This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Fair Value : Valuation of equities is one of those things that seems to confuse so many. Earnings are a fact, analysts’ earnings estimates are an opinion. If a company’s earnings are above or below consensus, it was the analysts who got it wrong and not vice versa.

He launched the Churchill Financial Group in 2006, which was purchased by PE giant The Carlyle Group in 2011. Known as the Dean of Valuation, he teaches Corporate Finance and Valuation to the MBA students at Stern where he has been voted “Professor of the Year” by the graduating M.B.A. class nine times.

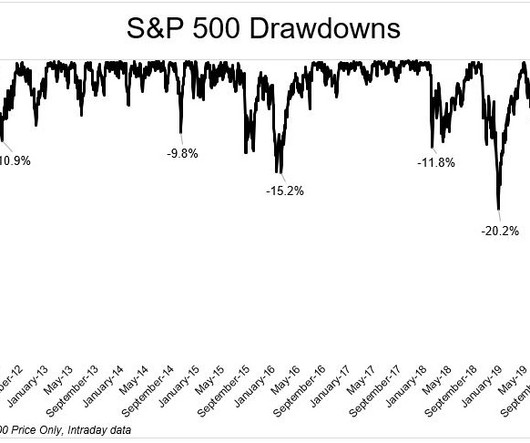

With the S&P 500 now close to 20% off its highs, I thought now might be a good time to look to our market valuation tool to see where things stand. But before I do that, I wanted to first cover two caveats I always put in articles about market valuation. With that all being said, let’s look at the current valuation data.

While some of that outperformance was due to improving fundamentals and earnings, most of it the returns came from the valuation investors assigned to these stocks. The chart below shows that of the tech sector’s 760% total return, 620% came from the change (increase) in valuation while 140% came from increasing earnings and dividends.

A companys price-to-earnings (P/E) ratio must be in line with or lower than its earnings growth rate to ensure valuation remains attractive. This strategy had big winning years like 2013 (+65.9%) , 2020 (+106.5%) , and 2021 (+51.7%) but also suffered steep declines, including 2008 (-27.0%) , 2011 (-16.7%) , 2015 (-9.6%) , and 2022 (-30.3%).

But some time around 2011/12 I got tired of living in fear and realized that very few people make money being pessimistic in the long-run. All that scaremongering about the national debt, QE, valuations, Capitalism, etc. The generally optimistic Cullen you might know by now did not exist.

With the benefit of hindsight, and some valuation expansion, it appears it was buried alive. On a monthly closing basis, it hasn't been more than 5% away from its all-time high since 2011. We've heard about the death of the traditional 60/40 portfolio for a few years now. 1 has compounded at 10.8% a year, for a 152% total return.

Gold was mostly in a downtrend from mid-2011 to early 2016. It doesn't look like we're going to get to an extreme panic level for the S&P 500 on this event but as an example, with equities down 40%, you don't need as much protection from gold as when the stock market is at all time highs combined with sky high valuations.

Two weeks ago, I wrote an article where I looked at the valuation of the median stock and how it has changed over time. 12/30/2011 1.5% 12/30/2011 23.8% By Jack Forehand, CFA, CFP® ( @practicalquant ) —. Year End Date Negative Earner Percentage 12/30/2005 1.1% 12/29/2006 1.2% 12/31/2007 1.0% 12/31/2008 2.1% 12/31/2009 4.9%

Sentiment cycles move from one extreme of greed to another extreme of fear which takes valuations also to extremes from their long-term averages. At the extreme of fear sentiment (which coincides with dirt-cheap valuations), the risk-reward is highly favorable i.e., higher potential upside with lower potential downside risk.

In 2011, a Tel Aviv-based startup called Cyvera began developing cybersecurity software deploying the coding equivalents of barriers and traps to thwart hackers staging potentially devastating “zero-day attacks.” Less than two years later, Palo Alto Networks purchased the company for $200 million—a more than 25-fold surge in valuation.

Since 2011, the S&P 500 has gained nearly 300%. We know that the combination of high valuations and investor euphoria always ends badly. The past decade has been one of endless prosperity. At least in risk assets. The return on certain individual securities makes the overall stock market look like a savings account.

With valuations still high, the threat of a recession still looms over the economy, ushering in a prolonged period of low returns across the market, from stocks and real estate to corporate profits, as well as elevated inflation and unemployment rates.

billion in assets they held in 2011. While the factors above have buoyed dividend-rich stocks this year, such stocks now pose a rising risk in portfolios for several reasons: Their valuations have stretched beyond what is justified by the fundamentals in many cases. billion, nearly double the $367.3 stock market (chart 1). Conclusion.

billion in assets they held in 2011. While the factors above have buoyed dividend-rich stocks this year, such stocks now pose a rising risk in portfolios for several reasons: Their valuations have stretched beyond what is justified by the fundamentals in many cases. Stretched Valuations. billion, nearly double the $367.3

Existing home sales are on track to record their slowest year since 2011. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors. Housing starts rebounded 7.0% month-over-month.

2010 - Have Cash, Wait for Stocks to Fall 2011 - Grantham sees most global equities as ranging from “unattractive” to “very unattractive” – valuing the S&P 500 at “no more than 950.” Investor enthusiasm, coupled with high valuations, has preceded all major market bubbles. It's been over four years since he wrote this.

LEDs In the LED sector, Servotech commenced production in 2011, crafting energy-efficient luminaries for residential, industrial, and commercial use. The extent of this growth and its impact on the company’s valuation remains a topic for discussion and speculation. Share your thoughts in the comments below!

stocks and Emerging Markets stocks: 2008 and 2011. Large caps beat the foreign stock categories yet still lost thirty-seven percent of their value, while 2011 was the only year where U.S. Oh, I forgot to mention it finished dead last in 2008 and 2011. Large Caps outperformed both Developed ex-U.S. Sounds unstoppable, right?

Quotes: Matt Cooper on the decision to take on private equity: “We entered into our inorganic growth stage in roughly 2011. The factors that determine whether or not an acquisition is satisfactory and successful for all parties. And we actually did it in a separate RIA within Beacon Point.

Bull markets are in the eye of the beholder, and when we mark the beginning is of little importance, unlike things like earnings and valuation and interest rates. From April through October 2011, the S&P 500 fell 21.6% The Netflix of fitness has a $4 billion valuation.

From 2011-12 onwards, IRFC has forayed into funding railway projects and capacity enhancement works. Hence, Investors must look for the perfect balance of high ROE, and low GNPAs at lower valuations (P/E). The NBFCs will then be required to keep aside hefty profits to write off these Non-Performing Assets.

Or tech valuations. So the 19% decline in 2011 isn't captured in my data. **Two of the 20% declines were 19 and change. Ben Carlson said: When the markets go haywire, you really have 3 options on what to do with your portfolio: Do more Do less Do nothing Callie Cox put it plainly. Or the Fed. Or the economy. Or commodities.

We bought ARM Holdings in July 2011 and held on even as oversupply slowed growth in smartphones sales. We look for fundamental strengths, attractive valuations and what we call Sustainable Business Advantage (SBA). They then construct their portfolios by using traditional measures for valuation and performance.

We bought ARM Holdings in July 2011 and held on even as oversupply slowed growth in smartphones sales. We look for fundamental strengths, attractive valuations and what we call Sustainable Business Advantage (SBA). They then construct their portfolios by using traditional measures for valuation and performance.

However, since 2008, the stock market has generally been on a consistent tear racking up a record of 10 wins, 2 losses (2015 and 2018), and one tie (2011). PRICES: Valuations have come down significantly – Price/Earnings ratio of 15.9 (i.e., For 2022, the S&P 500 index is down -21%, including -8% last month. Source: TradingView.

The strong price appreciation has resulted in a commensurate rise in valuations and a tsunami of new deal issuance in these areas. Exhibit 5: Dispersion in stock returns for the Russell 2000 ® Index, three-year trailing return for top and bottom quartile, by year since 2011, and average and median 1991–2020 Source: Furey Research Partners.

The strong price appreciation has resulted in a commensurate rise in valuations and a tsunami of new deal issuance in these areas. Exhibit 5: Dispersion in stock returns for the Russell 2000 ® Index, three-year trailing return for top and bottom quartile, by year since 2011, and average and median 1991–2020. Source: FactSet.

According to quarterly Federal Reserve data, money market assets were more than $6 trillion at the end of the third quarter of 2023, roughly double what they averaged from 2011 to 2017. Many investors’ fixed-income holdings still heavily favor short or ultra-short maturity bonds or cash-like vehicles.

As shown in Figure 2 , the 90% level has historically signaled the start of new bull markets coming off of major lows such as 2009, 2011, 2018-2019, and 2020. It is also a major component used to calculate the price-to-earnings valuation ratio. This indicator reached 87% on August 11, very close to that 90% trigger.

Last week’s riddle: About 90% of this country’s land area is made up of arid tan desert, yet its flag was once solid green (until 2011) – in fact, at one time it was the only nation in the world with a flag containing just one color. For that matter, a snakehead isn’t a snake – but what is it? What nation is this? Answer: Libya.

Because of the ever higher Fed rate hike expectations, the yield on the 10-year Treasury security has increased by nearly 200 bp this year after increasing around 100 bp in 2020 and is at the highest level since 2011 [Figure 1]. It is also a major component used to calculate the price-to-earnings valuation ratio.

In 2011, an Italian company under the name Fabbrica Italiana Lapis ed Affini (FILA) entered into a strategic partnership with RR Group. Now would this be enough to convince you to invest in a dull industry at a sky-high valuation of 43x? As of 2015, FILA raised its stake in DOMS to 51%, investing Rs. Let us know in the comments below.

And when they look at a sector, they want to be long, the very best stocks at the best valuations they can, and short the worst stocks at the worst valuations. So your next stop is Citadel in 2011, and you spend six years there, Citadel also, like Millennium has a fantastic reputation. 00:08:21 [Speaker Changed] Wow.

After a tough decade for simple systematic value strategies from 2011-2021 this model bounced back very well in 2022. Throughout 2022 the most expensive stocks were the ones hit hardest as valuations started to normalize in a new world of higher interest rates. The model portfolio was up 17.2% in 2022 vs. a 19.4%

Recharacterization: But what if you converted a traditional IRA to a Roth at a time when the assets were at peak valuation, and the value of the assets have since declined? Given the volatility in capital markets in recent years, you may find yourself in this situation.

Well, we believe that broader economic fundamentals are important for long-term stock valuations. The table at right summarizes the results of a 2011 study by Robert Kosowski, who found that managers indeed tended to struggle during economic expansions but produced meaningful value during recessionary periods.

Well, we believe that broader economic fundamentals are important for long-term stock valuations. The table at right summarizes the results of a 2011 study by Robert Kosowski, who found that managers indeed tended to struggle during economic expansions but produced meaningful value during recessionary periods.

But in the Mustachian Era (the years since 2011 when I started writing this blog ), there has only been one: the 2020 Covid Crash which only lasted about a month. A 20% drop in stock prices is called a “bear market” and they traditionally happen every few years, lasting just 9 months or so from top to bottom. ” Well, how interesting.

Asked about using valuation tools, like aggregate market cap to GDP or cyclically adjusted P/E ratios to gauge markets, Buffett explained that neither of these is paramount. Berkshire has an advantage when that happens. Markets are there to be taken advantage of rather than followed. Buffett said he views Apple and IBM differently.

Asked about using valuation tools, like aggregate market cap to GDP or cyclically adjusted P/E ratios to gauge markets, Buffett explained that neither of these is paramount. Berkshire has an advantage when that happens. Markets are there to be taken advantage of rather than followed. Buffett said he views Apple and IBM differently.

The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. The second, and what’s interesting about that period, is the fact that valuations actually peaked in 1961. MIAN: Valuations are ebb and flow. Because when you think about debt ceiling, you think about 2011.

2011 : “[T]he expected return/risk profile of the stock market has shifted to hard-negative.” 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.” 2020 : “[E]xtreme valuations. Not surprisingly, outflows began in earnest in 2011.

Investor concerns about slowing growth have sprung up here and there since 2011 but had yet to set back equities until this year. from 2016 until 2020, a step down from the annual target of about 7% from 2011 until the end of this year. 14, 2011, the UBS/Bloomberg CMCI rose 9.7% From April 7, 2011, until Sept.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content