This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirement planning process involves simulating whether the client's assets will last through retirement. One way that advisors can help bridge this gap is by using Historical Market Visualization (HiMaV) as a more intuitive alternative for illustrating retirement income strategies.

The tool includes the option to run plans through real-life historical scenarios including the Great Depression, the post-war period, 1970s stagflation, the dot-com bubble and the 2008 financial crisis.

At some point we are bound to see a stock market correction of some magnitude, hopefully not on the order of the 2008-09 financial crisis. As someone saving for retirement , what should you do now? Has the market rally accelerated the amount you’ve accumulated for retirement relative to where you had thought you’d be at this point?

The only other years with a higher reading since 1990 were 2008 when the S&P fell 38%, and 2002, when it fell 23%. Pensions Brace for Private-Equity Losses : Retirement officials predict grim results from investments in private equity and other illiquid assets ( Wall Street Journal ). • Wealth of Common Sense ). •

For example during the 2008-2009 market debacle I looked at funds to see how they did in both the down market of 2008 and the up market of 2009. If a fund did worse than the majority of its peers in 2008 I would expect to see better than average performance in the up market of 2009. Markets will always correct at some point.

thereformedbroker.com) Don't fight the last war: this isn't 2008. marketwatch.com) Seven important lessons about retiring successfully. (ramp.beehiiv.com) The bear case is obvious. What's the bull case? theirrelevantinvestor.com) Bear markets are where wealth is built. mr-stingy.com) TIPS yields are at their highest level in a decade.

But to illustrate the relative protection that bonds may be able to provide compared to stocks, heres what happened to the bond market in the 2008 great financial crisis and recession and 2020 market crash. The chart below shows what happened to fixed income (bonds) in 2008. Bond indices during the 2008 recession (gray).

In the mid-20th century, the first phone call for a person who needed guidance on saving or planning for retirement was likely to be to a stockbroker or a mutual fund or insurance salesperson.

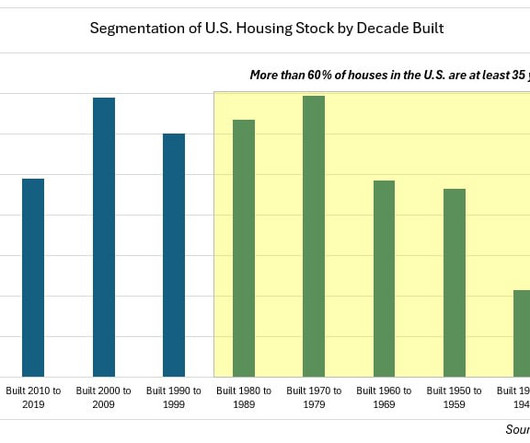

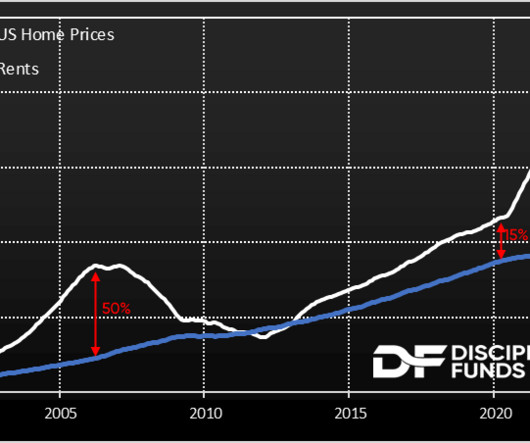

The housing bubble and subsequent bust that was largely responsible for the 2007 – 2009 financial crisis resulted in depressed housing starts for more than a decade; in fact, from 2008 through 2019, single family housing starts averaged just 660,000, not even 60% of the long-term average.

The New York Giants (an old NFL team) won in 2008 and the market tanked in what was the start of the financial crisis. Approaching retirement and want another opinion on where you stand? Financial coaching focuses on providing education and mentoring on the financial transition to retirement. NEW SERVICE – Financial Coaching.

The Wall Street Journal ran an article titled Here's What It's Like To Retire On Almost Nothing But Social Security. He said " he was unprepared for sudden retirement, financially or otherwise." Being unprepared in his context doesn't have to just be about retirement account balances. Think about that.

Veteran portfolio manager Bill Miller, founder of Miller Value Partners and manager of the firm’s Miller Opportunity Trust and the Miller Income funds, retired at the end of 2022, reports an article in CityWire. billion and has been renamed the Opportunity Trust under Patient Capital, since 2008.

In its annual Retirement Confidence Survey of current workers and retirees, the Employee Benefit Research Institute found that workers’ confidence in their ability to fund retirement fell by the largest extent since the financial crisis of 2008, to levels not seen since 2018.

MLB was last to the instant replay party, finally adding it to check on home runs on August 28, 2008, nine years after Frank Pulli dipped his toe into the water. ” According to long-time umpire Joe West (now retired), “[t]hree ways you can miss a call: lack of concentration, lack of positioning, lack of timing.”

The title of the Man article is Why Alpha Matters for Retirement Savers and in it, they make their case for portable alpha. Also PSLDX is capable of some huge drawdowns, dropping 43% in 2022 and 33% in 2008. Portable alpha combines plain vanilla exposure with alternatives in such a way that leverages up.

And be certain to listen to the end, where Eric discusses the key differences between CPA firms and RIAs, particularly the contrast between the goal of CPAs to maximize the efficiency of their billable hours and the more long-term client relationship-building done by financial advisors, how Eric approaches acquisitions, targeting younger or mid-career (..)

A Case Study on ‘Satyam Scam’ Accounting Scandal: When the 2008 recession hit the world, India was not only going through a financial crisis but also an ethical crisis. Satyam soon went on to cross the $2billion mark in 2008. 544 in 2008. This was what happened with Satyam Computer Services. The shares fell to Rs.11.50

Wall Street Journal ) • Why China Is Avoiding Using ‘Bazooka’ to Spur Economy : Beijing isn’t pulling out a “bazooka” stimulus package like it did during the global financial crisis in 2008-09, or even when the pandemic hit in 2020. Bloomberg ) • Roth vs. Traditional 401(k): Where to Put Your Money for Retirement? in the current one.

The 2022 economy has broken multiple records, first, with the highest inflation rate in 40 years, and now, the highest federal reserve interest rates since 2008. [1] 2] This rise in the cost of borrowing not only affects inflation but trickles into the decisions you make before and in retirement. Hike in Variable Debt Rates.

In one of the Tweets, that's right I said Tweets, he talked about 2008 being a disaster as correlations went to 1. I think the only capitally efficient funds back in 2008 were the PIMCO PLUS suite including the PIMCO Stocks PLUS Long Duration (PSLDX) which leveraged up 100/100 stocks and long bonds. versus down 21.63%.

In this episode, we talk in-depth about how Joe has witnessed firsthand as an advisory firm owner, and now a partner at a leading global investment management firm, how the financial services industry is evolving in real time as more banks and brokerage firms are truly adopting financial planning and implementing advisory services at national scale (..)

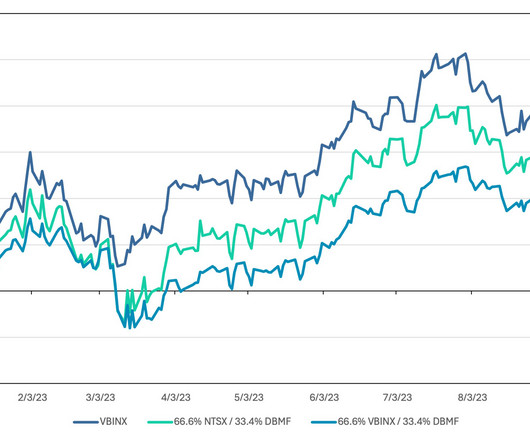

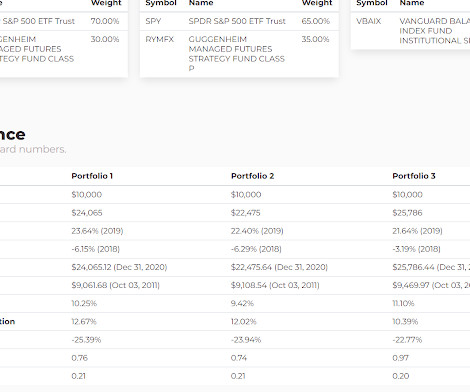

First on Monday's post about using return stacking to slightly increase the retirement withdrawal rate, I forgot about the WisdomTree Core Efficient Plus Fund (NTSX) which is leveraged up such that 67% in that fund equals 100% into a 60/40 portfolio like the Vanguard Balanced Income Fund (VBAIX). A couple of follow ups.

In 2022 it was actually flat while in 2008 it was down more than the S&P 500. They did well in 2022 but did poorly in 2008. I'm not saying these are bad funds to hold, they just don't offer too much zig when stocks zag. IGF is interesting though. MLPs are another odd one.

In fact, we’ve been vocal that this isn’t a repeat of 2008. If you adjust it for only the working age and retired population then inventory is even higher. Especially not in an environment where the demand for buying is drying up as the Fed raises rates aggressively and the average mortgage rate surges back to 7%.

Barron's wrote about the difficulty of spending down accumulated assets in retirement. Several quick hits today. I am pretty sure this will be difficult for me if our savings play a big role in our month to month lifestyle. This was an article where always read the comments applies.

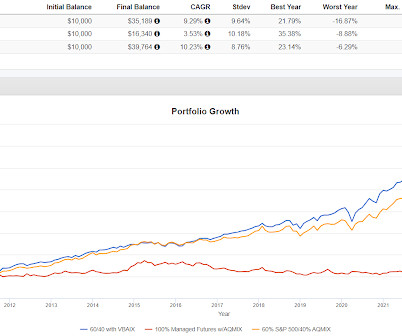

Someone retiring on Dec 31, 2021 being all in on traditional 60/40 had a real problem from an adverse sequence of returns. Someone retiring on Dec 31, 2021 with one of the managed futures-heavy portfolios had no such problem. The advantage that both managed futures portfolios had over traditional 60/40 is how well they did in 2022.

Barron's posted an article that by the title was about expenses to consider if you retire early but the article was pretty thin. A couple of stats from the article included that 46% of American retire sooner than they expected with the two most common reasons being laid off or health issues with themselves or their partner.

On December 24, 2008, the Dow Jones was down 1000 points and then on December 26th it was up 1000 points but of course that market event still had several months to go. John Authers from Bloomberg is calling it the end of the beginning. It is possible it's over but I would be ready for more volatility.

The S&P 500 doesn't fall 20% in a quarter very often but obviously it can happen, it happened in Q1 of 2020 and the 3rd quarter of 2008 and I imagine there were others. The next day the fund would have a new buffer 20% down from there. If someone is actually going to use this, it is crucial they sell before the 20% threshold is hit.

We are on pace to post the first double-digit loss in the major US markets since 2008. As we look forward to 2023, the IRS recently announced that the contribution limits for employer-sponsored retirement plans are going up. 2022 has been a difficult and trying year for stock and bond indexes in both emerging and developed markets.

The best example of this that I can think of to make the point was in the fall of 2008 when one day, the Dow fell 1000 points and then the next day it made it most of it back. The tape would be a little more constructive if the declines stopped with more of a whimper, just petering out versus such a dramatic move up.

The 2008 global financial crisis is one of the biggest examples of how significant it is to have proper compliance regulations in place in order to create a safe and healthy financial ground for the people. The primary cause of the 2008 global financial crisis was the deregulation of the financial industry.

In 2008, he bought three books on Social Security, read them cover to cover, and emerged with more questions than answers. Blair worked for SSA for 35 years before retiring on December 31, 2010. Over his three-decade career as a CPA, Kiner grew increasingly interested in the inner workings of Social Security benefits.

Brian talks about how predictions went with economists and TV personalities before 2008. Consider what you want to do long-term and how you spend your time in your retirement. Before you retire, have you thought through what you’ll do with your time? Is working in some capacity a part of your retirement plan.

If you think about what Vanguard is all about, we sit there each and every day, figuring out how do we help people retire better, put their kids through college, afford that dream home? We were losing market share in the critical retirement, the 401(k) business. He stepped down as the CEO in 2008. So we’ve rebuilt.

One of the first reforms he put in place was setting a retirement age. According to this policy, the retirement age for directors was set at 70 and senior executives at 65. Mody was sacked after a messy scrap, Seth and Kerkar retired over the years as they crossed the age limits and Palkhivala quit citing ill health.

RPAR has only been around since 2019 but the replication allows us to go back to 2008. It was down a little less in 2008 and 2022. It isn't necessarily a bad thing that risk parity lagged but it did so with a higher standard deviation. The year by year for risk parity replication shows quite a few things.

And since the other funds came along, RYMFX has shown to not be such a great representation of the strategy even though it helped in 2008. Plenty of other managed futures funds came onto the scene in 2013 and 2014 but I think RYMFX is the only one to test what was a terrible time for managed futures.

The chart also shows that carry has not helped as crisis alpha in either 2008 when it dropped dramatically or in 2022 where it looked like a horizonal line with a slight tilt upwards. The carry index does appear to start moving higher in late 2022 or early 2023 as the effect of higher rates started to kick in.

Meanwhile, the 5-year yield on Treasury inflation-protected securities, a reflection of market expectations for inflation, rose above 2% and headed for its highest closing level since mid-December of 2008 as of Thursday morning, according to Tradeweb.All three major U.S. s “troubling” fiscal trajectory, among other things.A

Studies by the American College of Financial Services show that 90% of special needs family members and caregivers admit that caring for their loved ones is more important to them than planning for their own retirement. Related: How Financial Advisors Should Engage With Female Clientele?

He also hosts the Stay Wealthy Retirement Show , which has been ranked on Forbes Top 10 Retirement Podcasts. Back in 2008, CFP® professional Jeff Rose set out with one intention: create the best financial planner blog in the world. Learn more about Grace on LinkedIn. Taylor Schulte . Guess what? Brittney Castro. Christine Benz.

Our recent Advisor Authority survey , powered by the Nationwide Retirement Institute®, found that many investors see a future financial crisis as more of a certainty than a possibility. On top of that, many respondents said they don’t believe their finances will survive the next market downturn.

Hardly: don’t forget the unexpected and shocking financial crisis of 2008 in the United States which crippled the economy. Investments with a short-term time horizon are best suited for those who would require a large amount of cash in the near future or will be approaching retirement soon.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content