This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Sherman oversees and administers DoubleLine’s investment management subcommittee; serves as lead portfolio manager for multisector and derivative-based strategies; and is a member of the firm’s executive management and fixed-income assetallocation committees. He is host of the podcast The Sherman Show and a CFA charter holder.

Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risk tolerance. For example during the 2008-2009 market debacle I looked at funds to see how they did in both the down market of 2008 and the up market of 2009.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

Since 2009, a total U.S. A lot of investors have abandoned international diversification (or at least strongly considered it) in recent years. I understand why this is happening. stock market has destroyed all comers ever since the Great Financial Crisis ended. That’s annual returns of more than 14% per.

Based on Cambria's other multi-asset funds, ENDW will probably have fixed income duration but that's a space I will continue to avoid. Most of us of course lived through that from 2000 through to 2009. It then had a huge snap back year in 2009. The results. That's a long time for a broad based index to not make any progress.

The funds did well in the Financial Crisis and they did well in 2022 but from 2009 onward, one of his two long standing funds has a negative annual growth rate and the one with a positive growth rate was less than 1/3 of a plain vanilla 60/40 portfolio. Gold was mostly in a downtrend from mid-2011 to early 2016.

Fund managers remain historically conservative per Bank of America’s Global Fund Manager Survey showing assetallocators long cash and short equities. Cash levels rose in March at the fastest pace since last September and remain above average and allocation to equities remains significantly lower than in history.

This fierce competition amongst asset management companies is driving down expense ratios, but investor's are potentially paying higher costs. Large Cap ETFs with over $500 million in assets, which means there will always be something in that category doing better than what you've selected. There are 50 U.S.

In February 2009, it fell to a low of 12.4, I would have thought that financials have had the best returns since March 2009, and was surprised to see that consumer discretionary has done better, returning 617% (oh my god 617%) compared with 548% for financials. investors who allocate to emerging markets. This is a scary chart.

Sure, I'm $200,000 short of my goal but you know what, I beat the market five years in a row from 2009-2013." When you get close to retirement, you know what will matter? What will matter is whether you have enough to retire to the lifestyle you want plus maybe having some sort of margin for error in your accumulated savings.

assets the cold shoulder. Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% Since trying to time regime changes is very difficult in real time without the benefit of hindsight, there are reasons to consider allocating both U.S. equities to an assetallocation. Source: J.P.

They charge either a percentage of assets managed or a flat hourly rate that can run as high as several hundred dollars per hour, plus trading commissions and administrative fees. You can also get information on your performance and assetallocation. And, that’s it. There are no additional fees.

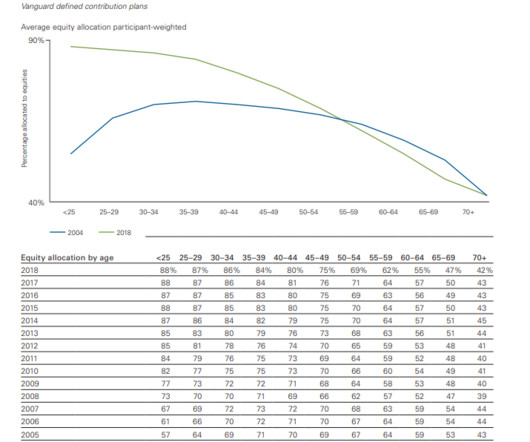

trillion in assets. They anticipate that by 2023 80% of all assets at Vanguard will be in an automatic investment program. 18,500, $24,500 for people 50 or older) The chart below shows overall assetallocation in these plans. Vanguard is out with a new monster research report called How America Saves.

1 Also, from fiscal year 2009 until fiscal year 2016, federal agencies cut annual grants to private and public organizations by 3.4% Alternatively, nonprofits can boost potential portfolio returns, which often means tolerating more risk and illiquidity, through a recalibration of assetallocation— the single biggest driver of long-term gains.

We are currently experiencing one of the most volatile times in decades, on top of the start of the pandemic and the 2008-2009 recession. That’s why, when facing market volatility, stewards of long-term assets held at all types of nonprofit institutions recognize the importance of a well-thought-out investment process. .

With the wild swings in the stock and bond market this year, it's likely that your assetallocation has gotten a bit out of whack. A portfolio rebalance is simply the act of returning to your pre-determined assetallocation. Assetallocation is all about trade offs. stock.bond) is now 54/46. Treasury Notes).

The chart below illustrates that the smart money enters when valuations are low and the majority of the investors aren’t looking at that asset class or security. The important takeaway is that there should be an allocation plan prepared for asset class volatility and it shouldn’t be just an ad-hoc emotional buying or selling.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term assetallocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfolio management decisions.

So it’s, 00:09:11 [Speaker Changed] You’ve become an enterprise, it’s 10 x what it once was in terms of headcount, it’s much bigger in terms of assets. I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular.

However, the impending end of the Federal Reserve (Fed) rate-hiking campaign, and the economy’s and corporate America’s resilience, help make the bull case that steers LPL Research toward a neutral, rather than negative, equities view from a tactical assetallocation perspective. Diversification does not protect against market risk.

For long-term stock investors who have reaped the massive +520% rewards from the March 2009 lows, they understand this gargantuan climb was not earned without some rocky times along the way.

built up substantial reserve capital while recovering from the Great Recession in 2008-2009. By Taylor Graff, CFA, AssetAllocation Analyst. We are recommending that clients consider high-yield bonds and other asset classes that can offer the prospect of solid gains that diverge from the path of traditional stocks and bonds.

We work with clients to create—either in writing or verbally—a “mission statement” detailing how they want their assets to serve their well-being in coming decades. The “core” allocation is made up of a mix of assets aimed at stability and growth. By Taylor Graff, CFA, AssetAllocation Analyst.

Since the March 2009 low, there have been 17 pullbacks of 5% or more. In the case of risk management via assetallocation, it's the size in stocks versus your size bonds. This doesn't happen suddenly, it slowly builds over time. One of the most important and least spoken about aspects of risk management is position sizing.

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Investment Perspectives | Bubbles II. Wed, 04/01/2015 - 16:48.

Below is the price chart of HUL from Jan 2000 to Jan 2009. If you do not have requisite skill-set or don’t have time, then you should hire an investment adviser who has the expertise to evaluate fair investment valuation and has the experience, temperament and skill-set to alter assetallocation with changing market dynamics and cycles.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

We found there were two times during the tech bubble that stocks gained 20% and again moved to new lows, and it also happened during the global financial crisis of 2007-2009. It was developed a decade ago and is a key input into our assetallocation decisions.

Morgan began tracking this data in 2009. That is the highest level since quarterly data collection began in 2009. . By Taylor Graff, CFA, AssetAllocation Analyst. Protecting inherited assets from a claim by a family member’s ex-spouse can help limit those losses. Dream or Opportunity?

is dragged down by 2008-2009 when the index tumbled 37%. We maintain our preference for equities over fixed income and cash in our recommended tactical assetallocation. References to markets, asset classes, and sectors are generally regarding the corresponding market index. The average of 1.1% How can this be?

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Despite the U.S.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Despite the U.S. Harsh Reaction.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. In terms of the economic cycle, we think the risk of a recession is at its highest level since 2009, but it is still far from a certainty.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. In terms of the economic cycle, we think the risk of a recession is at its highest level since 2009, but it is still far from a certainty.

Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e.,

Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e., Less Efficient Asset Classes.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) 84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009). Company case studies and practitioner-oriented books provide an outlook on the business case for corporate environmental strategies (Esty, 2009).

This work builds on the Capital Asset Pricing Model developed in the 1960s.) 84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009). Company case studies and practitioner-oriented books provide an outlook on the business case for corporate environmental strategies (Esty, 2009).

I’ll tell you something funny and people you know, we never quite had that accusation, but for the better part of 15 years before I started accepting capital, it was, “Hey, everybody’s telling you how to manage your assets the wrong way. And I think that has been true since 2009 until now. You could do it.

I recall one particularly glaring moment during 2009 when AIG became mostly owned by the US government and failed to meet S&P liquidity requirements, but they just ignored it. It forced me to think in a multi-temporal sense which has completely changed how I think about assetallocation.

And suddenly you could buy index funds that cover all of the major asset classes. And then on top of that, of course we ran straight into the 2008, 2009 great recession. And by the summer of 2009, they’d pulled the plug on this venture and suddenly, you know, I’ve thrown away my journalism career to join Citigroup.

Amusingly, about the only content I found was stuff I'd written including this at Seeking Alpha from October, 2009. Where John's approach veers from mine is how complex his portfolio was in 2009. It was an active portfolio though with changes made as necessary. ARBFX 3.7% JRS 3.9% (short position) MERFX 3.7%

The transcript from this week’s, MiB: Ken Kencel, Churchill Asset Management , is below. BARRY RITHOLTZ, HOST, MASTERS IN BUSINESS: This week on the podcast, I have an extra special guest, Ken Kencel of Churchill Asset Management, CEO, Founder, President. This is really a fascinating story. Ken Kencel, welcome to Bloomberg.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content