This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By Justin Carbonneau ( Twitter | LinkedIn | YouTube ) — Over the past few weeks, I’ve seen a number of charts highlighting the opportunity in small-cap stocks given their absolute and relative valuations. The chart below, also from our market valuation tool, compares small cap value to large cap growth stocks. Only 12.4%

Private Credit Outshines Many High-Valuation Stocks, Bonds. With interest rates at record lows and many publicly traded bonds and stocks approaching historically high valuations, private credit has become increasingly attractive to investors because of its total return prospects, steady income and role in diversification.

Barry Ritholtz : The the funny thing is, the behavioral aspect of mutual funds seems to have been when people finally learn about a manager who’s put up great numbers, by the time it makes to make makes it to Forbes, hey, most of that run is probably over and a little mean reversion is about to kick in.

What makes Graham so interesting is while everybody else in the world of private equity is focused on the analytics and crunching numbers and creating econometric models that will tell you where to invest, I think they’ve found a very different model that has been extremely successful for them, where the key focus is on talent.

at year-end can largely explain the compression in valuation, especially for higher multiple equities, primarily during the first half of the year. Great Financial Crisis October 2007 April 2009 -39.0% 3/9/2009 4/30/2009 69 29.0% at the beginning of the year to 16.6x by year-end. to nearly 3.9% 9/21/2001 12/31/2001 52 18.9%

He didn't specify which of the two (I believe that is the correct number) funds that Hussman managed back then. For 20 years, holy cow, the numbers look great. The ten year numbers tell a much different story due, I think, to the fund's large allocation to gold. Put it all in the yellow line and forget about then?

20,000 is not just a number; but happiness for many. Nifty 50 first hit 10,000 on July 26, 2017, and it took years to double that number. Amid all the noise surrounding geopolitical issues, global valuations, and FII selloff, the Nifty bulls might be feeling a bit clueless about their next moves. on July 20 of this year.

One other factor at play are valuations. Did high valuations add fuel to sellers' fire? I tend to think that valuations don't matter during panic selling. The long run average, which includes numbers from the 1800s, should be taken with a huge grain of salt.

And so there was a number of less liquid markets that made for quite wide spreads. And so there was certainly a number of different movements, but there was certainly downside of these things. And you know, I think ultimately there was a number of opportunities that came out. And so we have a number of business lines.

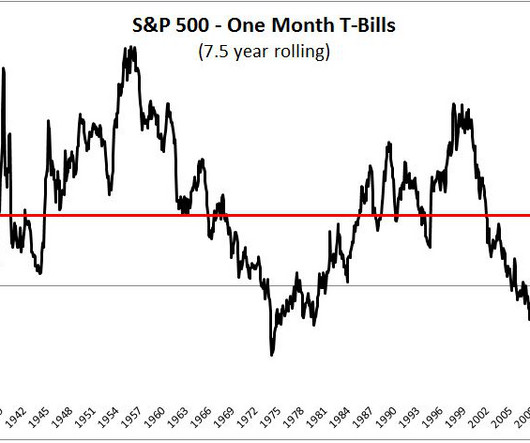

This range is determined by a number of factors, including but not limited to the business cycle, valuations, interest rates, inflation, and the collective mood of millions of investors. They're not wrong, since the bottom in 2009, stocks have outperformed risk free bills by 17.5% a year, the largest spread over a 7.5

He has a very interesting approach to thinking about market valuations and strategies and when to deploy capital, when to go with the crowd, when to lean against the crowd, and has amassed and excellent track record. 2009, 10 in that role. Second part of our framework is valuation fundamental work. Is low, right?

Almost exactly five years ago, we wrote a piece entitled Bubbles, which discussed the sharp rally in stocks from the lows of early 2009 and the risks of the growing federal deficit that resulted from government bail-outs and fiscal stimulus during the financial crisis. Investment Perspectives | Bubbles II. Wed, 04/01/2015 - 16:48.

Graham Foster] : 00:02:54 That was a number, that was number theory, pure number theory. And whether it’s all numbers or even numbers. Some people look at a casino as entertainment and hey, we’re gonna spend X dollars, pick a number, 500, 2000, whatever it is. Number one, longevity.

Investor enthusiasm, coupled with high valuations, has preceded all major market bubbles. stocks are based on traditional valuation metrics, via Michael Cembalest. In the decade since 2009, there have been regular claims that we were back in a bubble, but the FCF yield suggested valuation was not stretched.

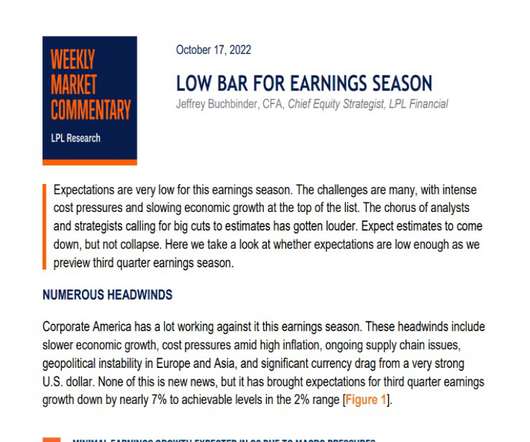

That means that the other 10 S&P sectors will likely see an earnings decline even if numbers come in better than expected, as they almost always do. While the pundits are mostly focused on what can go wrong this earnings season, there are several reasons to expect the numbers for this quarter to be decent. Quincy Krosby , Ph.D.

The stock market has increased more than 7-fold in value since the 2009 stock market lows, even in the face of many frightening news stories (see Ed Yardeni’s list of panic attacks since 2009 ). COVID, inflation, and Federal Reserve monetary policies may dominate the headlines du jour but this is nothing new.

Felix outlines a number of ways to combat the cost of pessimism, including checking your investments less frequently and finding ways to automate your investing contributions, among others. Over the last 25 years, we have seen four bear markets (1999-2002, 2008-2009, 2020, 2022) and numerous market corrections (10% losses).

In 2013, she applied it to the small number of privately held companies with a market value over $1 billion to denote their rarity. What is behind this sudden surge in the unicorn population, and are some of these valuations “spiraling” out of control? Lee coined the term. It’s now worth an estimated $51 billion just two years later.

And I did the math, and I think at that point in time, roughly speaking, assets in ETS were roughly just 10 percent, 12 percent of assets in mutual funds and I was pretty convinced that that number was to increase significantly. I was employee number 10. RITHOLTZ: Which is really a pretty big number. billion dollars in AUM.

So there are a number of us heading in out of college into the BLS. And how do we think about them from a valuation perspective? You said earlier, valuations were historically high both stocks and bonds late 2021, right about now, what are we? RITHOLTZ: It’s not March 2009. I was on the Producer Price Index.

is dragged down by 2008-2009 when the index tumbled 37%. Stock valuations are higher but bond yields are still low enough to support valuations with the 10-year Treasury yield well under 3% despite the big jobs number. It is also a major component used to calculate the price-to-earnings valuation ratio.

Stocks flooded the market, and valuations stretched into the stratosphere. The number of tech stocks exploded from under 300 at the beginning of 1995 to 952 at the bubble's peak. By the time its stock was back at all-time highs in 2009, it had done $21.69 Sound familiar? At its peak in 1999, Amazon did $1.64 billion in revenue.

When the current bull market inevitably turns, passive managers could be left holding stocks and sectors with poor fundamentals and inflated valuations. Being that we don't know when the bull market will "inevitably turn," why don't we look at some actual numbers. From 2000 to 2009, active outperformed passive nine out of 10 times."

In the multiyear bull market we’ve experienced since 2009, shareholders perceive these situations as persistently mediocre. These factors have combined to drive a number of spinoffs in the industrial sector of late, and in many cases these worked out very well for shareholders. Struggling under their own weight.

Set hard numbers. This helps to meet your immediate needs and instill discipline in a longterm context, averting excessive spending when valuations are rising. After the 2008-2009 financial crisis, many clients could use loss carry-forwards to reduce taxes against gains taken in subsequent years.

When does crowd psychology take hope for economic return beyond what valuation can support? And why do markets irregularly detach fundamentals from valuation to their own detriment? as featured in the book, “Valuation: Measuring and Managing the Value of Companies, University Edition.” In his book “What is Time?

Instant access to information allows analysts to monitor a greater number of stocks, and portfolio managers are able to analyze their holdings and track performance in myriad ways. Valuations are elevated but nowhere near the bubble levels of the late 1990s. The short answer is that it’s very much a mixed picture.

Instant access to information allows analysts to monitor a greater number of stocks, and portfolio managers are able to analyze their holdings and track performance in myriad ways. Valuations are elevated but nowhere near the bubble levels of the late 1990s. The short answer is that it’s very much a mixed picture.

True to form, she got back to me within just a few minutes with these thoughts: MMM: How should potential retirees think of the recent crash in valuation – has it really pushed out their retirement date, or not? It’d be like retiring at the bottom of 2009 with still-decent numbers. Data source: S&P market data.

The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. Reasons for this tendency are varied.

The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. Reasons for this tendency are varied.

Years later, in April 2009, the news that Morgan Stanley had lost $578 million in the space of three months was shocking enough to make the front page of the Financial Times. Rational measures of valuation had taken a backseat to “mouse clicks and momentum,” as Robertson put it, and he had no stomach for more punishment.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

From a longer-term perspective, stocks rose from 2009 until this recent correction with only a few setbacks along the way. increase in the average hourly wage rate, the fastest rise in that rate since 2009. (It Even after recent record-setting gains, investors remained positive about the prospects for further profits. 2, the U.S.

84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009). Finally, a growing number of meta-analyses conclude that incorporating ESG issues into investment decision making generates better returns than comparable non-ESG strategies (Clark, et al., Journal of Environmental Investing 8(1).

84 One study concluded that investors "pay a financial cost in abstaining from [sin] stocks" (Hong, 2009). Finally, a growing number of meta-analyses conclude that incorporating ESG issues into investment decision making generates better returns than comparable non-ESG strategies (Clark, et al., Journal of Environmental Investing 8(1).

Or at least the top, pick a number, 30, 40%. I don’t remember the number. ” 29, 87, 74, just pick any 50 plus percent number and certainly 2000 and ’08, ’09, a major index gets cut in half. So you’re talking about an average of a large number. What’s the valuation? Less, 20, 30%?

Our in-house Sovereign Sustainability Score provides an initial indication of a country’s performance from over 30 indicators across a number of factors. However, there may be opportunities to own corporate debt within Brazil to take advantage of strong commodity prices and improved balance sheets and valuations.

Our proprietary Sovereign ESG Score provides an initial indication of a country’s ESG performance from over 30 indicators across a number of ESG factors. However, there may be opportunities to own corporate debt within Brazil to take advantage of strong commodity prices and improved balance sheets and valuations.

Our proprietary Sovereign ESG Score provides an initial indication of a country’s ESG performance from over 30 indicators across a number of ESG factors. However, there may be opportunities to own corporate debt within Brazil to take advantage of strong commodity prices and improved balance sheets and valuations.

And I literally put the entire Schedule A, which is the pricing square footage unit numbers in a Hewlett Packard 41B using bit mapping. And we’d sort of turn that into a valuation business. Everybody knew the number but the appraiser. What are the, you know, I’d literally have it in my handheld. Just keep it fair.

Not, not terribly busy in 2007 to be honest, but in 2008, 2009, 10, it was by far the busiest time in my career in investing. Ritholtz ] 00:09:37 I recall reading, and I know you can’t say this, but I recall reading that fund return something like 19% a year, some just astounding number. Crazy number. Some, some, yeah.

The DJIA closed 1999 at 11,497 and 2009 at 10,428. At the GFC bottom, March 9, 2009, the Dow traded at 6,547. 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.” 2020 : “[E]xtreme valuations. So, he missed it by a mile. percent in losses.

I was thinking any number of things and mostly that I didn’t really know what I wanted to be when I grew up, but I was not kind of at all informed by, you know, gender norms that people asked me a lot about now, in particular how do you know a woman, how did you think about ending up in this thing? MCCARTHY: Yeah, absolutely.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content