This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

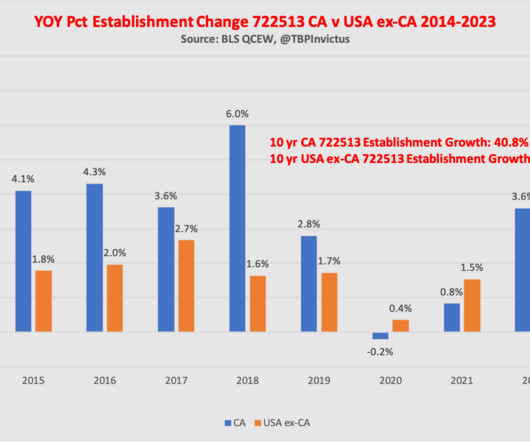

Here is NAICS code 722513 for California and Texas, indexed to 100 as of January 2013. The correlation between January 2013 and pre-Covid peak of March 2020 is 0.994. As mentioned above, for seven years – from January 2013 to March 2020 – CA and TX QSR employment moved almost identically, the correlation between them 0.994.

Here is NAICS code 722513 for California and Texas, indexed to 100 as of January 2013. The correlation between January 2013 and pre-Covid peak of March 2020 is 0.994. As mentioned above, for seven years – from January 2013 to March 2020 – CA and TX QSR employment moved almost identically, the correlation between them 0.994.

Camerer won the MacArthur Fellow (Genius award) in 2013. He is a member of the American Academy of Arts and Sciences and holds fellowship at the Econometric Society and the Society for the Advancement of Economic Theory. On today’s episode, we breakdown the behaviors that drive our financial decision making.

Bloomberg , October 9, 2015 Art Cashin’s Tis the day before New Year’s (December 31, 2014) Art Cashin Just Gave A Hilarious Wall Street History Lesson Going Back To The 1950s by Linette Lopez Business Inside, Oct 8, 2013 TBP 2013: Fireside Chat with Trading Legend Art Cashin (October 3, 2013) Art Cashin: Black Monday, An Unforgettable Single Day (October (..)

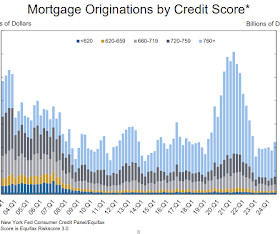

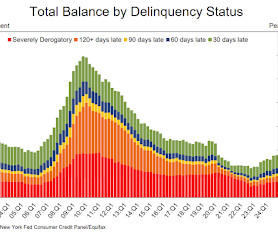

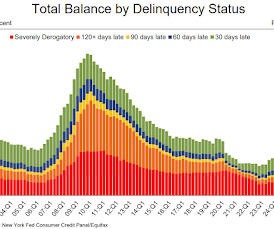

Household debt previously peaked in 2008 and bottomed in Q3 2013. About 126,000 consumers had a bankruptcy notation added to their credit reports this quarter, a small decline from the previous quarter. emphasis added Click on graph for larger image. Here are three graphs from the report : The first graph shows household debt increased in Q3.

The average annual property insurance premium among mortgaged single-family homes rose by a record $276 (+14%) to $2,290 in 2024 Thats the largest single-year increase on record dating back to 2013 when ICE began tracking the metric, and when stacked on top of the $245 (14%) increase seen in 2023 caps off a 61% ($872) increase over the past 5 years (..)

Professor Camerer was became a MacArthur Fellow (Genius grant) in 2013 for his work on risk, self-control, and strategic choice. Be sure to check out our Masters in Business next week with Colin Camerer , the pioneering neuroeconomist at California Institute of Technology.

Okay, it’s up 10,000% since May of 2013 and is now the best performing stock in America during the past decade. Everyone is obsessed. It’s the biggest story in the market this year. Cramer has now named a second family dog after it.

I have no idea whether its a long-term staple or a flash in the pan, but it feels to me like I am now at peak Substack… Previously : Things I Don’t Care About (January 15th, 2013) What Do You Control? (May May 30th, 2013) Asking the Right Questions (July 18th, 2013) The Price of Paying Attention (November 2012) Who Do You Trust?

Coming into 2025 the S&P 500 had just two down years out of the past 15: 2010 +14.8% 2024 +24.9% We were all probably a little spoiled. Regardless of the reason for the recent swoon, we were due.

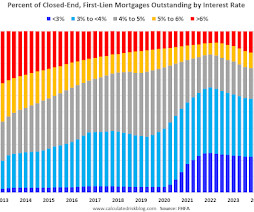

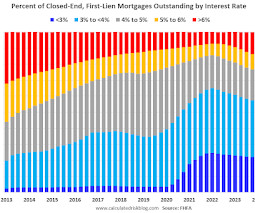

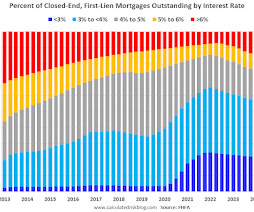

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q4 2023 (Q1 2024 data will be released in three weeks).

The best examples are 1946-66, 1982-2000, and 2013 forward. for this to be the case two things must have happened: 1) The secular bull market that began in 2013 has ended, and 2) We are now in a new secular bear market. We call these eras Secular Bull Markets.

Household debt previously peaked in 2008 and bottomed in Q3 2013. Transition into serious delinquency, defined as 90 or more days past due, edged up for auto loans, credit cards, and HELOC balances but remained stable for mortgages. emphasis added Click on graph for larger image. rise from 2024Q3.

Here is some data showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q4 2023. This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic.

@TBPInvictus here Our story so far : California has been raising its minimum wage for the past decade, starting at $8/hour through 2013. Many fast food workers (specifically) got bumped to $20/hour, from $16, in April (the law is very specific about who is eligible for the increase).

Here is some data showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q2 2024. This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic.

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q1 2024 (Q2 2024 data will be released in two weeks).

million units in the first six months of 2023, the fewest for the first six months of a year since 2013. The second graph shows the six-week average (not monthly) of U.S. intermodal in 2021, 2022 and 2023: (using intermodal or shipping containers): U.S. intermodal was down 10.3% Volume was 6.11

Consider these columns going back to 2013 pointing out the foolishness of tax-payer subsidized corporate welfare queens (2013), and why median wages were rising ( 2016 , 2017 , 2018 , 2018 , 2019 ). Then came the pandemic, and a huge federal worker subsidy.

February 17, 2015) Click for video [link] Source: Economics Media Library The post The Daily Show: Wage Against the Machine appeared first on The Big Picture.

On the discouraging side, January 2023 was the worst January for intermodal since 2013 , with originations down 8.1% Intermodal volume averaged 229,982 units per week in January 2023, the fewest for January since 2013. January 2022 was the worst January for total carloads in our records that begin in 1988. from last year. railroads.

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

percent is now at its highest level since fourth quarter 2013, driven by office portfolios at the largest banks. The quarterly increase was led by commercial and industrial loans and non-owner-occupied CRE loans. The noncurrent rate for non-owner occupied CRE loans of 1.59 emphasis added Click on graph for larger image.

June 3rd, 2011) THE MOST IMPORTANT EVER NFP blah blah blah (June 7th, 2013) “What’s Your NFP Number?” workers in the economy that excludes proprietors, private household employees, unpaid volunteers, farm employees, and the unincorporated self-employed.

Wages in America (2013-2021). Wealth Distribution in America (April 11, 2019). Composition of Wealth Differs: Middle Class to the Top 1% (June 5, 2019). No, Your iPhone Does Not Make You Wealthy (June 4, 2018). Source : Moving between wealth brackets: Minimum cutoffs from the Distributional Financial Accounts.

Way back in 2013, I wrote a post " Predicting the Next Recession. That was written in 2013, and it appears once again that we've avoided the "default" policy error. 1) Most of the post-WWII recessions were caused by the Fed tightening monetary policy to slow inflation.

Way back in 2013, I wrote a post " Predicting the Next Recession. I disagreed and noted I wasn't even on recession watch! Now it seems like most forecasts are for a recession in 2023. My answer is: Maybe. This post was in response to several recession forecasts (that were also incorrect).

Previously : America’s Corporate Welfare Queens (November 13, 2013) Minimum Wage Increases Do Not Destroy Jobs (January 24, 2019) Generational Reset of Minimum Wage (November 30, 2021) Wages in America The post Americonned appeared first on The Big Picture. And the personal stories are compelling.

Here is some data showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023. This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic.

Here is a graph of the participation rate by age cohort for November (1983, 1993, 2003, 2013 and 2023 NSA). Second, the reason we use the 25 to 54 group is that the participation rate is fairly steady across the entire age spectrum.

Previously, he was head of the European Special Situations Group from 2008-13, and head of the Global Special Situations Group: 2013-19. He is also a member of the management committee, and Co-Chairs the Asset Management Investment Committees, which includes private equity, infrastructure, growth equity, credit, and real estate.

Way back in 2013, I wrote a post " Predicting the Next Recession. And other measures of the economy were also positive, especially employment. So, it is extremely unlikely there was a recession. This post was in response to several recession forecasts (that were also incorrect).

The Pandemic crash and rally was a 34% reset and a continuation of the bull that formally began in March 2013. February 4, 2013) Looking at the Very Very Long Term (November 6, 2003) Bull & Bear Markets The post Where is This Rally Going? Secular Bull Market : US stocks are in the 5-6th inning of a bull market.

Household debt previously peaked in 2008 and bottomed in Q3 2013. Aggregate limits on credit card accounts increased by $100 billion and now stand at $4.22 trillion–the largest increase in more than ten years. emphasis added Click on graph for larger image. rise from 2022Q1.

Note the issue with OER is not a new phenomenon, and the research note 1 above was from 2013. Mike Bryan and Nick Parker, March 11, 2013). I thought that was important enough when I saw it in 2013 to have mirrored it at The Big Picture. -Mike Bryan and Nick Parker, MacroBlog , Atlanta Federal Reserve. Think Again.

Here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q4 2022.

Here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q1 2023 (Q2 2023 data will be released in a few weeks).

million) from 2021, and the lowest annual volume since 2013. For all of 2023, U.S. intermodal originations totaled 12.67 million containers and trailers — down 4.9% (657,165 units) from 2022 , down 9.6% (1.35 In 2023, containers were 94.9% intermodal units, a record high. emphasis added Click on graph for larger image.

Here is some data from the recently released FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q1 2023. Currently 23.3% of loans are under 3%, 61.3% are under 4%, and 81.2% are under 5%.

(December 5, 2022) The Super Wealthy versus the Merely Rich (February 7, 2022) Wealth Distribution in America (April 11, 2019) Composition of Wealth Differs: Middle Class to the Top 1% (June 5, 2019) Wages in America (2013-2021) The post Wealth Inequality Starts at the Top appeared first on The Big Picture.

After the launch of RWM in 2013, we tried different formats: The Evidence-Based Investment conference tried to pull some of the irrationality out of typical conferences; Wealth | Stack looked at the intersection of technology and wealth management. It didn’t have to be expensive or exclusive, so long as it was informative and useful.

Household debt previously peaked in 2008 and bottomed in Q3 2013. Delinquency transition rates for credit cards, auto loans, and mortgages increased slightly. emphasis added Click on graph for larger image. Here are three graphs from the report : The first graph shows household debt increased in Q2. rise from 2024Q1.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content