This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

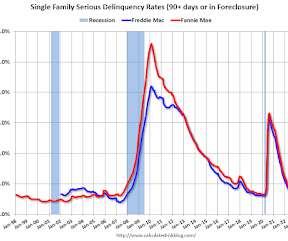

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.41% are seriously delinquent (down from 2.48% in August).

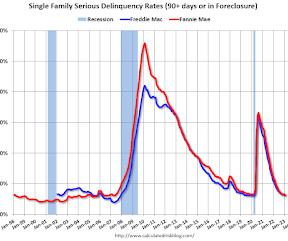

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.15% are seriously delinquent (down from 2.34% in October).

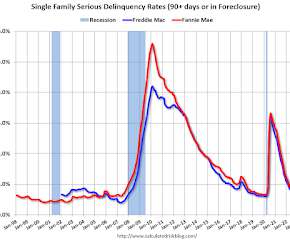

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 1.93% are seriously delinquent (down from 2.04% in February).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.16% are seriously delinquent (down from 2.15% in November).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.34% are seriously delinquent (down from 2.41% in September).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.60% are seriously delinquent (down from 2.75% in June).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.48% are seriously delinquent (down from 2.60% in July).

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.04% are seriously delinquent (down from 2.11% in January).

What’s obvious is that cheaper is better than more expensive; that there are inherent costs in managing an active portfolio that include more than just trading and taxes but research, analysis, PMs, etc. Morningstar, August 9, 2010. Concentrated portfolio risk. Russel Kinnel. Passive investing is: Marxist. Reached a mania.

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic. Click on graph for larger image By vintage , for loans made in 2004 or earlier (1% of portfolio), 2.75% are seriously delinquent (down from 2.86% in May).

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic. The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

Investors should be considering capturing some of that yield in their portfolios. We’re going to discuss how these changes are likely to affect your portfolios and what you should do about it. My stock portfolio is recovering. This is not the 2009, 2010 to 2020 period where basically all you needed was.

Consider: From 2010 through 2021, The S&P500 Index gained 330% — a little over 13% annually (not including dividends). But here is the unexpected thing about those predictions: Even if your forecast of future events is correct, the odds are against you capturing it in your portfolio. What’s already priced in?

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic. The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

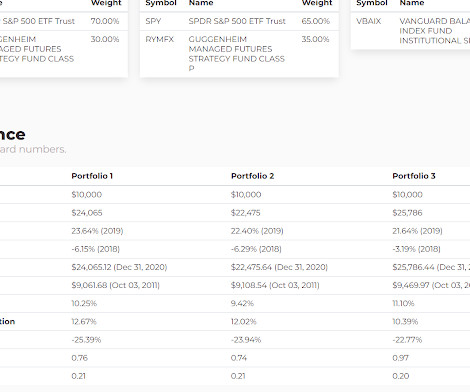

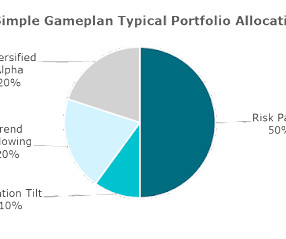

The idea is that you get the full beta (stocks and bonds) return with just a portion of the portfolio often with futures or some other form of leverage, leaving dollars left over to add alternatives all in pursuit of better nominal returns or better risk adjusted returns. The fourth portfolio more closely aligns with what we do here.

With that preamble, I started thinking about the 75/50 portfolio that I first started writing about during the Financial Crisis. I've mentioned 75/50 a couple of times in passing but the big idea was to create a portfolio that captures 75% of the upside of the equity market with only 50% of the downside. ARBFX 3.7%

This blog has pretty much evolved into 100 ways to build a portfolio without bonds. financial advisers are kidding you if they say they are 'positioning' your portfolio for a specific interest-rate scenario. I found an interview I did with Seeking Alpha in late 2010 that made its way to NASDAQ.com. This is an important point.

Some interesting conversations and the like related to portfolio construction and the use of alternative strategies. Nomadic Samuel kicked it off on Twitter with the following portfolio in a poll, asking whether a simple two fund, equity/bond 60/40 portfolio made more sense.

Since its inception on Validea in 2003, the models 10-stock, annually rebalanced portfolio has returned 825% , outperforming the S&P 500 by 361.8%. This portfolio is set to be rebalanced in June 2025, so you can follow the portfolio by accessing Validea today. Returns are model returns and do not reflect actual trading.

For a few years in the 2010's, I had a side gig working for ETF provider AdvisorShares. When I put together that they were running a capitally efficient portfolio I decided I wanted to play around with the 3x funds little bit here. None of the portfolios are leveraged up.

Mutiny Funds put out a paper on the hows and whys of using alts for The Cockroach Portfolio that they manage and that we've looked at a few times. Picture retiring in 2010 versus 2020. The S&P 500 was down 22% for the 10 years ending 1/1/2010 while the ten years ending 1/1/2020 it was up 189%.

This brings us to the heart of today's post about trying to build a set but don't completely forget portfolio. This slice of the portfolio will go down more often than not, it is a tool to smooth out the ride. Referencing the weightings above, all of the portfolios have 65% in equity beta. In real life, I don't have that much.

The 2010's was a rough decade for managed futures in nominal terms. 90/40 had a higher CAGR than traditional 60/40 but lower than 60% equities/40% managed futures in Portfolio 3. The advantage that both managed futures portfolios had over traditional 60/40 is how well they did in 2022.

It’s a very low cost and tax efficient way to get access to a diversified portfolio. At the same time, you might have components of your portfolio that are inherently short-term (such as cash or T-Bills), but in the aggregate your portfolio will likely have a time horizon of 5, 10 or 20 years.

There's no way to fit that many into a portfolio without having a portfolio of diversifiers hedged with a little bit of equity exposure which I don't think would be optimal. It has been challenging as we've talked about in other posts recently but I believe the 2010's were even worse. I'd say it's pretty close.

When we talk about expat living, I always say to not sell your house, to rent it out and live off the rental cash flow, allowing Social Security and the portfolio to grow. We've been saying for years, as the strategy was lagging throughout the 2010's, it was doing what it should, maintaining its negative correlation to equities.

If you've done research on managed futures then you've probably read what a rough decade the 2010's were for the strategy. Maybe it's as simple as equities went up a lot but either way from 2010 through 2019, RYMFX negatively compounded at 2.07% and AQMIX compounded annually at a positive 77 basis points.

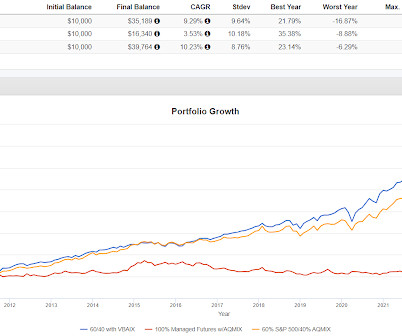

There was some interesting reading today looking at various portfolio construction and strategy issues. lagged far behind the Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 portfolio. lagged far behind the Vanguard Balanced Index Fund (VBAIX) which is a proxy for a 60/40 portfolio. For the year, that 1.8%

From 2010 to 2020, inflation as measured by the Consumer Price Index averaged around 2 percent, a relatively low level by historical standards. From 2010-2019, the average interest rate on a one-year certificate of deposit was about.5%, It wasn’t that long ago that inflation was almost non-existent in the economy.

The catalyst for this post was a Tweet from Adam Butler who talked about a backdrop in the 2010's the promoted speculation and what he called Minskyian Moral Hazard (a nod to Hyman Minsky). Some allocation to equities is always going to be part of the portfolio. The tech sector ETF I use is an index fund but is used actively.

to be exact) over the last two years, after adjusting for inflationfaster than the 2010-2019 pace of 2.4%. A diversified portfolio does not assure a profit or protect against loss in a declining market. But The Economy Has Slowed Down The US economy grew at an annualized pace of almost 3% (2.9%

There are about 13 different portfolio managers each focused on a different sub-sector. And to the credit of the portfolio manager that I was working with Josh Fisher, we were actually up that year. So in 2010, when they were looking for someone to start their healthcare team in San Francisco, I, I jumped at the opportunity, right?

Arnott’s method focused on funds the increased the most in asset size from 2010 to 2021, recognizing that the funds that were historically the most successful would get higher inflows; i.e., “the big generally get bigger.”. Quick Links Warren Buffett Portfolio High Momentum Stocks Low Volatility / Conservative Stocks.

What I'm talking about specifically is that if you owned a portfolio of the 10 largest stocks and did a rebalance every January, you absolutely annihilated the S&P 500. I suppose that's always the case to a certain extent, but this time has to be close to a record. I can't imagine this is always the case.

The value investing strategy—acquiring shares of companies that are trading below their fair market value—had fallen out of favor in the 2010-2020 decade as high growth businesses dominated the market. But value is now outperforming growth with a 10% CAGR (compound annual growth rate), according to an article in Financial Express.

The Permanent Portfolio-inspired Cambria Trinity ETF (TRTY) allocates 35% to trend. Saying TRTY is Permanent Portfolio-inspired is my impression, I don't know that Meb has ever described it that way. We've gone over the extent to which the 2010's were by and large terrible for managed futures. Meb is a huge believer in trend.

after adjusting for inflation, matching the average annual pace between 2010 and 2019. A diversified portfolio does not assure a profit or protect against loss in a declining market. Through June 2023, the economy grew 2.4% Since then, the economy has accelerated. The Atlanta Fed GDP Nowcast is projecting 5.4%

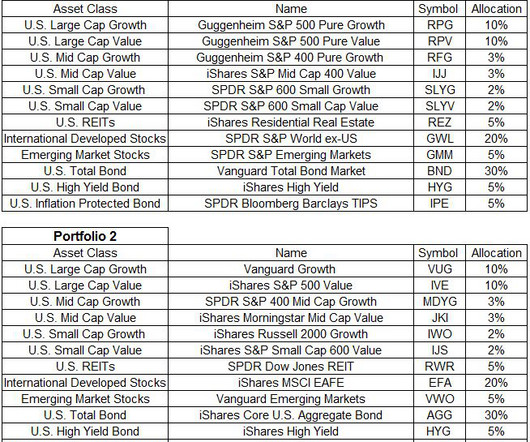

Below are two nearly identical portfolios; both are sixty percent stocks and forty percent bonds. Each portfolio has twelve slices, with identical allocations in each sleeve. For example, portfolio 1 has a 10% position to U.S. Portfolio 2 also has a 10% position to U.S. Portfolio 2 sold after the 23.3%

The space languished for most of the 2010's. It is another example of leveraging down as I like to describe it, using a capital efficient fund to build a full portfolio in a smaller portion of the portfolio and instead of adding on top, leveraging up, we can build in a large cash buffer. This year is kind of an anomaly so far.

It was titled Should Investors Try To Hedge Tail Risk which I wrote in 2010. Here's what's going on under the hood of the Accelerate OneChoice Alternative ETF Portfolio for example. If you have any interest in sophisticated portfolio construction, bookmark and then get to work as best you can.

On this episode, Bloomberg Intelligence ETF analyst Eric Balchunas joins us to discuss how fees can significantly impact your portfolio. ~~~ About this week’s guest: Eric Balchunas is been an ETF Analyst for Bloomberg Intelligence. Over the long term, the difference between a few basis points can turn into real, big money.

We have seen strong, strong demand pretty consistently for building out alternatives, portfolios, particularly when it comes to opportunities with great financial sponsors on the private equity side, looking at these long-term secular trends, right? RITHOLTZ: Let’s talk a little bit about inflation. You mentioned 8.5 percent inflation rate.

She has a fascinating career, starting a PLS working away up as an analyst and eventually, head of outcome-based strategies for Morningstar, eventually rising from that position and portfolio manager to Chief Investment Officer. Let me give you some background on Morningstar Managed Portfolios. I saw how personal money is.

Years ago when I was trading, probably 2010 or 2011, I had some fun trading weekly options around earnings releases. Take a look at your portfolio. Our portfolios are not a blank slate, we build positions over time, which can influence how we feel about these positions individually and how we feel about the market as a whole.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content