This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

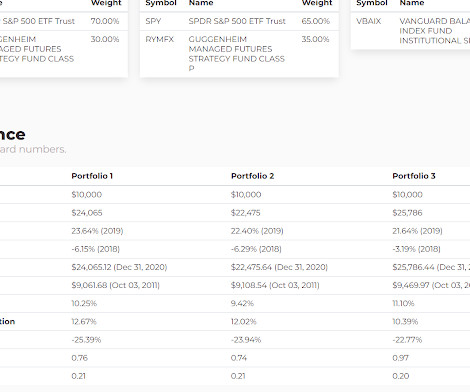

It backtests to 2014. I've been critical of the actual FIG ETF, the Simplify Macro ETF, it is really struggling but I think the fund's idea for assetallocation works for the most part. Again, those percentages are how I believe FIG has allocated its assets, using different holdings of course.

There's no fact sheet yet and while the holdings are available, the assetallocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly). Plenty of other managed futures funds came onto the scene in 2013 and 2014 but I think RYMFX is the only one to test what was a terrible time for managed futures.

according to Siegel (2014). And the only way that disaster happens is if your financial planner is making irrational projections about asset returns and your assetallocation. The worst narrative in finance is this idea that stocks generate 10%+. The reality is that stocks have averaged about 4.4%

It offers various services across various asset classes, including equity, fixed-income, and derivative securities. The exchange operates an “anywhere, any asset” trading platform. It was named Indian Exchange of the Year for 2014 by Futures & Options World. However, financial assetallocation increased recently.

We continue to stay under-allocated to equity (check the 3rd page for assetallocation) at the current valuation levels. Other Asset Classes : After a strong rally, Gold cooled off in Q1FY24 on the back of profit booking and shifting focus towards equity. We continue to prefer a portfolio duration of around 1-1.5

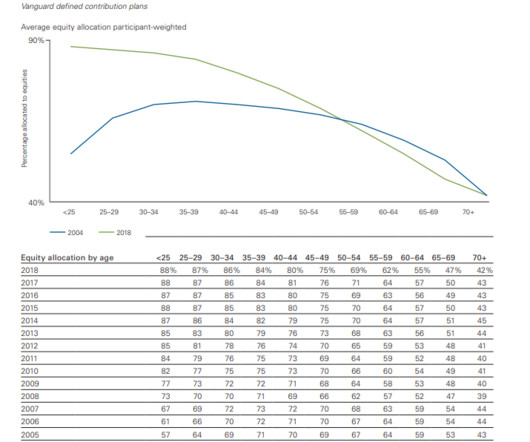

trillion in assets. They anticipate that by 2023 80% of all assets at Vanguard will be in an automatic investment program. There has been a pretty steep drop-off in participation for people under 25 years old, from 57% in 2014 to 38% in 2017. Vanguard is out with a new monster research report called How America Saves.

The Global X S&P 500 Covered Call ETF (XYLD) has been around since 2014 and while it has lagged the plain vanilla S&P 500 badly, its annualized total return is still 5.78%. They build out a few different types with various allocation percentages for each type.

In my multiple conversations with investors during the bull-run since 2014, there was no one who said that I will not take advantage of investing in equity when the market will crash. Not knowing how to value assets. 🔊 Play Audio. But interestingly, very few implement this strategy.

Within the $450 billion high-yield market, less than 60% of high-yield bonds sell for more than face value compared with more than 90% in June 2014. By Taylor Graff, CFA, AssetAllocation Analyst. The low volume indicates a reluctance among investors to roll over debt for stressed companies. Anchoring Expectations.

It's the assets you have to worry about. I first met Wes Gray, CEO/CIO of Alpha Architect in late 2014 and remember thinking, holy s**t, this guy rules. Investors were apparently seeking safer assets that morning, and the Bloomberg News service flashed this headline: U.S. He taught me that assetallocation matters.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. stocks growing more expensive.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. We maintain a model portfolio internally to track the results of our assetallocation stances. Thu, 06/01/2017 - 02:47.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. over the last 100 years (1915–2014), but interestingly, they increased to 7.9% Thus, it’s important to have a view on this key question. over the more recent 30-year period.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. over the last 100 years (1915–2014), but interestingly, they increased to 7.9% Thus, it’s important to have a view on this key question. over the more recent 30-year period.

We break down and assign each of the four “regions” with an asset class and then pick teams (stocks) that we think have the best chance at doing well relative to others. Betting on the right asset class or area of the world is usually going to bode better for you and also avoids having a collection of stocks that one has to follow.

And suddenly you could buy index funds that cover all of the major asset classes. And after I got my last urine bonus in early 2014, I walked in and handed, handed my notice. I was in my, I was 51, so I spent 10 or 11 months preparing to leave. I contacted the journal about writing for them again, I also started working on a book.

As you can see from the chart below, there have been no shortage of issues and events to worry about over the last 15 years (2007 – 2022): 2008-2009: Financial Crisis 2010: Flash Crash (electronic trading collapse) 2011: Debt Ceiling – Eurozone Collapse 2012: Greek Debt Crisis – Arab Spring (anti-government protests) 2012: Presidential Elections (..)

Alpha Architect on investing systems The sad conclusion is that few if these ideas stand up to intense robustness tests except for the simplest technical rules (much like assetallocation- simpler is often better). This is close to five times the spread between value and growth firms.

Public-sector debt has expanded every year since 2000, hitting 100% of gross national product at the end of fiscal year 2014. By Taylor Graff, CFA, AssetAllocation Analyst. Protecting inherited assets from a claim by a family member’s ex-spouse can help limit those losses. million from about 3.8 Dream or Opportunity?

in 2014, according to the International Monetary Fund (IMF). The ratio for the 19 countries in the eurozone rose to 93% at the end of the first quarter from 92% at the end of 2014, according to the European Union. By Taylor Graff, CFA, AssetAllocation Analyst. Eurozone growth will probably speed up to 1.5%

Click here if you need to catch up on a conflict that’s been in flux since February of 2014. We often talk about people having short memories but don’t think that the Ukraine and Russia conflict just started last week. The point of our “letter to Mr. Market” today, however, is on what to do with your investments.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. Some might argue that the Fed’s policy could trigger another crisis as asset prices become overly inflated.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Despite the U.S.

For the past year, we have been preparing client portfolios for the end of the extended bull market run that began in 2009—building cash and liquidity reserves, and also exploring opportunities in private and alternative asset classes that historically have offered lower correlation with public markets. Despite the U.S. Harsh Reaction.

Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e.,

Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e., Less Efficient Asset Classes.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) For example, one study revealed that beta is often confounded with alpha, and this can mistakenly attribute outperformance to the value-add of an active manager rather than market risk premia (Bender, 2014). Deutsche Asset & Wealth Management White Paper.

This work builds on the Capital Asset Pricing Model developed in the 1960s.) For example, one study revealed that beta is often confounded with alpha, and this can mistakenly attribute outperformance to the value-add of an active manager rather than market risk premia (Bender, 2014). Deutsche Asset & Wealth Management White Paper.

who became a professor at the University of Michigan before setting up his own asset management firm. 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.” percent in 2014; HSGFX declined 8.50 ” Which brings me to John Hussman. He is a Stanford Ph.D.

We maintain our underweight position to equity (check the 4th page for assetallocation) on the back of pricey markets. Other Asset Classes Gold cooled off further in Q2FY24 due to higher interest rates offered by US treasuries along with the expectation of falling interest rates. years with preferably floating rate instruments.

While this shift in monetary policy may ultimately have important implications for assetallocation and other investment decisions, we’re not convinced that its near-term impact will be particularly significant. By 2014, when QE officially ended, assets on the Fed’s balance sheet totaled $4.3

While this shift in monetary policy may ultimately have important implications for assetallocation and other investment decisions, we’re not convinced that its near-term impact will be particularly significant. By 2014, when QE officially ended, assets on the Fed’s balance sheet totaled $4.3 Uncertainty in Unwinding.

The transcript from this week’s, MiB: Ken Kencel, Churchill Asset Management , is below. BARRY RITHOLTZ, HOST, MASTERS IN BUSINESS: This week on the podcast, I have an extra special guest, Ken Kencel of Churchill Asset Management, CEO, Founder, President. This is really a fascinating story. Ken Kencel, welcome to Bloomberg.

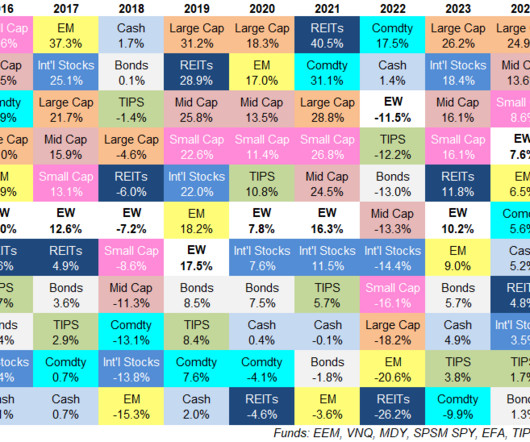

The first assetallocation quilt I created for this site covered the ten-year period from 2005-2014. Those returns look nothing like the last 10 years which is the whole point of this exercise. Treasury-inflation protected securities were up 2.1% annually over the sam.

Fisher, 1958 The Money Game - George Goodman, 1967 A Random Walk Down Wall Street - Burton Malkiel, 1973 Manias, Panics, and Crashes: A History of Financial Crises - Charles Kindleberger, 1978 The Alchemy of Finance - George Soros, 1987 Market Wizards - Jack Schwager, 1989 Liar's Poker - Michael Lewis, 1989 101 Years on Wall Street, An Investor's Almanac (..)

And that was his boss, Jeffrey Gundlock, founder of Double Line Capital, back in July, 2014. He really is one of the most knowledgeable people in this space, and not just knowledgeable in the abstract, but helping to oversee just about a hundred billion dollars in client assets. And so I worked a lot on the assetallocation side.

Assetallocation is more important than the selection of a portfolio’s component parts. All other things being equal, ETFs are better than mutual funds. Simple generally beats complex. Complex instruments, reaching for yield, and illiquidity are usually more dangerous than they appear.

Highly dependent on precise phrasing of questions That’s just about basic market, economic, and assetallocation questions. Operates on a substantial lag 4. Requires accurate self-reporting 5. ” In 2020, after a massive voter registration drive, the Census estimated that 168.3 million people were registered to vote.

DUTTA: And the thing is that it never got as low as it did in 2014 despite 7 percent mortgage rates, right? But a lot of the rally in the dollar, say, from 2014, to, you know, up until recently, I mean, a lot of that was just growth differentials, right? DUTTA: Right, exactly. So what does that tell you about underlying demand?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content