This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For many financial advisors, a core part of the retirementplanning process involves simulating whether the client's assets will last through retirement. That emotional connection supports confidence and increases the likelihood that the client will stick with their plan and stay committed through both good markets and bad.

At some point we are bound to see a stock market correction of some magnitude, hopefully not on the order of the 2008-09 financial crisis. As someone saving for retirement , what should you do now? If you have a financial plan this is an ideal time to review it and see where you are relative to your goals. Learn from the past

For example during the 2008-2009 market debacle I looked at funds to see how they did in both the down market of 2008 and the up market of 2009. If a fund did worse than the majority of its peers in 2008 I would expect to see better than average performance in the up market of 2009. Markets will always correct at some point.

But to illustrate the relative protection that bonds may be able to provide compared to stocks, heres what happened to the bond market in the 2008 great financial crisis and recession and 2020 market crash. The chart below shows what happened to fixed income (bonds) in 2008. Bond indices during the 2008 recession (gray).

The New York Giants (an old NFL team) won in 2008 and the market tanked in what was the start of the financial crisis. Approaching retirement and want another opinion on where you stand? Financial coaching focuses on providing education and mentoring on the financial transition to retirement. NEW SERVICE – Financial Coaching.

The Wall Street Journal ran an article titled Here's What It's Like To Retire On Almost Nothing But Social Security. He said " he was unprepared for sudden retirement, financially or otherwise." Being unprepared in his context doesn't have to just be about retirement account balances. Think about that.

We are on pace to post the first double-digit loss in the major US markets since 2008. As we look forward to 2023, the IRS recently announced that the contribution limits for employer-sponsored retirementplans are going up. IRA Accounts. Insurance Amounts .

The title of the Man article is Why Alpha Matters for Retirement Savers and in it, they make their case for portable alpha. Also PSLDX is capable of some huge drawdowns, dropping 43% in 2022 and 33% in 2008. Portable alpha combines plain vanilla exposure with alternatives in such a way that leverages up.

In its annual Retirement Confidence Survey of current workers and retirees, the Employee Benefit Research Institute found that workers’ confidence in their ability to fund retirement fell by the largest extent since the financial crisis of 2008, to levels not seen since 2018.

In one of the Tweets, that's right I said Tweets, he talked about 2008 being a disaster as correlations went to 1. I think the only capitally efficient funds back in 2008 were the PIMCO PLUS suite including the PIMCO Stocks PLUS Long Duration (PSLDX) which leveraged up 100/100 stocks and long bonds. versus down 21.63%.

Brian talks about how predictions went with economists and TV personalities before 2008. Consider what you want to do long-term and how you spend your time in your retirement. Before you retire, have you thought through what you’ll do with your time? Is working in some capacity a part of your retirementplan.

On December 24, 2008, the Dow Jones was down 1000 points and then on December 26th it was up 1000 points but of course that market event still had several months to go. John Authers from Bloomberg is calling it the end of the beginning. It is possible it's over but I would be ready for more volatility.

Barron's wrote about the difficulty of spending down accumulated assets in retirement. Several quick hits today. I am pretty sure this will be difficult for me if our savings play a big role in our month to month lifestyle. This was an article where always read the comments applies.

The S&P 500 doesn't fall 20% in a quarter very often but obviously it can happen, it happened in Q1 of 2020 and the 3rd quarter of 2008 and I imagine there were others. The next day the fund would have a new buffer 20% down from there. If someone is actually going to use this, it is crucial they sell before the 20% threshold is hit.

In 2022 it was actually flat while in 2008 it was down more than the S&P 500. They did well in 2022 but did poorly in 2008. I'm not saying these are bad funds to hold, they just don't offer too much zig when stocks zag. IGF is interesting though. MLPs are another odd one.

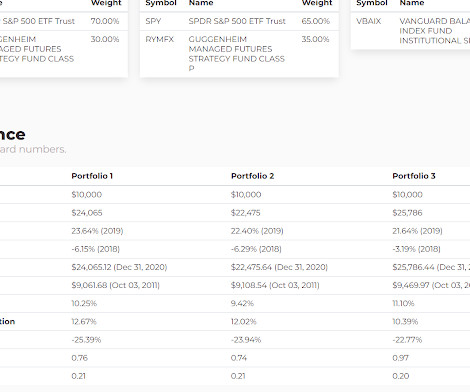

First on Monday's post about using return stacking to slightly increase the retirement withdrawal rate, I forgot about the WisdomTree Core Efficient Plus Fund (NTSX) which is leveraged up such that 67% in that fund equals 100% into a 60/40 portfolio like the Vanguard Balanced Income Fund (VBAIX). A couple of follow ups.

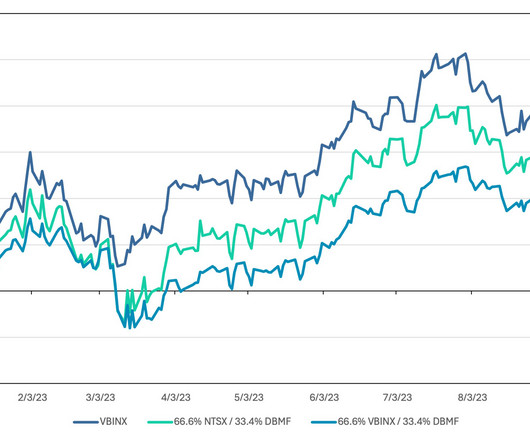

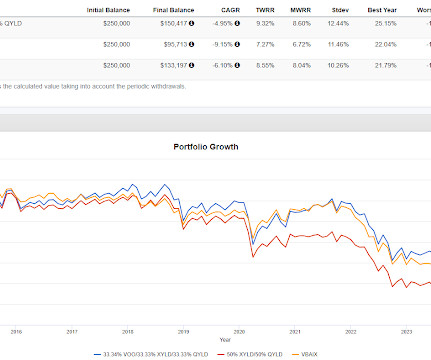

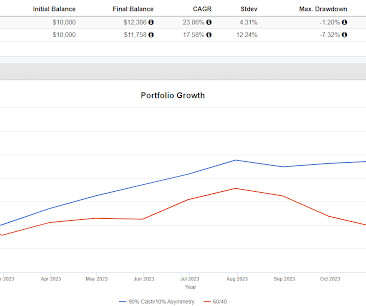

Someone retiring on Dec 31, 2021 being all in on traditional 60/40 had a real problem from an adverse sequence of returns. Someone retiring on Dec 31, 2021 with one of the managed futures-heavy portfolios had no such problem. The advantage that both managed futures portfolios had over traditional 60/40 is how well they did in 2022.

The best example of this that I can think of to make the point was in the fall of 2008 when one day, the Dow fell 1000 points and then the next day it made it most of it back. The tape would be a little more constructive if the declines stopped with more of a whimper, just petering out versus such a dramatic move up.

savings rate lowest since 2008 Buy now pay later companies being tested Housing affordability Ric Edelman on Crypto, retirementplanning, the advice business, and more Bipartisan Crypto bill Solana suffered its second outage in a month Coinbase slowing hiring The Netflix token The U.S.

Barron's posted an article that by the title was about expenses to consider if you retire early but the article was pretty thin. A couple of stats from the article included that 46% of American retire sooner than they expected with the two most common reasons being laid off or health issues with themselves or their partner.

If you think about what Vanguard is all about, we sit there each and every day, figuring out how do we help people retire better, put their kids through college, afford that dream home? We were losing market share in the critical retirement, the 401(k) business. He stepped down as the CEO in 2008. So we’ve rebuilt.

And since the other funds came along, RYMFX has shown to not be such a great representation of the strategy even though it helped in 2008. Plenty of other managed futures funds came onto the scene in 2013 and 2014 but I think RYMFX is the only one to test what was a terrible time for managed futures.

After facing the challenges of a post-2008 financial crisis world, many have thrived as entrepreneurs and in higher career roles. Comprehensive Financial Planning Beyond debt, millennials seek comprehensive financial advice. They need help initiating or boosting retirementplans, and saving prudently.

Let's say this person is 61, just retired, prefers to delay starting Social Security until age 70 and will take RMDs at 73 but could take IRA withdrawals earlier if the taxable account depletes. Putting it all into an S&P 500 index fund would run into trouble if the period in question included a 2008 when the index cut in half.

He also hosts the Stay Wealthy Retirement Show , which has been ranked on Forbes Top 10 Retirement Podcasts. Back in 2008, CFP® professional Jeff Rose set out with one intention: create the best financial planner blog in the world. Learn more about Grace on LinkedIn. Taylor Schulte . Guess what? Brittney Castro. Christine Benz.

The chart also shows that carry has not helped as crisis alpha in either 2008 when it dropped dramatically or in 2022 where it looked like a horizonal line with a slight tilt upwards. The carry index does appear to start moving higher in late 2022 or early 2023 as the effect of higher rates started to kick in.

While the market remains strong, how does this news affect the savings of retirees or those about to retire? . That tops the inflation fears that surged in 2008, just before the financial crisis, and a previous peak in early 2005, when the housing market was out of control.” . bond market’s prediction of U.S.

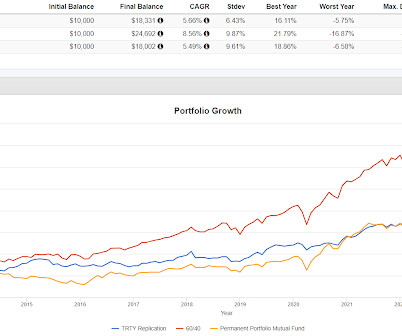

RPAR has only been around since 2019 but the replication allows us to go back to 2008. It was down a little less in 2008 and 2022. It isn't necessarily a bad thing that risk parity lagged but it did so with a higher standard deviation. The year by year for risk parity replication shows quite a few things.

There were places to make money during that run, most notably foreign stocks and equal weight S&P 500, that ETF came out in 2003 and had very good years until 2008. That's a long time for a broad based index to not make any progress. It then had a huge snap back year in 2009.

PRPFX outperformed 60/40 in 2008 by almost 12 percentage points and in 2022 by 11 1/2 percentage points. Bank loan funds are mostly lower risk but the space did blow up in 2008. For the last ten years, 60/40 has blown away PRPFX and the standard deviation numbers for PRPFX in that time were only so so.

Here's an article I wrote for theStreet.com in March, 2008 about the Rydex (now Guggenheim) Managed Futures (RYMFX). Yes, DBMF having the word strategy in the name is confusing but logically, there will be times where replication will outperform and times where it lags so saying one is better isn't the way to frame it.

stock market didn’t completely recover from the 2008 financial crisis until well into 2013. Usually those goals involve a retirementplan, and you shouldn’t ever invest more than you’re prepared to lose. Forbes offers 3 pieces of advice to increase future wealth, on the assumption that the economy will take some time to rebound.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

These strategies may include the conversion of an IRA or qualified retirementplan to a Roth IRA , because the tax consequences of such a conversion are based on asset values at the time of conversion, and any future growth in value will avoid income taxation, both within the plan and at the time of distribution to the plan beneficiary.

What would that do to people's retirementplans? If 2000 was fool me once and 2008 was fool me twice, what would 2019 be? The United States has experienced just six distinct bear markets since The Great Depression: 1929, 1937, 1969, 1973, 2000, and 2008. What would happen if stocks crash?

Two of the three where Portfolio 1 outperformed were 2008 and 2022 which supports the idea of managed futures offering a form of crisis alpha. 70% then becomes an overweight versus a more typical 60% so ok a little more risk in the face of a 2008 type of decline. This is all very interesting stuff.

For comparison, from 2008 forward, the S&P 500 had a CAGR of 7.65% and a standard deviation of 16.19%. RQI and UTF have each been around since at least 2008 and they too have compounded negatively, again, we are excluding the income because that is the author's premise. There is also inflation risk.

Retirementplan sponsors. We are currently experiencing one of the most volatile times in decades, on top of the start of the pandemic and the 2008-2009 recession. Investments and economy. OCIO/Investment outsourcing. Nonprofits and healthcare organizations. Institutional (US).

In 2008, JNJ was down just under 8% and in 2022 it was up about 7%. The next time the stock market drops 30-40%, I'd expect certain holdings like MSI to fall more and I'd expect some holdings to go down less (or maybe even up in a couple of instances). While that seems reliable to me, it's not infallible for future market events.

We spend a lot of time here on how to diversify to try to smooth out the ride and how to hold up better when markets have a year like 2022 or 2008. Diversification offsets the consequence of guessing what will work and being wrong. For us, that includes alternatives. Barron's had an article about alternatives sought by the "super rich.

Starting back in 2007 or 2008 I wrote about his barbell portfolio idea that goes very high risk with 10% of the portfolio in search of asymmetric returns and then very conservative with the other 90%. It's an interesting idea and if CAOS turns out to not be the answer, maybe something else in the future will be.

The reader back then didn't specify which funds but since 2008, Hussman's two most prominent funds have compounded at -4.15% and 3.16% versus 7.52% for Vanguard Balanced Index Fund (VBAIX). Back in the financial crisis, a reader left a comment about just "putting it all in Hussman" and forget about it.

Get money rich (GMR) blog is run by Mani (founded in 2008). Stable Investor also provides various financial services like financial planning, retirementplanning, children’s future planning, etc. You can also learn about stock market investing in Trade Brains’ recently launched android mobile app.

And although they’ve gotten off to a rocky start after the Great Recession of 2008, many have found success as entrepreneurs and in higher-level positions in their careers. . In fact, I’m one of the oldest of the millennial generation and I need help from my advisor with all of the following: Retirementplanning. Tax planning.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content