This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

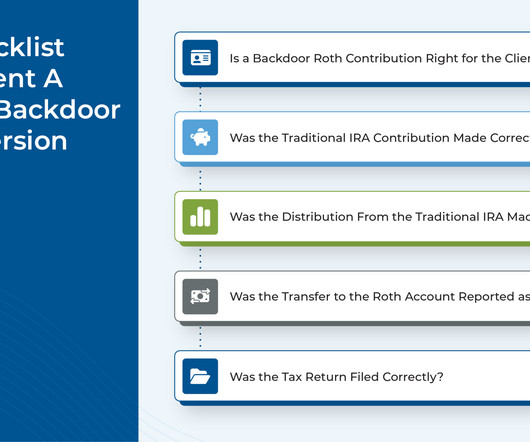

There are many taxplanning strategies that allow financial advisors to demonstrate the ongoing value they provide to clients in exchange for the fees they charge. Part of this value is understanding the detailed nuances that make a strategy effective and implementing it correctly, avoiding issues with the IRS down the line.

Navigating the complex world of personal finance, especially with retirement looming on the horizon, can be daunting. Working with a financial advisor can significantly enhance your chances of retiring with more wealth. Hiring the best financial advisors for retirement can lead to better savings and investment outcomes.

A little bit of effort and forward thinking during our summer and fall months will lead to a much more palatable and, potentially, financially advantageous tax season the following year. The reason for this is quite simple – taxplanning requires actual planning. One of the reasons to consider could be taxes.

SEIDES: But market returns across — RITHOLTZ: The past decade, 2010 to 2020, we were what? So I think that argument is very valid in those couple of years, 2009, 2010 probably, maybe 2011, which was a tough year for hedge funds. It’s part of their own taxplanning. RITHOLTZ: Oh no, it’s much worse.

The Long Game: Roth Conversions & Legacy Planning ajackson Thu, 08/01/2019 - 14:51 Legacy planning is all about transferring wealth to descendants as efficiently as possible. Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways.

Legacy planning is all about transferring wealth to descendants as efficiently as possible. So it may be surprising to hear that a Roth IRA—a vehicle ostensibly intended for retirement income—can be a powerful mechanism for next-generation wealth transfer. Background.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content