This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In particular, we see strong potential for companies that are well-positioned to serve members of the growing middle class in emerging economies, many of whom will be accessing a variety of services, such as banking and other financialservices, for the first time (see chart below).

In particular, we see strong potential for companies that are well-positioned to serve members of the growing middle class in emerging economies, many of whom will be accessing a variety of services, such as banking and other financialservices, for the first time (see chart below). .

We entered the liquid alts market with hedge funds back in 1994, and we entered the private market in 2014 with my product in late stage growth. We should consider doing a dedicated fund to take advantage of this trend for our clients. So fixed income is now a substantial percentage of our assets. When did you join Wellington?

Embedding ESG considerations into our investment analysis not only helps to shield our clients from business risks that can easily be ignored in the capitalist pursuit of profits, but also helps us invest in companies where we see the potential for a triple win—for the customer, the company and society or the environment.

Embedding ESG considerations into our investment analysis not only helps to shield our clients from business risks that can easily be ignored in the capitalist pursuit of profits, but also helps us invest in companies where we see the potential for a triple win—for the customer, the company and society or the environment.

Investment Perspectives | Real Returns achen Fri, 07/01/2016 - 06:00 One of the most penetrating and recurring questions we receive from clients is, “what is a reasonable long-term expectation for U.S. Private clients typically find themselves in a similar position, although they may not describe it in the same terms.

One of the most penetrating and recurring questions we receive from clients is, “what is a reasonable long-term expectation for U.S. Since equities typically comprise the largest single component of a balanced portfolio, they are the greatest single determinant of overall returns for institutional and private clients alike.

It suspended trading and filed for bankruptcy in February 2014, announcing that hundreds of thousands of bitcoins had been lost and likely stolen.2. The UK Financial Conduct Authority cited a number of concerns as it prohibited the sale of “cryptoasset” investment products to retail investors last year.

As the price of oil began to drop in 2014, investors in highyield credit grew increasingly concerned about default risk among energy companies. From June 2014 until February 2016, the oil price plunged 75%.) This piece is intended solely for our clients and prospective clients and is for informational purposes only.

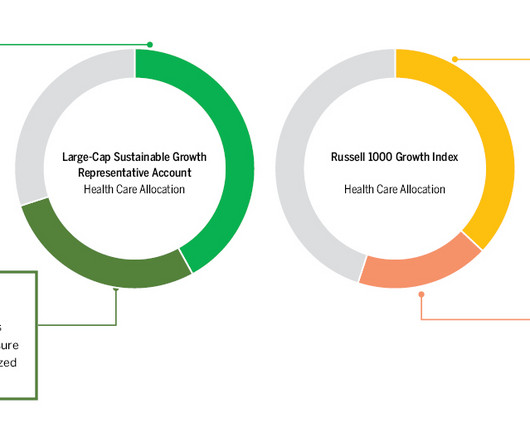

Account vs. Russell 1000 Growth Index 9/30/2014–9/30/2019 (Index=100) Source: Bloomberg. Average Health Care Subsector Weightings and Gross Returns, Five-Year Lookback (9/30/2014-9/30/2019) Source: Bloomberg. Global Industry Classification Standard (GICS®) and “GICS” are service makers/trademarks of MSCI and Standard & Poor’s.

As the price of oil began to drop in 2014, investors in highyield credit grew increasingly concerned about default risk among energy companies. From June 2014 until February 2016, the oil price plunged 75%.). This piece is intended solely for our clients and prospective clients and is for informational purposes only.

Account vs. Russell 1000 Growth Index 9/30/2014–9/30/2019 (Index=100). Average Health Care Subsector Weightings and Gross Returns, Five-Year Lookback (9/30/2014-9/30/2019). Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s FinancialServices LLC (“S&P”), a subsidiary of S&P Global Inc.

Thus, we consistently maintained a reduced weighting in European equities in the years since the crisis (relative to the blended benchmarks typically used by our clients to measure portfolio results). Currencies: Our analysis shows that between 1978 and 2014, currency movement explained 50% of the U.S. stocks growing more expensive.

Thus, we consistently maintained a reduced weighting in European equities in the years since the crisis (relative to the blended benchmarks typically used by our clients to measure portfolio results). Currencies: Our analysis shows that between 1978 and 2014, currency movement explained 50% of the U.S. stocks growing more expensive.

The background liquidity conditions for capital markets have changed substantively since the 2008-09 financial crisis, and to some extent these changes have contributed to the liquidity crunch in various segments of the market in the wake of the coronavirus outbreak. 10/15/2014 10-Yr U.S. Reference Market/Index % Change No.

The background liquidity conditions for capital markets have changed substantively since the 2008-09 financial crisis, and to some extent these changes have contributed to the liquidity crunch in various segments of the market in the wake of the coronavirus outbreak. 10/15/2014. Reference Market/Index. of Standard Deviations.

After joining the investment industry in 2001, he served as director of research at two firms, creating a small-cap growth strategy at one of them before joining Brown Advisory in 2014. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure.

After joining the investment industry in 2001, he served as director of research at two firms, creating a small-cap growth strategy at one of them before joining Brown Advisory in 2014. Criteria evaluated include market capitalization, financial viability, liquidity, public float, sector representation and corporate structure.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. In short, every situation is different.

Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. In short, indexing should be seen as part of the toolkit available for addressing a range of client objectives. The Role of Passive.

I first met Wes Gray, CEO/CIO of Alpha Architect in late 2014 and remember thinking, holy s**t, this guy rules. Wes has a great take on superior returns; "Sustainable alpha requires sustainable clients." A large swath of the financialservices industry would love to have you believe in their magic.

When I first launched “Masters in Business” in 2014, I spent a lot of time begging ( begging !) So when Brendan reached out and asked to come on to discuss behavioral finance and financial planning, I felt like paying it forward was the right way to go. guests to come on. There are over 20+ biases to pick from.

I mean, essentially what no one understood in the industry and still don’t understand today in the real estate industry is that when appraisers doing an appraisal for the buyer that’s getting a mortgage, their client is actually the bank. RITHOLTZ: Right, that’s right. MILLER: That they’re going to move their location.

As Morgan Housel has cautioned : “The business model of the majority of financialservices companies relies on exploiting the fears, emotions, and lack of intelligence of customers. 2014 : “What concerns us beyond valuations is the full ensemble of overvalued, overbought, overbullish conditions.”

Samantha Russell Reason to Follow: Advocate for digital marketing innovation for advisors Samantha Russell, Chief Evangelist at FMG Suite, is a pioneer in digital marketing for financial advisors. His signature sketches, creation of Behavior Gap , and podcast Kitces & Carl help advisors foster better client relationships.

So you can imagine that first check multiplied a little bit from 2014 or so. So I was very heavy in financialservices stock, which was a great lead gen engine. And I mentioned, you said it’s 2014. But, but for other people, we have, we have clients who’ve sold businesses. So we like to win.

What we try to do, of course, is to make sure we’re sending it out a little bit later than our clients get it, because then, you know, why pay for research in the first place if you can get it for free on Twitter. It doesn’t matter who the institutional client is, you would give him like an eight-second tee-up.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content