This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Sherman oversees and administers DoubleLine’s investment management subcommittee; serves as lead portfolio manager for multisector and derivative-based strategies; and is a member of the firm’s executive management and fixed-income assetallocation committees. He is host of the podcast The Sherman Show and a CFA charter holder.

It has been my experience when reviewing portfolios that diversification is typically expressed simply as a number of various stocks owned, or owning a handful of asset classes, usually stocks of various sizes and geographies, and bonds of varying maturities.

He didn't specify which of the two (I believe that is the correct number) funds that Hussman managed back then. For 20 years, holy cow, the numbers look great. The ten year numbers tell a much different story due, I think, to the fund's large allocation to gold. Put it all in the yellow line and forget about then?

Fund managers remain historically conservative per Bank of America’s Global Fund Manager Survey showing assetallocators long cash and short equities. Cash levels rose in March at the fastest pace since last September and remain above average and allocation to equities remains significantly lower than in history.

Barry Ritholtz : The the funny thing is, the behavioral aspect of mutual funds seems to have been when people finally learn about a manager who’s put up great numbers, by the time it makes to make makes it to Forbes, hey, most of that run is probably over and a little mean reversion is about to kick in.

It is very difficult to do but anyone able to pull that off would obviously have a smoother ride and if you play with the numbers, you'd see that you'd come out ahead over the long term. Amusingly, about the only content I found was stuff I'd written including this at Seeking Alpha from October, 2009. ARBFX 3.7%

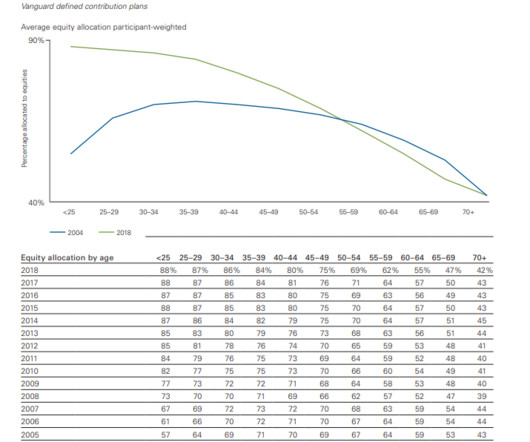

These numbers are pretty encouraging. 18,500, $24,500 for people 50 or older) The chart below shows overall assetallocation in these plans. The biggest takeaway for me here is the cash number. That number fell to 19% in 2018. I wonder if student loans have something to do with this. There is way too much of it.

Mint does a fantastic job of giving you numbers, but falls short on providing any financial insight. You can also get information on your performance and assetallocation. This will help you to create an assetallocation that will get you where you need to go with your investments.

With the wild swings in the stock and bond market this year, it's likely that your assetallocation has gotten a bit out of whack. A portfolio rebalance is simply the act of returning to your pre-determined assetallocation. These numbers assume perfect execution, no transaction costs, and no taxes.

And I think that has been true since 2009 until now. And they do that for 35 years tweaking numbers I go you won, you won the game. Once you have your assetallocation dialed in, your automatic contributions dialed in, all the basics, then you can move on. SETHI: Yes, number one is eating out or dining.

Set hard numbers. After the 2008-2009 financial crisis, many clients could use loss carry-forwards to reduce taxes against gains taken in subsequent years. By Taylor Graff, CFA, AssetAllocation Analyst. During times of market volatility, such long-term planning enables clients to shake off an impulse to sell.

Morgan began tracking this data in 2009. That is the highest level since quarterly data collection began in 2009. . By Taylor Graff, CFA, AssetAllocation Analyst. The momentum helped push up the proportion of European companies beating estimates for second-quarter earnings to 65%, the highest level since J.P.

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Simply stated, asset classes tended to move together: When U.S.

is dragged down by 2008-2009 when the index tumbled 37%. We maintain our preference for equities over fixed income and cash in our recommended tactical assetallocation. The entirety of a recession—particularly a mild one—hasn’t historically been all that bad for stocks from start to finish. The average of 1.1% How can this be?

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. In terms of the economic cycle, we think the risk of a recession is at its highest level since 2009, but it is still far from a certainty.

As head of assetallocation research in our Investment Solutions Group, he is responsible for analyzing the relative attractiveness of various asset classes and investment strategies. In terms of the economic cycle, we think the risk of a recession is at its highest level since 2009, but it is still far from a certainty.

84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009). Finally, a growing number of meta-analyses conclude that incorporating ESG issues into investment decision making generates better returns than comparable non-ESG strategies (Clark, et al., Journal of Environmental Investing 8(1).

84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009). Finally, a growing number of meta-analyses conclude that incorporating ESG issues into investment decision making generates better returns than comparable non-ESG strategies (Clark, et al., Journal of Environmental Investing 8(1).

The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. Reasons for this tendency are varied. In short, every situation is different.

The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. Reasons for this tendency are varied. In short, every situation is different.

The DJIA closed 1999 at 11,497 and 2009 at 10,428. At the GFC bottom, March 9, 2009, the Dow traded at 6,547. ” That may have been a perfectly appropriate assetallocation for Professor Markowitz, of course, but his thinking was far more fear-based than analytically driven. So, he missed it by a mile.

And then I left there and joined a number of my colleagues from Drexel and launched a business that as it turns out, was pretty much a carbon copy of the business we have today. So a very different dynamic than we saw back in 2007, 2008, 2009. Ken was there at the beginning of the private credit markets when he was working at Drexel.

He launched his own firm right into the teeth of the collapse in ’09, which turned out to be quite a fortuitous time to launch an asset management shop. RITHOLTZ: So you’re there for 20 years, from 1988 to 2009. So, you know, 2009, what had happened was I was very burnt out. They wanted to hear a bear story post 2009.

So a lot of the headline names, you see a lot of the stories you see about, about the financial crisis, a significant number of, of those investors we were helping in security selection, modeling, and analytics. And so, so starting in 2009, we, we, there was no flip market. They’re assetallocation model driven folks.

You put a different number on the piece of paper, and that was the moment that I decided I wanted to start the firm. RITHOLTZ: So given those sorts of numbers, the pullbacks, recoveries, what sort of correlations are there with other types of debt, be it performing or distressed equities and other asset classes? RITHOLTZ: Sure.

And then MassMutual combined Barings investing with a number of other shops, including Babson, a very well regarded investing firm. You had a number of bankruptcies going on. Mike Freno : It’s become, it’s become an asset for us to be located there for, for sure. The shop manages about well over $430 billion.

And so graduating right into 2009, right out of the financial crisis, I said, I don’t think I’m gonna get a job. Honest back testing, really looking at the numbers versus exaggerating returns and, and making up the claim that something’s live when it’s not. 12, 14 even that not a lot of numbers.

But our belief is that this economic and profit environment is better than in the early 1990s, early 2000s, or 2008-2009 and therefore supports higher valuations. President Biden’s approval rating has continued to decline amid higher inflation numbers, with a near perfect inverse correlation to gas prices. IMPORTANT DISCLOSURES.

The very first Masters in Business that was broadcast just about 10 years ago, July, 2014, episode number one, Jeffrey Gundlock, DoubleLine Capital. And so I worked a lot on the assetallocation side. Again, as I said, we’ve worked in assetallocation. And effectively I did. That’s right.

And in my career, I feel like the Canadian, they produce a large number of economists. And I remember I wrote a piece basically I think in June 2009, basically saying that the recession was over. It was really in March of 2009. It’s a giant number. And number two, what was the call that Greenspan nailed?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content