This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

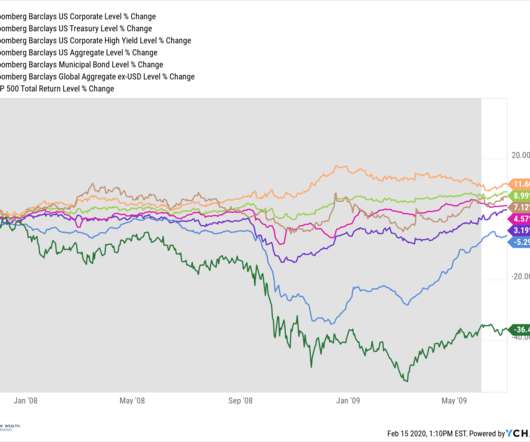

Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risktolerance. For example during the 2008-2009 market debacle I looked at funds to see how they did in both the down market of 2008 and the up market of 2009. Focus on risk.

At some point we are bound to see a stock market correction of some magnitude, hopefully not on the order of the 2008-09 financial crisis. As someone saving for retirement , what should you do now? Has the market rally accelerated the amount you’ve accumulated for retirement relative to where you had thought you’d be at this point?

The New York Giants (an old NFL team) won in 2008 and the market tanked in what was the start of the financial crisis. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. Approaching retirement and want another opinion on where you stand? Take stock of where you are.

For more years than I’d care to name, I’ve been trying to put my finger on exactly why I have a such a huge problem with the traditional (Think: Riskalyze, now Nitrogen) risktolerance assessments in the financial planning profession. You can actually test various bear markets and adjust accordingly.)

However, it should be well understood that a client’s financial profile includes their risktolerance and their risk capacity. In this article, although we will be focusing on the latter one and why it is significant to determine your client’s risk capacity let’s first understand the difference between the two.

Regardless, the goal of long-term investing is to master the art of maximizing returns and limiting taxes subject to your risktolerance. Just imagine what unknown leaky costs on your investments could mean for your retirement. Do you want high or unknown investment fees to delay your retirement by years? I think not.

A strong savings rate relative to your income can help you build reserves before retirement—and during retirement, the focus should be maintaining a reasonable and flexible withdrawal rate relative to your investable assets. And during periods of high inflation or market volatility, the negative effects of over-spending are magnified.

This includes articulating a policy with regard to investment risktolerance, long-term goals, cash flow needs and sector diversification. It also encompasses intended lifestyle, charitable giving, retirement and estate planning, and liabilities, including anticipated costs for health care.

And then I moved back to London at the end of 2008, which was a really interesting pivot. At the end of 2008, we owned a lot of illiquid assets. And there was a problem with 168 of them at the end of 2008. It was the year I made partner, actually, in 2008. I did that for a couple of years. RITHOLTZ: Good timing, yes.

MIELLE: After 2008? RITHOLTZ: 2008, ’09. So you retire in 2018. MIELLE: And then the biggest luck of it all, is I joined Canyon in the ‘90s and there was a tsunami that literally lifted all waves of hedge funds from ‘90 to 2008 and even beyond. Tell us about that period. But it was not a liquidity issue. ’08

Whenever I get that question, I typically start by explaining what an I-R-A stands for: Individual Retirement Arrangement (emphasis on arrangement). They are just a type of account – a retirement account. If you had invested into the stock market in 2008, your Roth IRA probably paid closer in the -30% range.

. ’cause they sort of feel like, you know, we can wait a little bit longer and the risk that we’re taking is very slow because look at how strong the US labor market is. Early retirements have been taking place a giant uptick in new business formation. We’ve reduced legal immigration for, for jobs dramatically.

I went there because I was fearful that being a professor would be like retiring in your 20s. But we know, and this is what at least I wasn’t sufficiently alert to in 2008, that self-interested or malevolent types can use behavioral biases to manipulate people. SUNSTEIN: But by tradition, it is not just a lackey.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content