This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Even with bear markets like 2000-2002 and 2008-2009, the portfolio had strong returns for a very long period. While some of that outperformance was due to improving fundamentals and earnings, most of it the returns came from the valuation investors assigned to these stocks. Source: [link]. The yellow metal then saw two positive years.

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Since 1995, there are four rather distinct periods during which forward earnings estimates for the S&P 500 Index declined, tied to a specific event and/or economic downturn. by year-end.

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. 2009, 10 in that role. But generally starts with the economic cycle. Where are you in the economic cycle?

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Investment Perspectives | Bubbles II. Wed, 04/01/2015 - 16:48.

I think it’s very hard to say stocks are objectively cheap because all of these valuation metrics have, have become unreliable over the decades as the nature of the stock market has changed. And then on top of that, of course we ran straight into the 2008, 2009 great recession. 00:21:46 Everything was a headache.

The challenges are many, with intense cost pressures and slowing economic growth at the top of the list. These headwinds include slower economic growth, cost pressures amid high inflation, ongoing supply chain issues, geopolitical instability in Europe and Asia, and significant currency drag from a very strong U.S. Numerous Headwinds.

I could maybe flip that around a little bit since I think particularly post 2008, 2009, the quality style of investing has become a lot more popular. You really like the long time where you have to hold to make up that valuation whole is so long that you just really shouldn’t be involved. 00:18:41 [Speaker Changed] Yep.

1 Also, from fiscal year 2009 until fiscal year 2016, federal agencies cut annual grants to private and public organizations by 3.4% Rising economic and political risks— including weak global growth and increasing nativism and protectionism in several countries such as the U.S., Charitable giving to foundations in 2015 shrank 3.8%

stock market by China with its zero-COVID policy, which has essentially shut down the world’s 2 nd largest economy and further delayed the full reopening of the global economic game. PRICES: Valuations have come down significantly – Price/Earnings ratio of 15.9 (i.e., Lastly, a wild pitch has been thrown at the U.S. Impeachment.

Market strategists and pundits make the relationship between recessions and the stock market seem binary, but each economic contraction is different and has different effects on earnings. First, keep in mind that stocks tend to look forward by four to six months and can provide warnings of changing economic conditions. How can this be?

I’ve had a coach since 2009. And so, coaching was an exercise — back then in 2009, it was not very well known and it was definitely an exercise in humility of saying, “I think I need some help.” And since we look at both private and public markets, what do you think of in terms of valuation? WEAVER: Yeah.

In 2015, though, three trends began to weigh on stock prices: equity valuations rose above their historical average, record central-bank stimulus failed to fuel faster growth, and corporations, having already wrung out significant inefficiencies, made fewer gains in streamlining and improving profit margins, especially in the U.S.

The median performance, at 25.4%, is a better representation of where stocks might normally be at this stage because it takes out the ferocious V-shaped rebounds coming out of the 2008-2009 Great Financial Crisis and the early stages of the pandemic in March 2020. At the same time, the resilience of the U.S. All index data from FactSet.

When does crowd psychology take hope for economic return beyond what valuation can support? And why do markets irregularly detach fundamentals from valuation to their own detriment? Or is it a convenient way to measure the relative economic value created between our starting and end points? What does this actually mean?

Since the moment the stock market’s deep dive brought on by the Great Recession bottomed out in early 2009 – almost 15 years ago now – recency bias has continued to support the same behavior as home equity bias — buy American stocks! In Chapter One (2000-2009), that almanac will reveal that U.S. Sounds unstoppable, right?

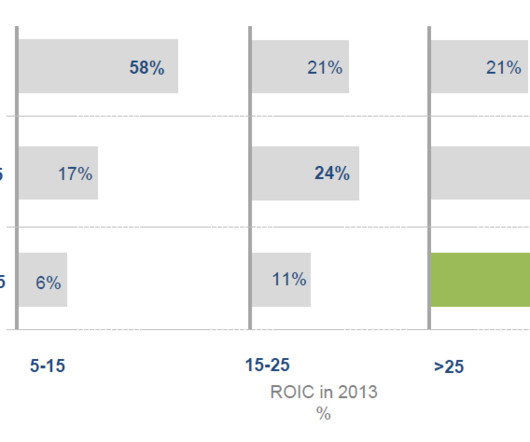

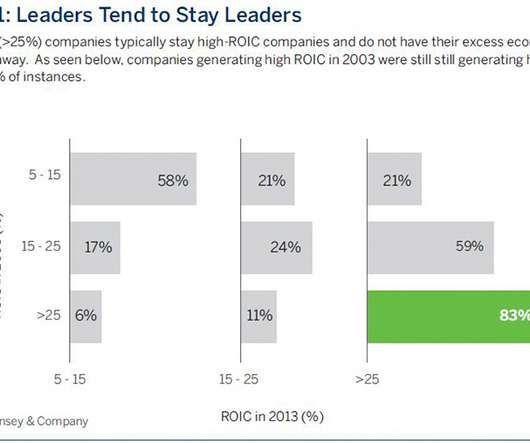

Manager Q&A: Mick Dillon and Bertie Thomson, Global Leaders Strategy achen Fri, 08/25/2017 - 11:34 Indeed a host of macro-economic and political events have impacted global markets since Mick Dillon and Bertie Thomson launched the Brown Advisory Global Leaders strategy. 6th Edition, 2015. ROIC is calculated as % without goodwill.

Indeed a host of macro-economic and political events have impacted global markets since Mick Dillon and Bertie Thomson launched the Brown Advisory Global Leaders strategy. as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition." Fri, 08/25/2017 - 11:34. src="[link] />?. 6th Edition, 2015.

Memories of 2008-2009 are still vivid even though global banks, overall, are in much healthier shape due to stringent regulations put in place following the crisis. The British pound had been weakening for some time amid a backdrop of dollar strength and a poor economic outlook as the U.K. has been wracked by rising energy costs.

So I leave the Bureau of Labor Statistics and I move into economic consulting. And how do we think about them from a valuation perspective? You said earlier, valuations were historically high both stocks and bonds late 2021, right about now, what are we? RITHOLTZ: It’s not March 2009. That’s very funny.

Investors Facing Rising Risks Need Solid Defense, Savvy Offense achen Mon, 09/12/2016 - 02:00 As rising economic and political risk fuels market volatility worldwide, investors need to maintain adequate liquidity, stability and diversification to shield against any protracted economic downturn. France and Germany.

As rising economic and political risk fuels market volatility worldwide, investors need to maintain adequate liquidity, stability and diversification to shield against any protracted economic downturn. Innovation and dynamism are alive and well despite several years of low economic growth. Mon, 09/12/2016 - 02:00.

This helps to meet your immediate needs and instill discipline in a longterm context, averting excessive spending when valuations are rising. After the 2008-2009 financial crisis, many clients could use loss carry-forwards to reduce taxes against gains taken in subsequent years. Ensuring Legacies Last.

While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha. Resource and Energy Economics 41:103-121. Available from [link]. Douglas, E.,

While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha. Resource and Energy Economics 41:103-121. Available from [link]. Douglas, E.,

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

As shown in Figure 2 , the 90% level has historically signaled the start of new bull markets coming off of major lows such as 2009, 2011, 2018-2019, and 2020. Any economic forecasts set forth may not develop as predicted and are subject to change. It is also a major component used to calculate the price-to-earnings valuation ratio.

Which has in turn triggered the more skittish stock investors to run for the exits and completely change their view of our economic future, flooding the financial news with red ink and scary headlines. Now that we’ve covered the background, we can get into some better news: This is all a normal, healthy part of the economic cycle.

A better historical understanding of these events helps us take into account a wider range of possibilities as we consider potential market and economic outcomes in the future. has not seen 10+ year economic expansions, other developed markets certainly have. Valuations are elevated but nowhere near the bubble levels of the late 1990s.

A better historical understanding of these events helps us take into account a wider range of possibilities as we consider potential market and economic outcomes in the future. has not seen 10+ year economic expansions, other developed markets certainly have. Valuations are elevated but nowhere near the bubble levels of the late 1990s.

A degree in mathematics from Oxford, a doctorate in mathematical epidemiology and economics from Cambridge. And you do a lot of work with infinity [Barry Ritholtz] : 00:03:29 [Speaker Changed] And then economics, which is a little bit squishier. What made you add economics to your, to your graduate degree? What is that?

The FSBF offers secured loans to micro-entrepreneurs and self-employed individuals for business purposes, asset creation (home renovation or improvement), or meeting expenses for significant economic events such as marriage, healthcare, and education. Vinay Sanghi has headed the organization since its inception in 2009.

What is behind this sudden surge in the unicorn population, and are some of these valuations “spiraling” out of control? Bull market for public equities: Certainly, the run-up in public market valuations over the past few years has spurred gains in private market values over the same period. Lee coined the term. Rapid Growth.

Exhibit 4 shows marked inconsistency in valuation characteristics for the three largest US equity momentum funds during the value premium rally of late 2020 through early 2021. See, for example, the Fama/French US Momentum Factor’s return of –83.16% in 2009. Up-momentum: Stocks ranking high on prior return relative to the market.

For a corporation, human capital is crucial to its ability to innovate and to mitigate against operational disruptions, just as it is key to a country’s ability to grow and develop economically. We evaluate each sovereign on key ESG factors that we believe can affect political stability, promote economic growth and drive progress on the U.N.

For a corporation, human capital is crucial to its ability to innovate and to mitigate against operational disruptions, just as it is key to a country’s ability to grow and develop economically. We evaluate each sovereign on key ESG factors that we believe can affect political stability, promote economic growth and drive progress on the U.N.

For a corporation, human capital is crucial to its ability to innovate and to mitigate against operational disruptions, just as it is key to a country’s ability to grow and develop economically. For example, social factors are focused on human capital and the ability of a country to increase economic competitiveness through its citizens.

Years later, in April 2009, the news that Morgan Stanley had lost $578 million in the space of three months was shocking enough to make the front page of the Financial Times. Rational measures of valuation had taken a backseat to “mouse clicks and momentum,” as Robertson put it, and he had no stomach for more punishment.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. Reasons for this tendency are varied.

Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. It underperformed primarily during very strong markets, as might be expected given its discipline with regard to valuations.

So I think that argument is very valid in those couple of years, 2009, 2010 probably, maybe 2011, which was a tough year for hedge funds. SEIDES: Yeah, I wouldn’t measure it in terms of economic returns. What’s the valuation? You still had 2012 to 2017 to finish the bet. RITHOLTZ: Right. RITHOLTZ: Right.

Not, not terribly busy in 2007 to be honest, but in 2008, 2009, 10, it was by far the busiest time in my career in investing. So you have almost a doubling of the interest coupon paid by some of these businesses against the backdrop of c ovid 19 inflation and some of the economic pressures that come with, with those factors.

And we’d sort of turn that into a valuation business. MILLER: Well actually I thought, leading up to the great financial crisis, I thought to myself, we’re going to be out of business within a couple of years because nobody wanted an independent valuation. What are the, you know, I’d literally have it in my handheld.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content