account depletes. Putting it all into an S&P 500 index fund would run into trouble if the period in question included a 2008 when the index cut in half.

That worst year column is noteworthy, those numbers come from 2008. What does the complexity of capital efficiency in this example give the investor versus just owning VBAIX? Well, not much. There's four more basis points for CAGR which is given back in standard deviation.

Yes, I was bothered by the fact that it took such a complicated psychological issue and rendered it into an overly-simplistic two-digit number—your ‘score,’ so to speak. The goal to be achieved is really many goals: children’s college fund, buying a beach house, retirement, a legacy, etc.,

After facing the challenges of a post-2008 financial crisis world, many have thrived as entrepreneurs and in higher career roles. They need help initiating or boosting retirement plans, and saving prudently. Beneath the surface, there are three compelling reasons why financial advisors should focus on millennials.

We spend a lot of time here on how to diversify to try to smooth out the ride and how to hold up better when markets have a year like 2022 or 2008. Adding some asymmetry would add one or two more to that number. Diversification offsets the consequence of guessing what will work and being wrong. For us, that includes alternatives.

I'd rather be doing literally anything else than having my retirement hinge on me being able to see the future." However, it's also true that the worst bear markets ever- 1929, 1973, 2000 and 2008 all came after all-time highs, when investors were feeling supremely confident. Last week I showed that all-time highs are not bearish.

What would that do to people's retirement plans? If 2000 was fool me once and 2008 was fool me twice, what would 2019 be? The United States has experienced just six distinct bear markets since The Great Depression: 1929, 1937, 1969, 1973, 2000, and 2008. Entering these numbers was an uncomfortable experience.

The way portable used to primarily be implemented was to leverage up with correlated assets and it ended up going very badly in 2008 when equities dropped 40%. The risk to 40% or 30% of managed futures via leverage is that in a year like 2008, instead of going up like they "should," managed futures drops 15 or 20%.

The context is sustainable withdrawal rates in retirement. In the last few years or so there has been plenty of content positing that 4% is no longer safe, that 3% should be the number or even 2.5%. I would note that their numbers for failing at 4% are lower than any others I've ever seen. Looking backwards, it never failed.

They run long short across each of these, and they’ve put up some pretty impressive numbers over the past couple of years. He, he had retired, retired, but he was still active. You know, so I, I was, I was, I was in 00:07:48 [Speaker Changed] 2008, the start of the great financial crisis. That was great.

Get money rich (GMR) blog is run by Mani (founded in 2008). You can read a number of interesting articles regarding stock investing, mutual funds, real estate, income tax, personal finance, etc on this blog. You can also learn about stock market investing in Trade Brains’ recently launched android mobile app. Get Money Rich (GMR).

It has to be such a different set, the retirement planning is different, the safety net is different. People in Spain when I was growing up in the ‘80s and ‘90s, they expect to just retire and have the government give them like a paycheck every month. I was employee number 10. RITHOLTZ: So you move here from Spain.

Even Mr. Money Mustache, as a person who retired 17 years ago, is still in this boat for the simple reason that my retirement income from dividends and hobby businesses is still greater than my annual living expenses (which still hover around $20,000 per year). (It’s the current blowup) -20% so far What’s your guess?

And that number is set to drop to 1 within the next decade. There is, however, a far more stable government-backed system that can boost your retirement plans. Between 2008 and 2009, US consumer spending fell 8.2% When Social Security was introduced in 1935, there were 42 workers for every retiree. Today, there are only 2.9.

She has a number of investments as as really a entrepreneur and a venture investor. So then I, I knew the Yahoo folks, Jerry Yang and Sue Decker asked me to come in and help them in 2008. And so the magic number was $388 a month. That they could add to PayPal’s numbers. She was Chief Revenue Officer at Microsoft.

It was last below it for a brief moment in 2008 and before that, you had to go back to 1988! Perhaps people are putting a higher valuation on a shrinking number of public stocks. Retirement didn't exist. Jumping in or out of stocks based on valuation can be extremely difficult, if not completely impossible.

By comparison, the 2008 Troubled Asset Relief Program (“TARP”) was $700 billion, and the subsequent American Recovery and Reinvestment Act (“ARRA”) of 2009 was $831 billion. There are a number of temporary income tax provisions in the CARES Act that will be of interest to our private clients. trillion, equivalent to about 10% of U.S.

By comparison, the 2008 Troubled Asset Relief Program (“TARP”) was $700 billion, and the subsequent American Recovery and Reinvestment Act (“ARRA”) of 2009 was $831 billion. . There are a number of temporary income tax provisions in the CARES Act that will be of interest to our private clients. trillion, equivalent to about 10% of U.S.

Deferring taxes one year before retirement and then over a 10-year distribution schedule has value, but deferring taxes for 20 years (allowing your money to grow pre-tax) has a lot more value. So, you have a situation where you might not see your money until as much as ten years after you retire. Siemens Matching Benefit.

As bad as 2008 was, we're 3x from there. Going back to the above, risk and volatility become much easier to endure when you know that your cash needs for x number of months are all set and you truly understand that bear markets end and eventually there will be a new high even if that takes longer than you'd like.

It also encompasses intended lifestyle, charitable giving, retirement and estate planning, and liabilities, including anticipated costs for health care. Set hard numbers. It is not meant to be changed dramatically over time and is tailored to a client’s specific needs, including retirement, education and philanthropy.

Initially, with top marginal tax rates as high as 90 percent in the 1960s and 70 percent in the 1970s, these plans’ primary benefit was to shift income into lower-tax, retirement years. So, you have a situation where you might not see your money until as much as ten years after you retire.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content