This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

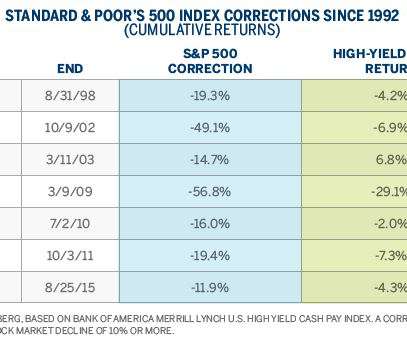

The article lays out 5 reasons why investors should consider adding junk bonds to their portfolios: Junk bonds have been battered this year, and the only other instance in recent history when they were down more than 2022 was in 2008, when they plummeted 26%. But they shot back up 55% in 2009.

And then on top of that, of course we ran straight into the 2008, 2009 great recession. And by the summer of 2009, they’d pulled the plug on this venture and suddenly, you know, I’ve thrown away my journalism career to join Citigroup. And I think it partly depends on the economic comfort in which you grew up.

Through conservative, bottom-up analysis, we are taking advantage of current market dynamics to buy attractively priced debt in companies with solid revenues and limited vulnerability to an economic downturn. Debt in well-managed companies positioned to weather an economic slump return nearly three times the 2.3%

In advising clients over the years, we have seen the value of helping families buy into the longterm orientation essential to successful investing and portfoliomanagement through all market conditions. Therefore, it is essential that we structure client portfolios to be tax efficient. We cannot control the first two forces.

The methods for doing this involve very large data sets that build broad, hypothetical portfolios and back-test them over long periods of time to determine correlations that may define systematic, or beta, risk factors. 84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009).

The methods for doing this involve very large data sets that build broad, hypothetical portfolios and back-test them over long periods of time to determine correlations that may define systematic, or beta, risk factors. 84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009).

Taylor is also an excellent communicator and regularly shares his thoughts with our balanced portfoliomanagers serving private clients, endowments and foundations. Technology has also enabled analysts, portfoliomanagers and traders to improve their productivity. In a word, the internet has changed everything.

Taylor is also an excellent communicator and regularly shares his thoughts with our balanced portfoliomanagers serving private clients, endowments and foundations. Technology has also enabled analysts, portfoliomanagers and traders to improve their productivity. In a word, the internet has changed everything.

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Investment Perspectives | Bubbles II. Wed, 04/01/2015 - 16:48.

We believe this group of alternative assets to be less vulnerable than stocks to the risk of flagging economic growth, and less vulnerable than bonds to rising interest rates. Since 2009, we have identified eight opportunities to shift portfolio allocations to capitalize on a determined upside/downside mismatch. this year, 0.3

War and financial turmoil— the bane of Europe’s economic well-being last century—are currently veiling a rebound in regional growth and unanticipated vigor among European companies. Morgan began tracking this data in 2009. That is the highest level since quarterly data collection began in 2009. . Exceeding Expectations.

She has a fascinating career, starting a PLS working away up as an analyst and eventually, head of outcome-based strategies for Morningstar, eventually rising from that position and portfoliomanager to Chief Investment Officer. So I leave the Bureau of Labor Statistics and I move into economic consulting. NORTON: Right.

Now I do fundamental side research portfoliomanagement, which I just, 00:08:20 [Speaker Changed] So, so you joined GMO, there’s 60 people, 30 years. Dick Mayo was a traditional, I’d say portfolio, strong portfoliomanager focused on US stocks. Jeremy’s never really been a portfoliomanager.

Investors Facing Rising Risks Need Solid Defense, Savvy Offense achen Mon, 09/12/2016 - 02:00 As rising economic and political risk fuels market volatility worldwide, investors need to maintain adequate liquidity, stability and diversification to shield against any protracted economic downturn. France and Germany. small-cap stocks.

As rising economic and political risk fuels market volatility worldwide, investors need to maintain adequate liquidity, stability and diversification to shield against any protracted economic downturn. Innovation and dynamism are alive and well despite several years of low economic growth. Mon, 09/12/2016 - 02:00. versus 1.9

We experienced the largest bull market run in history from 2009 to March 11, 2020. How did these animals become an economic metaphor for market health? Unlike the DOW which tracks 30 stocks, the S&P 500 tracks 500 stocks across all economic sectors. The rise precedes another 20% drop. Introducing Market Indexes.

For a corporation, human capital is crucial to its ability to innovate and to mitigate against operational disruptions, just as it is key to a country’s ability to grow and develop economically. We evaluate each sovereign on key ESG factors that we believe can affect political stability, promote economic growth and drive progress on the U.N.

Our sustainable investing philosophy and process were developed in-house and are supported by a robust team of ESG research analysts, portfoliomanagers and other dedicated professionals. ESG risks and sustainable opportunities ultimately have an impact on a country’s potential for economic growth and political stability.

As with many things in life, the truth is somewhere between the extremes: While both simulated and real-world data suggest momentum may not be suitable as a driver of long-term asset allocations, we believe momentum considerations can be integrated in a cost-effective way to help inform daily portfoliomanagement decisions.

For a corporation, human capital is crucial to its ability to innovate and to mitigate against operational disruptions, just as it is key to a country’s ability to grow and develop economically. We evaluate each sovereign on key ESG factors that we believe can affect political stability, promote economic growth and drive progress on the U.N.

For a corporation, human capital is crucial to its ability to innovate and to mitigate against operational disruptions, just as it is key to a country’s ability to grow and develop economically. We evaluate each sovereign on key ESG factors that we believe can affect political stability, promote economic growth and drive progress on the U.N.

For a corporation, human capital is crucial to its ability to innovate and to mitigate against operational disruptions, just as it is key to a country’s ability to grow and develop economically. For example, social factors are focused on human capital and the ability of a country to increase economic competitiveness through its citizens.

At the risk of oversimplification, it seemed like most of the economic debate during the post-crisis period centered on two main concerns: the strength and durability of the U.S. Slower growth in China, fear of an eventual hard landing and concern that China’s leaders are divided over economic policy. Multiple Risks.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. Reasons for this tendency are varied.

Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. Manager Characteristics. Investment Perspectives - The Great Debate. Wed, 06/21/2017 - 12:35. Reasons for this tendency are varied.

I want to get into that before we start talking about asset management. A degree in mathematics from Oxford, a doctorate in mathematical epidemiology and economics from Cambridge. And you do a lot of work with infinity [Barry Ritholtz] : 00:03:29 [Speaker Changed] And then economics, which is a little bit squishier.

BARRY RITHOLTZ, HOST, MASTERS IN BUSINESS: This week on the podcast, I have an extra special guest, Tom Wagner, co-founder and portfoliomanager at Knighthead Capital. I was like talking through with him how the fund economics worked and what the upside was. So I think those are the things that push me there.

Not, not terribly busy in 2007 to be honest, but in 2008, 2009, 10, it was by far the busiest time in my career in investing. So you have almost a doubling of the interest coupon paid by some of these businesses against the backdrop of c ovid 19 inflation and some of the economic pressures that come with, with those factors.

And Wall Street didn’t work out for a variety of reasons, but I ended up working sort of an adjacent industry in the portfoliomanagement software business, and really wasn’t where my passion was. You know, we do the typical stuff, market economic outlooks and research there, product research. in June of 2009.

You began as a central bank portfoliomanager in Finland. And when I was studying in university economics, I did not really get the passion. So, that relationship actually already started when I was a portfoliomanager, right? Let’s start just by talking about your career. ILMANEN: Yes. RITHOLTZ: Right.

You get a BA in Economics from Hamilton College. So obvious question, it’s 1990, technology is about to explode, how do you help a value manager short of saying, psst, go buy growth? So what we did was we figured out the economic rationale, the macroeconomic influences about why growth and value work at any point in time.

I was a fixed income portfoliomanager and trader, which is a ton of fun. PIMCO out on the West Coast, read the first thing I wrote in the Journal of PortfolioManagement. Some famous periods of reversals in market, the most famous spring of 2009 when we came off the GFC. Program didn’t feel right.

We’ll get to where you work at JP Morgan, but economics bachelor’s from Columbia MBA from Harvard. So I decided to become an economics major and a psychology minor. So the intersection of psychology and economics became really interesting. Christine Philpots. 00:01:37 [Speaker Changed] Thank you for having me.

The economic dislocation, the health risks, just the mayhem that took place, but from the perspective of a number of corporate CEOs, Bill Ackman of Pershing Square Capital, the hedge fund that had a couple of amazing trades based on this. HOFFMAN: So obviously, I’ve — you know, economically minded from the jump.

And I’ll just, you know, go back to, like, I remember Argentina 2009 and meeting with the Finance Minister who not only didn’t know, finance, but didn’t know how to do a debt restructuring. And again, it depends on whether you’re talking about from a political economic perspective, from a GDP perspective.

And so graduating right into 2009, right out of the financial crisis, I said, I don’t think I’m gonna get a job. 00:19:11 [Speaker Changed] The, the challenge is always the transition from the uptrend to the downtrend, which is why you have portfoliomanagers and allocators arguing who’s responsible.

And the second was, of course, the Warren Buffett story that came out the same week, where he essentially called people who post buybacks, you know, economically illiterate. And again, some history, until 2009 or ‘10, Warren Buffett actually spoke out against buybacks. I mean, strong words for Buffett. RITHOLTZ: He was not a fan.

At TCW Barry Ritholtz : You were at the Trust company of the West, you’re a senior vice president, you’re a portfoliomanager, you’re a quantitative analyst. So you mentioned financial repression, you and the rest of the quants in your core group, including gun lock, decide to stand up your own firm in 2009.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content