This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The transcript from this week’s, MiB: Mike Greene, Simplify Asset Management , is below. We have to pay attention to this, and we have to understand why this is potentially a risky asset. We built a company that was focused on valuation, initially, actually targeting corporate strategic planning departments.

His model is both conservative and disciplined, focusing on balance sheet strength and attractive valuations. Strong Liquidity (Current Ratio 2) A companys current assets must be at least twice its current liabilities, ensuring financial stability. Reasonable Price/Book Ratio (P/B P/E 22) A safeguard against excessive valuations.

The basic concept is when one of these asset classes starts a long move, they tend to go much further and much longer than people typically expect, and you want to capture as much of that move as possible. So different time horizons, different assets. What assets are they in? I don’t know if all our listeners are.

Mortgage-Backed Security (MBS) Index was trading at an option-adjusted spread of 65 bps, which ranked in the 91st percentile since 2010. We believe moves in the asset class have been overdone and that current valuations present an opportunity. As of April 25, the Bloomberg U.S.

No 685845 1.50% 12 MONEYLICIOUS SECURITIES PRIVATE LIMITED No 681706 1.49% 13 5PAISA CAPITAL LIMITED No 536009 1.17% 14 INDMONEY PRIVATE LIMITED No 493779 1.08% 15 MIRAE ASSET CAPITAL MARKETS ( INDIA ) PRIVATE LIMITED No 483858 1.06% Please note that the total number of active clients of all stockbrokers is 4,56,71,347 (4.46 lakh clients).

When he began, PE was a little bit of a niche boutique sort of investment, and over the ensuing 25 years, it has grown to be really a major asset class with giant opportunities that have been expressed by then small, now very large companies, of which Blackstone is one of the largest. It is an institutionalized asset class.

You mentioned in the beginning of the book lower asset yields and richer asset prices have pulled forward future returns. ILMANEN: It’s always good to think of starting yields and valuation sort of two sides of the same coin. RITHOLTZ: Really quite interesting. Explain that. Bonds are the most expensive. Stocks are pricey.

John Furey and I discuss: John’s thoughts on the 2005-2010 “breakaway movement” that created so many new RIAs versus where the industry is today. Why there is a disconnect between the valuation level of private advisory firms and publicly traded firms. .”

Valuation/Prices at which you invest (the difficult part) Now, if you do some thorough research and gain some insight to feel confident about better future growth prospects of any particular sector/theme you can still lose a significant amount of money or get poor returns even if your understanding was right. Let me share two examples: 1.

No, I — the first thing I spoke at was a Goldman Sachs Asset Management conference, strange enough in a place called Carefree, Arizona. And he did — when I met him, let’s say in 2010, he acknowledged that they’ve got things wrong. Jeremy called and said, “Would you like to join the asset allocation team?”

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/31/2010 1.4% 12/31/2010 26.1% And with intangible assets rising in the economy, standard earnings calculations are becoming less and less accurate. By Jack Forehand, CFA, CFP® ( @practicalquant ) —.

They advise or directly manage about $250 billion in flying assets. RITHOLTZ: So how do you find your way from economist to analyst to asset manager? RITHOLTZ: You said, I know, I want to run assets. RITHOLTZ: What was that experience like beginning in asset management in the aisle of hurricane? NORTON: Yeah.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. Some might argue that the Fed’s policy could trigger another crisis as asset prices become overly inflated.

2010 - Have Cash, Wait for Stocks to Fall 2011 - Grantham sees most global equities as ranging from “unattractive” to “very unattractive” – valuing the S&P 500 at “no more than 950.” Investor enthusiasm, coupled with high valuations, has preceded all major market bubbles. You can’t have your cake and eat it.

And much like the investors and analysts who didn’t heed his warnings in 2008 or in the years since regarding the Dodd-Frank Act of 2010 and loose monetary policy, he doesn’t expect many to listen to him now. He also pointed to gold, which many have added to their portfolios as a stable asset. But for long-term prosperity in the U.S.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Asset allocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is not particularly notable. is much clearer.

Asset allocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. 30, 2010, this underweighting was the largest positive contributor to the model’s relative performance out of all of our asset allocation decisions.

And before that, Morgan Stanley, doing technology and operations planning for the wealth and asset management group. What percentage of the assets are in ETFs relative to mutual funds? So fast forward to where we are today, we have over $40 billion in assets under management. BERRUGA: You know, great question. BERRUGA: Exactly.

Any asset subject to such sharp swings may be catnip for traders but of limited value either as a reliable medium of exchange (to replace cash) or as a risk-reducing or inflation-hedging asset in a diversified portfolio (to replace bonds). Assessing the merits of bitcoin as an investment can be problematic. Dimensional Japan Ltd.,

Where we differ, is that he allocates his "side" portfolio to one asset - Facebook. I try to highlight the dangers of being as concentrated in one asset as he is. I'm going back to 2010 and assuming a portfolio that invested $1,000 into each of Apple, Amazon, Google and Netflix, and never rebalanced. Consistently, and by a lot.

Background Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways. Background.

The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. The second, and what’s interesting about that period, is the fact that valuations actually peaked in 1961. MIAN: Valuations are ebb and flow. RITHOLTZ: So let’s take a couple of examples.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Despite the U.S.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Despite the U.S. Harsh Reaction.

Related reading: SPAC vs. Traditional IPO: Valuation, Lockup Period, and Employee Equity Founders have more options for reducing the tax consequences of an acquisition Founders are generally in the best position to engage in tax planning and limit the taxable consequences associated with an acquisition.

According to quarterly Federal Reserve data, money market assets were more than $6 trillion at the end of the third quarter of 2023, roughly double what they averaged from 2011 to 2017. The average yield from 2010-2021 was just 2.34%. As noted above, the yield to maturity for the Agg on Jan. 16 was 4.65%.

Ever since Taylor joined our firm in 2010, I’ve been deeply impressed with his understanding of the markets and his intellectual curiosity with respect to all types of investments. Valuations are elevated but nowhere near the bubble levels of the late 1990s. In the wider context of history, however, these “analyses” seem simplistic.

Ever since Taylor joined our firm in 2010, I’ve been deeply impressed with his understanding of the markets and his intellectual curiosity with respect to all types of investments. Some observers are comforted that recessions since the 1970s have been preceded by oil price spikes or asset bubbles—conditions that do not exist today.

SEIDES: But market returns across — RITHOLTZ: The past decade, 2010 to 2020, we were what? So if you start with the S&P 500 or in this case stocks and bonds, you only have two asset classes, right. So the proper benchmark for those pools has to look a little bit like the underlying assets they’re investing in.

which has declined from over 6% at the end of the financial crisis in 2010 to less than 2.5% The future course of interest rates is probably the greatest single concern for investors today, from both a fundamental and a valuation perspective. Spending has been supported recently by a reduction in the personal savings rate in the U.S.,

which has declined from over 6% at the end of the financial crisis in 2010 to less than 2.5% The future course of interest rates is probably the greatest single concern for investors today, from both a fundamental and a valuation perspective. Spending has been supported recently by a reduction in the personal savings rate in the U.S.,

The Company was awarded the Maharatna status in 2010. 9,212 crore and capitalized assets of Rs. The Company currently trades at a PE valuation of 11.73x, which is slightly higher than its peer Maharatnas. ONGC was set up under the leadership of Pandit Jawahar Lal Nehru, in 1955. It also made a Capital Expenditure of Rs.

And since we’re looking for narratives as opposed, and then do valuation work second as opposed to cheap, we don’t screen. From 2010 to 2014, we were fine, but then things got a little tougher in 2015 and we ran through five years where we had two awful years and three mediocre years. How, how do you manage around that?

She and her team manages over $565 billion in real estate assets. Kathleen has been with Blackstone since 2010. But I’d say those are all similar things, whether you’re talking about, you know, companies that make something, or companies that own real estate or real estate assets. And real estate offered that.

In The Next Great Bubble Boom: How to Profit from the Greatest Boom in History: 2006-2010 , published in January 2006, Dent doubled down on his earlier predictions for the 2000s and called for big gains through the rest of the decade. who became a professor at the University of Michigan before setting up his own asset management firm.

A prohibition on IRAs holding investments open only to those with a certain level of assets – such as investments open only to Accredited Investors. The elimination of certain valuation discounts frequently used in connection with estate planning transactions. Gift/Estate/GST Tax. Corporate Income Tax. Carried Interests.

He wasn’t tactical asset allocator. And the sort of narrative embedded in that, I suppose might matter to institutions, but our eight plus trillion dollars of client assets are for the most part individual investors. He is just, he’s just bearish all the time. It wasn’t the case. 1987 is a perfect example of that.

The firm plans to hit $10 trillion in client assets over the next decade. Known as the Dean of Valuation, he teaches Corporate Finance and Valuation to the MBA students at Stern where he has been voted “Professor of the Year” by the graduating M.B.A. His Next Act Is No Less Ambitious. class nine times.

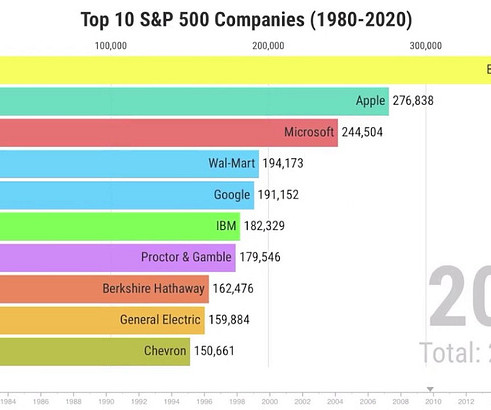

In 2010, Exxon stayed at number one (oil prices had skyrocketed over the previous ten years), Microsoft moved up to third, GE fell to fifth, and Walmart stayed sixth, but only Exxon grew its market cap significantly (Microsoft’s was basically flat; GE’s and Walmart’s fell). All 1990 list members are gone by 2010.

He really is one of the most knowledgeable people in this space, and not just knowledgeable in the abstract, but helping to oversee just about a hundred billion dollars in client assets. And so I worked a lot on the asset allocation side. Again, as I said, we’ve worked in asset allocation. And so it’s not just me.

Low rates also raise valuations for business acquisitions. Berkshire is willing to pay some small amounts now for money it can’t really employ in order to have it available when something good comes along—like the deals Berkshire struck in 2008-09 when others were forced to sell assets at low prices or raise capital at high cost.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content