This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

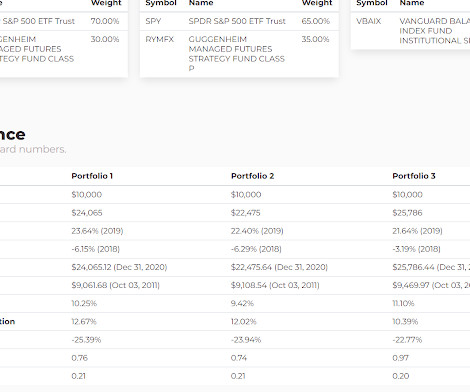

From the fund page : the goal is seeking stable returns across a variety of economic and financial market conditions, consistent with the preservation of capital. There's no fact sheet yet and while the holdings are available, the assetallocation is vague without calculating the spreadsheet yourself which I did (hopefully correctly).

All the sectors went up with major sectoral growth seen in auto (up 22%), realty (up 33%), and consumer durables (up 13%) on the back of an improving economic outlook. We continue to stay under-allocated to equity (check the 3rd page for assetallocation) at the current valuation levels.

Through conservative, bottom-up analysis, we are taking advantage of current market dynamics to buy attractively priced debt in companies with solid revenues and limited vulnerability to an economic downturn. Debt in well-managed companies positioned to weather an economic slump return nearly three times the 2.3%

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks. Thu, 06/01/2017 - 02:47.

As you can see from the chart below, there have been no shortage of issues and events to worry about over the last 15 years (2007 – 2022): 2008-2009: Financial Crisis 2010: Flash Crash (electronic trading collapse) 2011: Debt Ceiling – Eurozone Collapse 2012: Greek Debt Crisis – Arab Spring (anti-government protests) 2012: Presidential Elections (..)

In my multiple conversations with investors during the bull-run since 2014, there was no one who said that I will not take advantage of investing in equity when the market will crash. 🔊 Play Audio. In good times i.e. when the market valuations are usually very high, everyone agrees to the logic of buying low and selling high.

Alpha Architect on the myth that economic growth drives stock returns We're going to let you in on a little secret: Investors focused on economic growth are wasting their time.If may be that the best prices can be had in times of low economic growth, whereas we tend to overpay in a growing economy.

On the economic side there is no denying that the more financial predictions you make the more business you do and the more commissions you get. I first met Wes Gray, CEO/CIO of Alpha Architect in late 2014 and remember thinking, holy s**t, this guy rules. He taught me that assetallocation matters. Fred Schwed Jr.,

War and financial turmoil— the bane of Europe’s economic well-being last century—are currently veiling a rebound in regional growth and unanticipated vigor among European companies. in 2014, according to the International Monetary Fund (IMF). Economic recoveries usually feature a surge in consumption as employment and wages rebound.

million in 2006, inhibiting demand and economic growth, according to the Krueger report. Public-sector debt has expanded every year since 2000, hitting 100% of gross national product at the end of fiscal year 2014. Economic recoveries usually feature a surge in consumption as employment and wages rebound. million from about 3.8

And after I got my last urine bonus in early 2014, I walked in and handed, handed my notice. And I think it partly depends on the economic comfort in which you grew up. I was in my, I was 51, so I spent 10 or 11 months preparing to leave. I contacted the journal about writing for them again, I also started working on a book.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. over the last 100 years (1915–2014), but interestingly, they increased to 7.9% Thus, it’s important to have a view on this key question. over the more recent 30-year period.

Changes in their assumed rate of return can impact decisions ranging from assetallocation to the spending level that a portfolio can rationally support. over the last 100 years (1915–2014), but interestingly, they increased to 7.9% Thus, it’s important to have a view on this key question. over the more recent 30-year period.

Click here if you need to catch up on a conflict that’s been in flux since February of 2014. We often talk about people having short memories but don’t think that the Ukraine and Russia conflict just started last week. The point of our “letter to Mr. Market” today, however, is on what to do with your investments.

While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha. Resource and Energy Economics 41:103-121. Journal of Financial Economics.

While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha. Resource and Energy Economics 41:103-121. Journal of Financial Economics.

Although we expressed some worry about the long-term effects of mounting deficits, we concluded that stocks and other assets were not in bubble territory and represented good value despite what we saw as a weak economic recovery. It’s remarkable how far the markets have come in the five years since then. Then and Now.

We still like Energy this year and that is especially so with it being one of the most beaten down economic sectors from 2023. We’ve been pounding the table for holding Gold for several years now starting with our first nibble at it in 2014. 5 seed Targa Resources ( TRGP ) knocks out #11 Charter Communications ( CHTR ).

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. In short, every situation is different.

Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. Investment Perspectives - The Great Debate. Wed, 06/21/2017 - 12:35. In short, every situation is different. 1 [link] AssetFlows/AssetFlowsJan2017.pdf

And so, you know, I went to David and Bill in 2014, and we had kind of served out our three-year term there. But they also owned an asset management platform, so they had institutional distribution and the ability to raise capital from third parties globally. You raised another $11 billion in capital, despite the economic environment.

And that was his boss, Jeffrey Gundlock, founder of Double Line Capital, back in July, 2014. The very first Masters in Business that was broadcast just about 10 years ago, July, 2014, episode number one, Jeffrey Gundlock, DoubleLine Capital. And so I worked a lot on the assetallocation side. They got here a little late.

Behavioral economics provides insight into both surveys and modern polling errors). Highly dependent on precise phrasing of questions That’s just about basic market, economic, and assetallocation questions. The reason is that Sentiment measures suffer from problems similar to political polling. Backwards looking 2.

Neil Dutta has been doing economic analysis and research from a market-based perspective for over 20 years. I found this to be just an absolutely fascinating discussion about how to best contextualize the world of economic data around you, in a way that’s useful for you as an investor. With no further ado, RenMac’s Neil Dutta.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content