This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

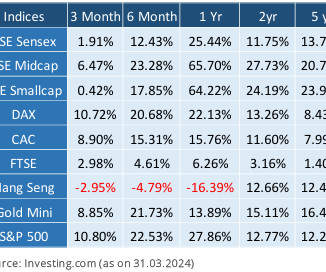

The major laggards were FMCG (down 6%), IT (down 2%) and financialservices (down 2%). Consequently, the portfolio allocation should reflect these probabilities depending on the risk profiles. Therefore, we maintain our underweight position to equity (check the Model Portfolio Current assetallocation below).

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. is much clearer.

Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. We maintain a model portfolio internally to track the results of our assetallocation stances. Thu, 06/01/2017 - 02:47.

As we will discuss in this article, we conduct climate-related research and analysis (as part of our overall research efforts) along several separate but integrated tracks to guide our assetallocation, manager research and portfolio construction efforts.

As we will discuss in this article, we conduct climate-related research and analysis (as part of our overall research efforts) along several separate but integrated tracks to guide our assetallocation, manager research and portfolio construction efforts. A 360-Degree Climate Evaluation. CARBON ATTRIBUTION” of SUSTAINABLE PORTFOLIOS .

A December 2017 working paper of the National Bureau of Economic Research examines the rates of return between 1870 and 2015 in several asset classes across 16 developed economies. It’s important to note here that we’re not recommending wholesale changes in assetallocation.

A December 2017 working paper of the National Bureau of Economic Research examines the rates of return between 1870 and 2015 in several asset classes across 16 developed economies. In attempting to reduce portfolio risk by shifting assets from equities to bonds, it’s important to recognize that bonds carry risks of their own.

Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” 3/18/2015 U.S. 8/24/2015 S&P 500 Index -5.0 Essentially, liquidity refers to how quickly an investment can be turned into cash. Treasuries -15.0

Consider how we defined investment risk in our 2018 assetallocation publication, Confronting the Unknown: “The probability that a portfolio will not meet an investor’s needs.” 8/24/2015. Liquidity, like many concepts in the investment world, is simple on the surface but becomes far more complex when one examines it more deeply.

As Morgan Housel has cautioned : “The business model of the majority of financialservices companies relies on exploiting the fears, emotions, and lack of intelligence of customers. 2015 : “Exit now.” .” Real fear comes with names, faces, and a story. And oh how we want deliverance from our fears.

But, yeah, I mean, you know, we started that account maybe in 2015. But again, it’s one of these interesting things, Barry, where if you look at like consumer confidence, it got very good after 2015 and particularly when we had the windfall from the positive supply shock in energy. Yeah, we’ve been growing it ever since.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content