This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Previously : The Timing Mistake: Thoughts & Pushback (August 26, 2020) Market Timing for Fun & Profit (August 28, 2020) The Art of Calling a Market Top (October 4, 2017) DOs and DONTs of Market Crashes (January 16, 2016) The Truth About Market Timing (March 13, 2013) Timing the Market? By Jeff Sommer New York Times, Nov.

Hendrik Bessembinder An excellent piece from Bloomberg came out over the weekend, The Math Behind Futility , which looks beyond the usual explanations as to why the majority of professional stock pickers fail to keep up with an index. In 2016, the average S&P 500 stock returned 1.5 down to 2.9%.

You would offer three of their stock picks where they were probably touting stocks they wanted to unload from their portfolio. But the numbers you can’t argue with, I mean, we all know that the brutal math of investing before costs investors collectively will earn the market return after costs. That’s exactly right.

00:03:14 [Mike Greene] So that was actually an outgrowth from my experience coming out of Wharton and you mentioned the, the, you know, the transition of people who tended to be skilled at math or physics into finance. Initially I joined to help them manage their equity portfolio. It was the exact same trade.

They are a publicly traded investment manager, stocks symbol DHIL, that have been public since day one since 2016. All of their portfolio managers not only are substantial investors in each of their funds, but they do a disclosure year that shows each manager by name and how much money they have invested in their own fund.

Part of the math that determines options premiums is the risk free rate of return from T-bills. We've also looked at countless ways to incorporate a small allocation to covered calls funds to help reduce portfolio volatility, so using them as alts in a matter of speaking. Covered call funds have many favorable attributes.

Notably, between 2000 and 2016, U.S.-based STEM (science, technology, engineering and math) funding is steadily declining—a dynamic that potentially opens the door for China to gain ground on the AI innovation front. has commanded the majority of AI activity over the past two decades. Sharpened by both the U.S.

Notably, between 2000 and 2016, U.S.-based STEM (science, technology, engineering and math) funding is steadily declining—a dynamic that potentially opens the door for China to gain ground on the AI innovation front. has commanded the majority of AI activity over the past two decades. Sharpened by both the U.S.

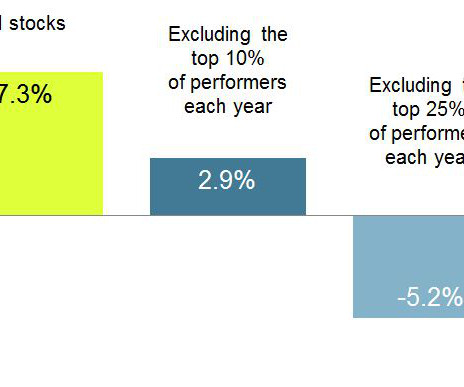

Based on the above, nobody should be surprised that 2022 looks like it will be the worst year for the classic 60:40 portfolio since 1937’s -22 percent. Wes created a hypothetical stock portfolio constructed with perfect foresight, invested entirely in the top decile of stocks based on their performance over the upcoming five years.

ANAT ADMATI, PROFESSOR OF FIANCE AND ECONOMICS, STANFORD GRADUATE SCHOOL OF BUSINESS: So, my journey starts where I took a lot of math. I was good in math and I love the math. So, I was kind of, in my romantic mind when I was in my early 20s, I was going to take but not give back to math, that kind of thing. ADMATI: Yes.

One of our colleagues, Ken Stuzin, likens portfolio construction to Darwinian Investing – it is about survival of the fittest. In a concentrated portfolio, it is the losers that kill you. What sort of hit rate should we then expect within their portfolio? 5 As Table 2 below highlights, this team appears to be seriously good!

BRYANT: So money, unlike math, money is highly emotional. I mean, there’s 50,000 kids in the Atlanta public school system, so you can do the math there. I believe I love math because it doesn’t have an opinion, that’s a Melody Hobson quote. RITHOLTZ: Right. BRYANT: Number two, money is emotional. RITHOLTZ: Yes.

That’s a really easy portfolio to create. It allows you to understand, generally speaking, what is a reasonable beta for that whole portfolio. By the time I got there in ’92, they had a great venture portfolio and almost nobody else even understood what venture capital was. That allows you to do two things.

And we wanted to, I really wanted them to move beyond the blog at, at, when I got to Barstool in 2016, it was, it was predominantly a blog operation. So I can remember going to, to Facebook, I write about this in the book when I was, you know, 2016, I had a meeting with Facebook that somebody gave to me as a favor.

I look for people that have done extracurricular work, or you know, manage their own little portfolio, or have stock ideas or businesses ideas that they want to pitch. SHAW: My wife and I decided to move to Tennessee back in 2016. RITHOLTZ: Why is it not surprising that a math nerd is also a placekicker? RITHOLTZ: Right.

She was a partner and a portfolio manager at Canyon Capital, a firm that runs currently about $25 billion. Before that, 2016, the energy crisis, same. But it’s interesting that you really can pinpoint the difference in return because there’s this sort of impatient or overzealousness in trading your portfolio.

RITHOLTZ: So it’s different math then I need 100x winner versus 99? I don’t have — coming from a family business, we say we don’t have portfolio theory. We’ve never had a business — again, go out of business or not paying interest payment. And the question is, you know, how high we can build?

Because he was all sure he was a totally isolated math. So, so he’s brilliant at math. He goes to m i t to study, study physics and math. So brilliant enough so that sure, he goes to math camp in the summer and find, kind of finds his tribe. But in math camp, he’s not the best. And the Undoing project.

So this is the math that I applied. So think about this, do the math. LINDZON: If you return your cash in 2016, we returned some cash in Robinhood in 2016, very early, but say those LPs bought Bitcoin. LINDZON: But that math, if you really put it in a calculator … RITHOLTZ: Becomes a problem. RITHOLTZ: You do it.

That’s why the markets are much more of a mind game than a math game. And that’s why markets will always be exceedingly hard, even when the math seems easy or the future seems certain. Stop with the math.` Beyond the present lies imagination. And lots of surprises. that hasn’t yet arrived. Also interesting.

Though insurance produced an unusual underwriting loss in 2017, it provided $114 billion in investable float, which partially funds Berkshire’s $314 billion investment portfolio. Berkshire’s investment portfolio holds about $186 billion in equities and $118 billion in cash equivalents and bonds as of March 31, 2018.

Though insurance produced an unusual underwriting loss in 2017, it provided $114 billion in investable float, which partially funds Berkshire’s $314 billion investment portfolio. Berkshire’s investment portfolio holds about $186 billion in equities and $118 billion in cash equivalents and bonds as of March 31, 2018.

William Priest, chairman, co-chief investment officer, and a portfolio manager at TD Epoch, picked Meta (+66 percent), which handily beat the S&P 500, but his other four picks did not. When Sam Bankman-Fried was at Jane Street Capital (before he became famous for FTX and convicted of fraud), he built a system to get the 2016 U.S.

So, I did the math, 20 million times a hundred. So, let me just repeat the math. And so, again, I went through this simple math. The currency devalued by 75 percent and my portfolio, which was above $1 billion, went down 90 percent. And this had an unbelievably positive affect on the value of my portfolio.

Here’s something that pulls them apart, I’m going to give a simplified version of the best data I’m aware of on this, where people in the 2016 election who favored Trump or Clinton also had predictions about whether Trump or Clinton would win before the election. Let’s take Clinton voters. Are you aggressive?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content