This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The post The Fastest Drop in Home Prices Since 2009 appeared first on The Reformed Broker. Previous to her current position, Skyler founded a consultancy supporting public-facing economic data program, was head of economics at a digital mortgage start-up, and spent 8 years supporting the Zillow economic research department.

Today, in the Calculated Risk Real Estate Newsletter: Moody's: National Multifamily Supply and Demand at Lowest Levels since 2009 A brief excerpt: The big story here is that demand for apartments fell off a cliff in Q4 2022, but that new supply was also very low, even though there are a large number of apartments currently under construction.

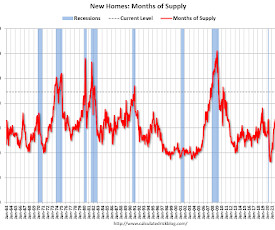

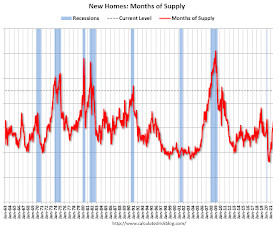

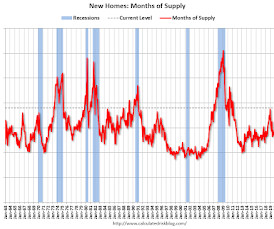

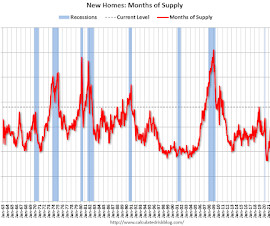

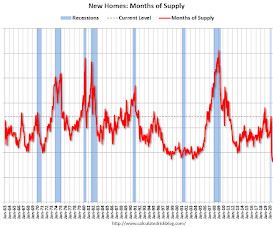

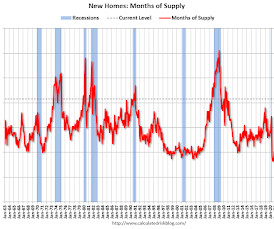

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in November to 8.9 months from 9.2 months in October. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply increased in January to 9.0 months from 8.0 months in December. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020.

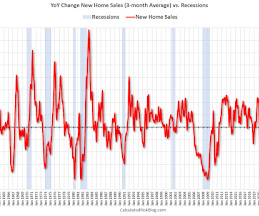

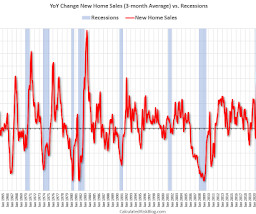

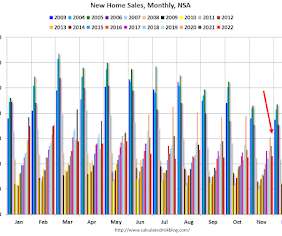

Also note that the sharp decline in 2010 was related to the housing tax credit policy in 2009 - and was just a continuation of the housing bust. Another exception was in late 2021 - we saw a significant YoY decline in new home sales related to the pandemic and the surge in new home sales in the second half of 2020.

The US population today is 341,814,420; in 2009 it was 308,512,035. Economy in 2022 was $25,439.70B; in 2009, it was $14,478.06B; ignore that also? from 2009, and by 2024 you get (wait for it) $193.44T. Do we simply ignore the growth in the size of the economy and the U.S. population? Do we just ignore that?

We’ve been in a recession just 1% of the time since the end of the Great Financial Crisis in the summer of 2009. One of my favorite ongoing economic stats is the fact that the U.S. economy has been in a recession for just two months out of the past 15-and-a-half years. Sure, there have been some bumps along the way but the U.S.

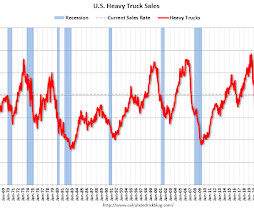

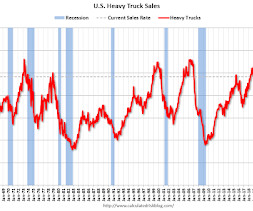

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. The dashed line is the March 2025 seasonally adjusted annual sales rate (SAAR) of 403 thousand. Then heavy truck sales increased to a new record high of 570 thousand SAAR in April 2019. Click on graph for larger image.

” – George Soros, 2009 I’ve spent 25 years watching, trading and investing in the stock market. “When I see a bubble forming I rush in to buy, adding fuel to the fire. That is not irrational.” The repetition of patterns is amazing.

Office REITs are trading at their lowest levels since 2009, reports Bloomberg. Crow Holdings formed a $2.6 billion joint venture focused on retail assets. These are some must reads from around the real estate investment world heading into the weekend.

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. The dashed line is the April 2024 seasonally adjusted annual sales rate (SAAR). Then heavy truck sales increased to a new record high of 570 thousand SAAR in April 2019. Click on graph for larger image.

For loans made in 2005 through 2008 (1% of portfolio), 3.83% are seriously delinquent (down from 3.95%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.55% are seriously delinquent (down from 0.57%). So, Fannie is still working through a few poor performing loans from the bubble years.

For loans made in 2005 through 2008 (1% of portfolio), 3.49% are seriously delinquent (down from 3.71%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.52% are seriously delinquent (down from 0.53%). So, Fannie is still working through a handful of poor performing loans from the bubble years.

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. The dashed line is the September 2022 seasonally adjusted annual sales rate (SAAR). Then heavy truck sales increased to a new all-time high of 570 thousand SAAR in April 2019. Click on graph for larger image.

For loans made in 2005 through 2008 (1% of portfolio), 3.11% are seriously delinquent (down from 3.31%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.48% are seriously delinquent (down from 0.51%). So, Fannie is still working through a few poor performing loans from the bubble years.

For loans made in 2005 through 2008 (1% of portfolio), 3.49% are seriously delinquent (unchanged from 3.49%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.53% are seriously delinquent (up from 0.52%). So, Fannie is still working through a handful of poor performing loans from the bubble years.

For loans made in 2005 through 2008 (1% of portfolio), 3.71% are seriously delinquent (down from 3.83%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.53% are seriously delinquent (down from 0.55%). So, Fannie is still working through a handful of poor performing loans from the bubble years.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in March to 7.6 months from 8.4 months in February. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in May to 6.7 months from 7.6 months in April. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020. This is above the top of the normal range (about 4 to 6 months of supply is normal).

Public construction spending is 6% above the peak in March 2009. Residential (red) spending is 36% above the bubble peak (in nominal terms - not adjusted for inflation). Non-residential (blue) spending is 19% above the bubble era peak in January 2008 (nominal dollars). The second graph shows the year-over-year change in construction spending.

Public construction spending is 9% above the peak in March 2009. Residential (red) spending is 35% above the bubble peak (in nominal terms - not adjusted for inflation). Non-residential (blue) spending is 24% above the bubble era peak in January 2008 (nominal dollars). The second graph shows the year-over-year change in construction spending.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in January to 7.9 months from 8.7 months in December. The all-time record high was 12.1 The all-time record low was 3.5 months, most recently in October 2020.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in September to 7.6 months from 7.9 months in August. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020.

Back in early 2009, I wrote a couple of posts arguing there would be an increase in auto sales - Vehicle Sales (Jan 2009) and Looking for the Sun (Feb 2009). This was an out-of-the-consensus call and helped me call the bottom for the US economy in mid-2009. Click on graph for larger image in graph gallery.

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. The dashed line is the August 2023 seasonally adjusted annual sales rate (SAAR). Then heavy truck sales increased to a new record high of 570 thousand SAAR in April 2019. Click on graph for larger image.

For in depth description of these issues, see Jed Kolko's article from 2014 "Let’s Improve, Not Ignore, Seasonal Adjustment of Housing Data" Note: I was one of several people to question the change in the seasonal factor (here is a post in 2009 ) - and this led to S&P Case-Shiller questioning the seasonal factor too ( from April 2010 ).

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in August to 8.1 months from 10.4 months in July. The all-time record high was 12.1 The all-time record low was 3.5 months, most recently in October 2020. The seasonally?

Also note that the sharp decline in 2010 was related to the housing tax credit policy in 2009 - and was just a continuation of the housing bust. Another exception was in late 2021 - we saw a significant YoY decline in new home sales related to the pandemic and the surge in new home sales in the second half of 2020.

capitalspectator.com) The credit markets are very different than they were in 2009. (behaviouralinvestment.com) Why selling a stock is harder than buying. flyoverstocks.com) Bond investors are being given an opportunity to lock in 2% real yields. semafor.com) A wide range of outcomes is always on the table.

November 29, 2023) The Most Hated Rally in Wall Street History (October 8, 2009) Bull & Bear Markets The post All-Time Highs Are Historically Bullish appeared first on The Big Picture.

He is the author of the Bailout Nation: How Greed and Easy Money Corrupted Wall Street and Shook the World Economy (Wiley, 2009). Barry Ritholtz is the creator and host of Bloombergs Masters in Business radio podcast, and a featured columnist at the Washington Post.

Way back in 2009, I pointed out that there are usually two bottoms for housing. Brief excerpt: I’ve heard some positive comments from a number of real estate agents in the last week about the existing home market. Activity is still down sharply year-over-year (YoY), but the YoY decline is getting smaller.

For loans made in 2005 through 2008 (1% of portfolio), 4.11% are seriously delinquent (down from 4.45%), For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.60% are seriously delinquent (down from 0.63%). So, Fannie is still working through a few poor performing loans from the bubble years.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in September to 6.9 months from 7.7 months in August. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020. This is above the top of the normal range (about 4 to 6 months of supply is normal).

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in June to 9.3 months from 8.4 months in May. The all-time record high was 12.1 The all-time record low was 3.5 months, most recently in October 2020. The seasonally?

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in April to 7.6 months from 7.9 months in March. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020. This is well above the top of the normal range (about 4 to 6 months of supply is normal).

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in November to 8.6 months from 9.3 months in October. The all-time record high was 12.1 The all-time record low was 3.5 months, most recently in October 2020.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply was unchanged in January at 8.3 months from 8.3 months in December. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply increased in August to 7.8 months from 7.0 months in July. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020. This is above the top of the normal range (about 4 to 6 months of supply is normal).

Monetary stimulus (ZIRP/QE) from 2009-2021. – Great Financial Crisis, March 2009 : The S&P 500 index made a generational low post-GFC on March 9, 2009, after having fallen 56.78%. Historically, SPX averages about 8% with dividends. Fiscal stimulus 2020-22. The next ~12 years saw gains of 608.5% through January 4, 2022.

months of supply in January 2009. The second graph shows New Home Months of Supply. The months of supply decreased in December to 8.2 months from 8.8 months in November. The all-time record high was 12.2 The all-time record low was 3.3 months in August 2020.

Heavy truck sales really collapsed during the great recession, falling to a low of 180 thousand SAAR in May 2009. The dashed line is the July 2024 seasonally adjusted annual sales rate (SAAR) of 485 thousand. Then heavy truck sales increased to a new record high of 570 thousand SAAR in April 2019. Click on graph for larger image.

This was the largest increase for the full month of February since 2009’s 4.4% From Manheim Consulting today: Wholesale Used-Vehicle Prices See Large Increase in February Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) increased 4.3% in February from January. from a year ago. year over year.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content