This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

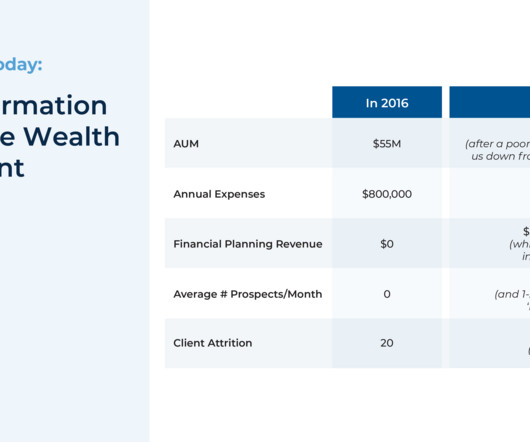

But as market trends changed (with the performance of this asset class falling behind large-cap stocks during the 2010s) and clients entered retirement (often consolidating their investment management with 1 advisor), Eliot Rose started losing clients, eventually becoming unprofitable in 2016, the year Jason became president of the firm.

Low Stakes : The most successful market timers are often those people who do not have actual assets at risk. When you get it wrong, it crushes your retirementplans. The less it matters, the easier it is to be bold and outside of the mainstream.4 4 Newsletter writers are notorious for making big calls.

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risk tolerance. At the very least wait until the dust settles.

Quoted in a Wall Street Journal article before the 2016 game, respected Wall Street analyst Robert Stoval said, “There is no intellectual backing for this sort of thing, except that it works.”. Perhaps it’s time to rebalance and to rethink your ongoing asset allocation. Some notable misses for the indicator include: St.

Both are multi-asset but PRPFX obviously allocates to precious metals and where you see the two funds diverge, those divergences coincide with big moves in gold. Then from about 2013 to 2016, gold struggled and so too did PRPFX. The ten year numbers are awful for PRPFX because gold went down for about 4 years from 2013-2016.

Two primary goals of the IRA were to provide a tax-advantaged retirementplan to employees of businesses that were unable to provide a pension plan; in addition, to provide a vehicle for preserving tax-deferred status of qualified planassets at employment termination (rollovers). Approximately 27.3

In 2016, it’s widely expected that the 2017 tax laws will revert. Business owners may be able to accelerate tax-deferred savings even more through different retirementplan structures. Asset location means utilizing the tax treatment of different investment accounts to your advantage when investing across your portfolio.

I stumbled into an old podcast from Resolve Asset Management that looked at the lack of differentiation from most factors and how to seek out "orthogonality" to get better diversification. In the 11 full and partial years we can see that Portfolio 2 lagged by a lot in 2016 and 2020.

Anytime I talk about letting markets work for you over the long term and the role that an adequate savings rate plays in financial success, I will usually caveat that with assuming a proper asset allocation. Gold was mostly in a downtrend from mid-2011 to early 2016.

As 2015 comes to a close, we remind our clients and friends of how important it is take time to review new tax rules, consider tax-saving opportunities and review investment and asset-protection plans before year’s end. Shift income into the more advantageous tax year. tax bracket.

Economist Roger Ibbotson and his team at Zebra Capital Management ran hypothetical return simulations from the years 1927 to 2016, which included both rising and falling yields. to 2016, a 60/40 stocks and bonds portfolio returned 7.6%, on average. Make your income-producing assets produce income and let your growth assets grow.

It's not quite as plain vanilla as mixing the S&P 500 and the Agg, there's more to it and the targeted notional allocations appear to be 75% to each asset using equity ETFs and bond futures. NFDIX has struggled since its inception and Yahoo shows it has having one star from Morningstar. The benchmark is 60/40 remember so 55.5%

The catalyst for this post is a research paper from ReSolve Asset Management that looks at a whole much of different equity factors in search of optimization. There was some sort of market event in Sept/Oct 2016 where low volatility funds went down quite a bit more than MCW, but again that was only a month and half.

The Catalyst/Aspect Enhanced Multi-Asset Fund (CASIX) just started trading at the start of the year. It seems to take a page from client/personal holding Standpoint Multi-Asset (BLNDX) by layering managed futures on top of, in this case, a passive 60/40 portfolio. I would also note that managed futures did worse in 2016 than 2018.

Yeah, that lot that talks about terms like compounding, risk profile, returns, retirementplanning, budgeting, Investing, and whatnot! The asset management company charges a fee in the form of an expense ratio to compensate them. He was associated with UTI AMC (Jul 2006-Sep 2016) as a fund manager, prior to joining IDFC AMC.

Back to Israelov's quote, they can be a way to add volatility as an asset class, in this case through something that sells that asset class, that sells volatility. Saying covered call funds are hormetic might be a stretch but you get the idea. They also do usually add quite a bit of yield.

The ETF allocates 25% each to equities and fixed income, 35% to trend and 15% to real assets. The Cambria website reports performance from Nov 2016-March 2024. In addition to the Cambria Trinity ETF (TRTY) there are six versions that as best as I can tell are separately managed accounts (SMA) offered through Betterment.

equity funds in 2016 alone. Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e.,

equity funds in 2016 alone. Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e.,

This number becomes concerning because the 2016 Consumer Finance Survey points out that approximately two-thirds of all households with young children have no savings. You can list your directives in the will, allocate the assets, assign guardianship for your child, specify rights, mention the power of attorney, etc.

OTRFX had a phenomenal 2020, it also had a strong 2016 and settled in with the pack the rest of the time. He's a big believer in Risk Parity which weights asset classes based on their risk which usually results in leveraging up the bond position. Here's how they've done compared to the iShares 3-7 Year Treasury ETF (IEI).

In 2016, SPY was up 12%, managed futures as measured by EBSIX was down 11% and an RSST replication using the two would have been flat which is what I mean by kneecapping upcapture. If you know me well, you might push back and ask why I own Standpoint Multi-Asset Fund (BLNDX), what the difference between it and the ReturnStacked suite?

Mon, 01/04/2016 - 13:57. To a certain extent, the Federal Reserve’s zero-rate monetary policy has fueled the flow of money into higher-risk asset classes, since “safe” assets have been priced to yield only meager returns. Investment Perspectives | Unicorns: Beyond the Myth.

Midyear Planning Tools for 2016. Thu, 06/16/2016 - 15:22. Yet despite a heavy dose of recent market volatility, the planning environment in 2016 is relatively stable. Yet despite a heavy dose of recent market volatility, the planning environment in 2016 is relatively stable. Presidential election.

The main takeaways are that one, 60/40 is not dead and that two, different assets have different durations. He works through a little theory coming with equities being an 18 year asset and bonds being a 5 year asset. Cullen Roche looked at the 60/40 portfolio concept through an interesting lens. Additionally on this point.

The simplest example would be the person to retired at the end of 2007 and then 12 months later, the stock market was 39% lower. With a cash buffer of two years or whatever, that sort of decline doesn't have to derail anyone's retirementplan. That person would be in some trouble without a cash buffer.

2016 Year-End Planning Letter. Sat, 11/19/2016 - 15:45. . However, the current policy environment remains relatively steady, at least through the end of 2016. As we noted in our midyear letter, it is helpful to build long-term plans on a foundation of stable, incremental yearly steps. Key Planning Notes for 2017.

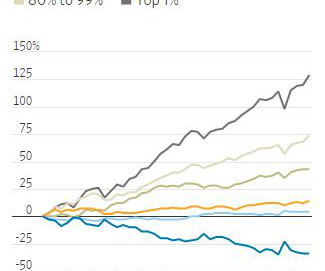

More Benefits , Binyamin Applebaum writes: The average worker received 32 percent of total compensation in benefits including bonuses, paid leave and company contributions to insurance and retirementplans in the second quarter of 2018. By 2016, the top 10 percent took 48 percent. That was up from 27 percent in 2000.Even

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content