This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

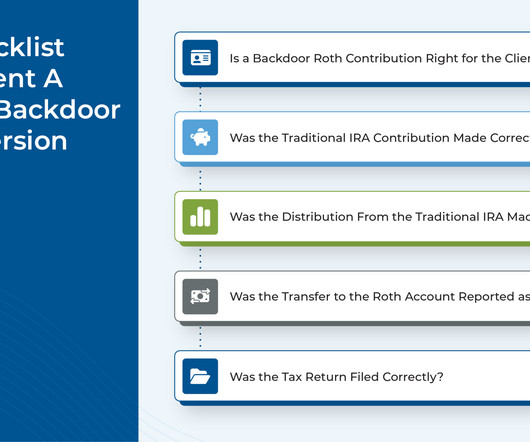

As while income phaseouts apply to contributions made to a Roth IRA, there are no such limitations on contributions made to a traditional IRA, nor on conversions from a traditional IRA to a Roth IRA (since 2010).

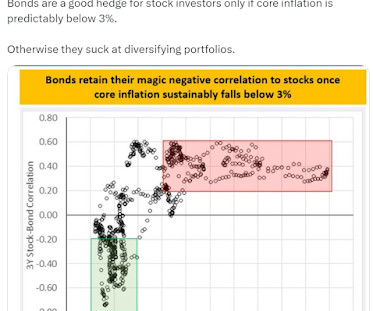

Every now and then we talk about expat living as part of a retirementplan, usually the context is an underfunded retirementplan. We've been saying for years, as the strategy was lagging throughout the 2010's, it was doing what it should, maintaining its negative correlation to equities.

For however long I've been a broken record on this, I've avoided trying predict anything since probably 2010, I learned a lesson at some point back then about how silly it is to try to predict interest rates. I found an interview I did with Seeking Alpha in late 2010 that made its way to NASDAQ.com. Here's the relevant excerpt.

Two primary goals of the IRA were to provide a tax-advantaged retirementplan to employees of businesses that were unable to provide a pension plan; in addition, to provide a vehicle for preserving tax-deferred status of qualified plan assets at employment termination (rollovers).

Picture retiring in 2010 versus 2020. The S&P 500 was down 22% for the 10 years ending 1/1/2010 while the ten years ending 1/1/2020 it was up 189%. One fascinating point looked at getting great market returns later in your accumulation period versus earlier. This is in the neighborhood of sequence of return.

If we're thinking about risk planning for the next ten years, I might wonder about a lost decade for US equities like we had from 2000-2010 and whether that might mean foreign equities rotate back into favor like they were back in 2000-2010. It's good to start thinking about these things ahead of time.

There's no way to know if repeating this same study running from 2015 to 2030 after a flurry of funds came out in the mid-2010's might get us closer but we can check back in five years.

If you've done research on managed futures then you've probably read what a rough decade the 2010's were for the strategy. Maybe it's as simple as equities went up a lot but either way from 2010 through 2019, RYMFX negatively compounded at 2.07% and AQMIX compounded annually at a positive 77 basis points.

It has been challenging as we've talked about in other posts recently but I believe the 2010's were even worse. Check out the following. To my knowledge, RYMFX was the first managed futures mutual fund and it had the space to itself for several years after in launched in 2007.

From 2010 to 2020, inflation as measured by the Consumer Price Index averaged around 2 percent, a relatively low level by historical standards. From 2010-2019, the average interest rate on a one-year certificate of deposit was about.5%, It wasn’t that long ago that inflation was almost non-existent in the economy.

The firm has been running the Alpha Simplex Managed Futures Strategy Fund (ASFYX) since 2010. The paper seems to support the very new Alpha Simplex Managed Futures ETF (ASMF) which started trading in mid-May.

For a few years in the 2010's, I had a side gig working for ETF provider AdvisorShares. One of my regular tasks was a quick, monthly call with each fund manager reviewing what happened and maybe getting some sort of forward look from them.

We've gone over the extent to which the 2010's were by and large terrible for managed futures. So maybe the 2010's were a coincidence. Managed futures did have a couple of fine years in the 2010's in the context of being a diversifier which is how we view the strategy here. Could such a terrible run repeat?

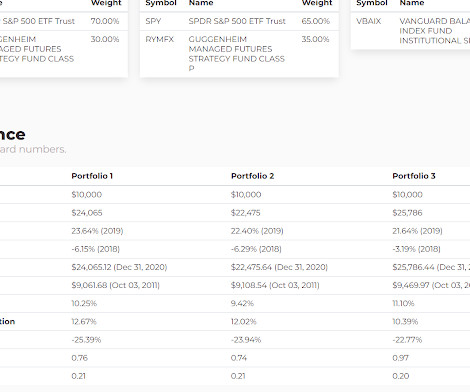

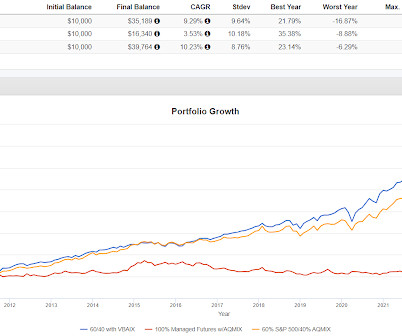

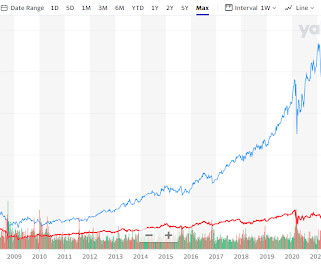

The 2010's was a rough decade for managed futures in nominal terms. I had enough previous experience with managed futures to understand the concept would work. Part of how they positioned the concept before the fund launched was a chart similar to this one. The S&P 500 was up 244% and managed futures went nowhere.

A Private Letter Ruling (PLR) from 2010 presents an interesting outcome from an indirect rollover – a rollover that was not done in a trustee-to-trustee transfer. Photo credit: jb.

As we bid adieu to this year, it’s a golden opportunity for savvy investors and retirement planners to give their strategies a once-over, particularly when it comes to Roth IRA conversions. Since 2010, everyone, regardless of income, can join in. Reach out to us today, and let’s make your retirementplanning shine.

The current funk is nowhere near as long as the languishment of the 2010's though. Looking at the history of a backtest is different than enduring a dry spell. Managed futures is a phenomenal diversifier but has been in a funk for awhile. Where we allocated 10% to second responders, only one of the models has all 10% in managed futures.

The catalyst for this post was a Tweet from Adam Butler who talked about a backdrop in the 2010's the promoted speculation and what he called Minskyian Moral Hazard (a nod to Hyman Minsky). Of course, there's an argument that index funds aren't really passive because of how the indexes are constructed.

I am absolutely a believer in the strategy even though it generally did poorly for most of the 2010's. We've written a lot about managed futures during this bear market as well as during the financial crisis. It worked during that stretch though for maintaining its negative to low correlation to equities as equities rocketed higher.

The space languished for most of the 2010's. I write all the time about managed futures as a diversifier and being able to live with the reality that managed futures will probably struggle when stocks are going up. This year is kind of an anomaly so far. Stocks are up and so are a lot of the managed futures funds.

The group struggled for many years in the 2010's and we saw a nasty whipsaw a year ago. T-bills instead would be less volatile with a lower yield. Managed futures can be a very challenging hold as we've talked about countless times.

Read the article but substitute ETF anytime it uses the word alternatives or any synonyms because this article read like one of the countless late to the part articles about ETFs from 2007 to maybe 2010.

I've been part of the planning committee for this drill since 2010, maybe 2009 and a participant since 2003. For a volunteer department like ours, there will be some years where the drill is our only live fire hours so it is very important.

It was titled Should Investors Try To Hedge Tail Risk which I wrote in 2010. In doing some research for another post, I found an old blog I wrote ages ago that touches on the same area. It makes for interesting reading because how many fewer ways there were to protect against extreme market events back then.

PTY is a couple of bucks lower than where it was 20 years ago and NLY is trading at about 1/4 of where it was in 2010. His thought with these very high yields is not to spend more than 4% (give or take) but to instead take what he calls extra income they pay to buy more shares because both of these go down in price.

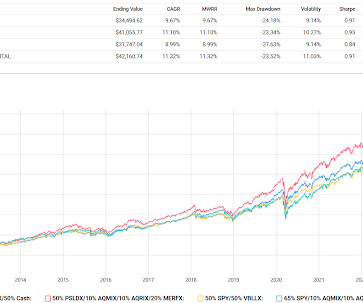

This is probably attributable to trend having some weak years in the 2010's. I find this to be interesting but anyone needing normal stock market growth in order for their retirementplan to work, probably isn't going to get it from any of these portfolios. Both 2 and 3 were up in 2022 while the RPAR replication was down 11%.

Managed futures has generally struggled lately just kind of grinding around which as I said almost all the way through the 2010's is what you might expect a strategy that is usually negatively correlated to equities to do. It's not that capital efficiency can't work but somehow, anytime I look, these particular funds are underwhelming.

I've referred to the 2010's as a dark winter for managed futures. That seems like a reasonable outcome, you don't want you diversifier to be your best performer. It's a little different now that the cash held to collateralize the futures contracts is now earning 5%. It was a long slow event that weighed on returns.

I said the same thing in various places I-don't-know-how-many-times during the 2010's. We have two years in a row now where equities were up a lot and managed futures languished which is exactly what should be expected. The more time goes on, the worse the 20%-to-managed-futures calls look.

Yeah, that lot that talks about terms like compounding, risk profile, returns, retirementplanning, budgeting, Investing, and whatnot! He is associated with ICICI Prudential Asset Management Company Limited since June 2010. of Stocks Held 68 This is a retirement solution-oriented mutual fund scheme from HDFC Mutual Fund.

I've been part of the planning group for this event since 2010. I've talked about this before that the inter-agency cooperation in the Prescott area was very unique but I believe other areas are now doing similar things.

Below are five benefits of working with a financial advisor and how they can help you retire with more wealth: 1. Consider a hypothetical scenario where you initially allocated 60% of your portfolio to equities and 40% to fixed-income assets in January 2010.

It has to be such a different set, the retirementplanning is different, the safety net is different. I mean, when I was in Chicago, one of my best experiences in Chicago was when Spain won the World Cup in 2010. So a phenomenal learning experience with both Jefferies and Morgan Stanley. RITHOLTZ: So you move here from Spain.

in Financial and Retirement Income Planning from The American College of Financial Services, where he was named the Sievert-Sternberg Doctoral Research Fellow, and is currently pursuing a Doctor of Criminal Justice degree from Northcentral University. 2010, August 1). Lee holds a Ph.D. Sources Consumer Federation of America.

I gave that up in something like 2010. The front of the curve is ok and of course there are segments of the equity market that take interest rate risk but that kind of volatility from equities is fine, I don't want it from income sectors. We've written countless posts on this for many years. Isolating the risk was easy.

From 1990 to 2010, the divorce rate for people over 50 doubled. A spouse with fewer marketable skills and less capacity to earn might want to argue for a greater share of the retirement assets, which they can use to shore up their own retirementplan. In divorce, you need to create two separate retirementplans.

When I retired in 2010, I had about $360K in a deferred IRA and $60K in a Roth IRA. I have taken RMD's since 2010 when I turned 70 and now I have over $550K in my deferred IRA and about $450K in my Roth without investing a dime. I will only spend my dividends… my pirates bounty of stocks and cash stay in the accounts earning $$.

Then you have to go back to year end June 2010 to find another year that VBAIX outperformed. Looking at a few other years, the year ending June 2021 Yale up 40% versus 20% for VBAIX. Year ending June 30, 2020 had Yale up 6.8% with VBAIX up 5%. In 2019 VBAIX outperformed by 221 basis points.

I bought it for clients in 2010 or 2011 and still hold it, so maybe. ARBFX 3.7% JRS 3.9% (short position) MERFX 3.7% TBT 24.7% (thought of as a short/hedge position) TDF 3.1% VXX 7.4% (thought of as a short/hedge position) VXZ 7.5% (thought of as a short/hedge position) XLE 3.9% There's a lot there, really lot.

Even when retirement is many years away, owners often view their business as a legacy they can pass on to the next generations of their family. In 2010, a study from the Conway Center for Family Business found that the lifespan of a family business was just 24 years.

But as I've been saying (occasionally) since maybe 2010, managed futures tend to have a negative correlation to equities. We've looked at the struggles of managed futures since then, many times. Yes, it has been a challenging hold since the 2022 glory.

That is refutable though because interest rates went down steadily for many years in the 2010's but the strategy did poorly. I think it's much simpler to think of managed futures as a "second responder" to a crisis or deep decline. The line between diversifier and core holding is probably debatable.

workers participate in an employer-sponsored retirementplan. ( Since 2010, IBM and General Electric have spent $95 and $72 billion respectively on share buybacks. Just 27% of the middle class owns at least $10,000 in equities, compared with 94% of the wealthiest households. ( Ben Carlson ) Only 45% of U.S.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content