This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Taxplanning serves as the cornerstone of the entire acquisition deal, extending far beyond a simple checkbox. Every element, from structure to price negotiations, hinges on understanding tax implications for all parties involved. Get it right, and you will have set yourself up for a smooth transition and maximized returns.

Founders, board members, and employees of startups that get acquired can experience tax consequences as a result of a liquidity event. It’s imperative to plan for the tax implications so you can be prepared to pay what you owe the IRS.

Breathe Easier Next Tax Season with These Planning Strategies Every year, most of us smile when we see April 15th in the rearview mirror. The completion of our tax returns being filed marks the beginning of a nine month period where we don’t need to think about funny acronyms and form numbers. 401(k), 403(b) etc.)

They help with asset allocation Asset allocation is an important component of successful retirement planning, and working with the best financial advisors for retirement can provide invaluable guidance in navigating this complex terrain. This ultimately optimizes the likelihood of achieving your desired outcomes over the long term.

SEIDES: But market returns across — RITHOLTZ: The past decade, 2010 to 2020, we were what? Was that the plan or was he just going to announce it? That was never part of the plan, didn’t happen. It’s part of their own taxplanning. RITHOLTZ: Oh no, it’s much worse. SEIDES: It’s lower.

For federal income tax purposes, structuring transactions and planning for capital gains exclusions related to QSBS are crucial. Unfortunately, the Commonwealth also passed a ‘millionaire tax’, which adds a 4% surtax to taxable income over $1M , even for one-time sudden wealth events.

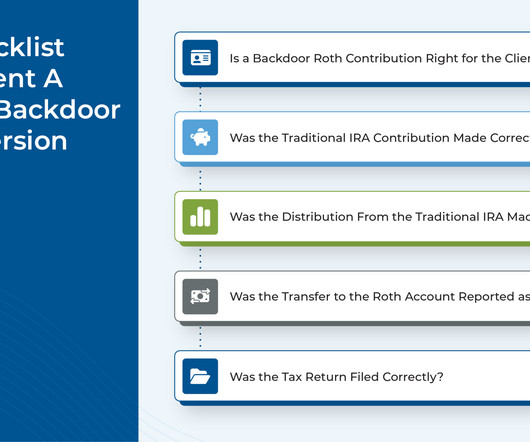

The Long Game: Roth Conversions & Legacy Planning ajackson Thu, 08/01/2019 - 14:51 Legacy planning is all about transferring wealth to descendants as efficiently as possible. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

The Long Game: Roth Conversions & Legacy Planning. Legacy planning is all about transferring wealth to descendants as efficiently as possible. Since January 1, 2010, all individuals, regardless of income levels, have been able to convert existing retirement accounts such as traditional IRAs into Roth IRAs. Background.

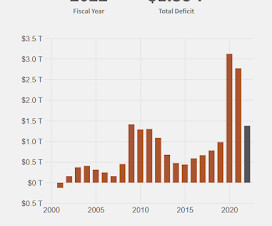

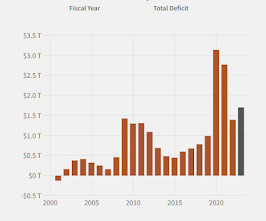

The CBO projections showed an almost $6 Trillion in debt reduction in the 2001 through 2010 period. 3) Bush Tax Cuts: These tax cuts were sold as slowing the growth of the surpluses (using Greenspan's speech for cover)! Instead, the tax cuts (mostly for the wealthy) turned the surpluses into deficits and reduced revenue by $1.5

The CBO projections showed an almost $6 Trillion in debt reduction in the 2001 through 2010 period. 3) Bush Tax Cuts: These tax cuts were sold as slowing the growth of the surpluses (using Greenspan's speech for cover)! Instead, the tax cuts (mostly for the wealthy) turned the surpluses into deficits and reduced revenue by $1.5

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content