This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

With that preamble, I started thinking about the 75/50 portfolio that I first started writing about during the Financial Crisis. I've mentioned 75/50 a couple of times in passing but the big idea was to create a portfolio that captures 75% of the upside of the equity market with only 50% of the downside. ARBFX 3.7%

There's no fact sheet yet and while the holdings are available, the assetallocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly). It has been challenging as we've talked about in other posts recently but I believe the 2010's were even worse. Offering diversified exposure to U.S.

GAA stands for Global AssetAllocation and it has been lagging for 15 years. This brings us to the heart of today's post about trying to build a set but don't completely forget portfolio. This slice of the portfolio will go down more often than not, it is a tool to smooth out the ride.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks. Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. Thu, 06/01/2017 - 02:47.

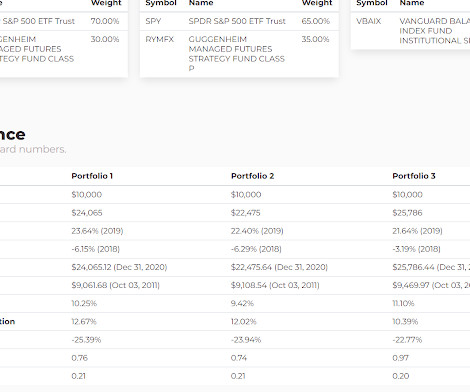

Below are two nearly identical portfolios; both are sixty percent stocks and forty percent bonds. Each portfolio has twelve slices, with identical allocations in each sleeve. For example, portfolio 1 has a 10% position to U.S. Portfolio 2 also has a 10% position to U.S. Portfolio 2 sold after the 23.3%

They help with assetallocationAssetallocation is an important component of successful retirement planning, and working with the best financial advisors for retirement can provide invaluable guidance in navigating this complex terrain. This can help optimize your wealth accumulation while mitigating unnecessary risks.

We have seen strong, strong demand pretty consistently for building out alternatives, portfolios, particularly when it comes to opportunities with great financial sponsors on the private equity side, looking at these long-term secular trends, right? RITHOLTZ: Let’s talk a little bit about inflation. You mentioned 8.5 percent inflation rate.

Her job is portfolio and product solutions and that means she could go anywhere in the world and do anything. I thought this conversation was absolutely fascinating and I think you will also, with no further ado, Goldman Sachs asset managements Elizabeth Burton. That sounds great, but I only have spots in my portfolio for a Cape Cod.

At Carson Investment Research, we have moved our longer-term strategic assetallocations to their maximum equity overweight while continuing to favor U.S. 3% in 2023 after adjusting for inflation, which would be above the 2010-2019 trend. That is why we seek to control risk in our portfolios. Here’s why.

Initially I joined to help them manage their equity portfolio. My background in the asset management space was originally going to small cap value, and Canyon Partners really gave me the platform that allowed me to branch that out into multiple different areas. I’m gonna hold it in my portfolio. I buy everything.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets.

Ever since Taylor joined our firm in 2010, I’ve been deeply impressed with his understanding of the markets and his intellectual curiosity with respect to all types of investments. Technology has also enabled analysts, portfolio managers and traders to improve their productivity. In a word, the internet has changed everything.

Ever since Taylor joined our firm in 2010, I’ve been deeply impressed with his understanding of the markets and his intellectual curiosity with respect to all types of investments. Technology has also enabled analysts, portfolio managers and traders to improve their productivity. In a word, the internet has changed everything.

And I remember being on the phone thinking, as the PMs were asking questions about cash flows and things, I was thinking, you’re asking all the wrong questions about whether this portfolio will perform because it’s things like down payment. So she wants her portfolio managed that way. That’s not a terrible thing.

Thus, since early 2010, earnings growth of close to 85% has accounted for the vast majority of the doubling in stock prices. In 2010, the economic expansion was widely forecast to be weak, and indeed it turned out to be slower than in most postrecession periods. Diversification Should Help.

Our research contacts with a large number of companies in client portfolios tend to confirm that demand growth remains very much intact. which has declined from over 6% at the end of the financial crisis in 2010 to less than 2.5% Spending has been supported recently by a reduction in the personal savings rate in the U.S.,

Our research contacts with a large number of companies in client portfolios tend to confirm that demand growth remains very much intact. which has declined from over 6% at the end of the financial crisis in 2010 to less than 2.5% Spending has been supported recently by a reduction in the personal savings rate in the U.S.,

Invariably, the question behind the question is, “Should I be doing something different in my portfolio?” If only we could find them, our portfolios would do so much better. How would her hypothetical portfolio have performed over the past 50 years following this simple annual readjustment strategy? Consider Felicity Foresight.

In The Next Great Bubble Boom: How to Profit from the Greatest Boom in History: 2006-2010 , published in January 2006, Dent doubled down on his earlier predictions for the 2000s and called for big gains through the rest of the decade. who became a professor at the University of Michigan before setting up his own asset management firm.

So when you think about the individual exposure to a specific name, in our funds, it represents less than one half of 1 percent of the portfolio. Arcmont, one of the early adopters in Europe, they actually launched their firm back in 2010, 2011. So we saw an opportunity to really partner with a leader in the same business as us.

And I was a portfolio manager, so I was doing bottom up research and picking stocks. He wasn’t tactical assetallocator. Hey, if you knew with perfect clarity, if that bird landed on your shoulder and told you here’s where equity prices are gonna be in 10 years, position your portfolio for that.

Fisher, 1958 The Money Game - George Goodman, 1967 A Random Walk Down Wall Street - Burton Malkiel, 1973 Manias, Panics, and Crashes: A History of Financial Crises - Charles Kindleberger, 1978 The Alchemy of Finance - George Soros, 1987 Market Wizards - Jack Schwager, 1989 Liar's Poker - Michael Lewis, 1989 101 Years on Wall Street, An Investor's Almanac (..)

At TCW Barry Ritholtz : You were at the Trust company of the West, you’re a senior vice president, you’re a portfolio manager, you’re a quantitative analyst. And so I worked a lot on the assetallocation side. Again, as I said, we’ve worked in assetallocation. Signs him, right?]

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content