This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

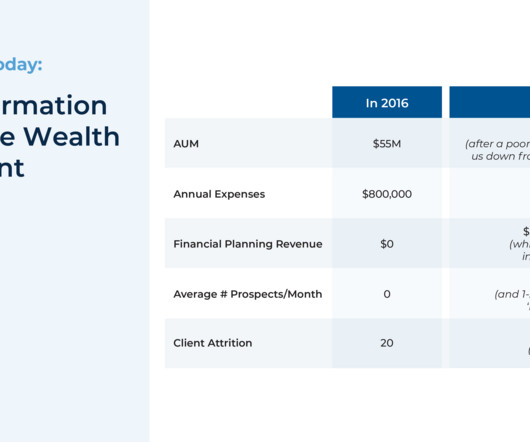

But as market trends changed (with the performance of this asset class falling behind large-cap stocks during the 2010s) and clients entered retirement (often consolidating their investment management with 1 advisor), Eliot Rose started losing clients, eventually becoming unprofitable in 2016, the year Jason became president of the firm.

Then from about 2013 to 2016, gold struggled and so too did PRPFX. The ten year numbers are awful for PRPFX because gold went down for about 4 years from 2013-2016. Here's how it did back to 2016. During the GFC and a little beyond, gold did very well and PRPFX outperformed by a mile.

In the 11 full and partial years we can see that Portfolio 2 lagged by a lot in 2016 and 2020. You can also see a long run from 2016 to 2021 where it was pretty far behind 60/40. Those aren't big numbers so a portfolio that was 80% equities and 20% managed futures that year would have been down 5.4%. Ok, no big deal, it happens.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. In recent years, a number of states developed a sort of workaround for business owners to navigate the SALT cap. In 2016, it’s widely expected that the 2017 tax laws will revert.

Some fund had a very good year or even great and the 5 and 10 year numbers look very favorable compared to that fund's benchmark. If the outperformance from the one great year is strong enough, it will move the needle on all of the long term performance numbers. In 2016 though, MTUM lagged MCW by 700 basis points.

He didn't specify which of the two (I believe that is the correct number) funds that Hussman managed back then. For 20 years, holy cow, the numbers look great. The ten year numbers tell a much different story due, I think, to the fund's large allocation to gold. Gold was mostly in a downtrend from mid-2011 to early 2016.

The gross numbers aren't that far off but some of those drawdowns look like deathblows. It spent so much time running below Portfolio 2 because it lagged by a lot in 2016. I got a reply from @HMLCompounder who back tested 3X S&P to the cash index with the following result. Note, this is very much a theoretical conversation.

In this letter, we outline a number of tax-saving and other opportunities to consider before the close of the year. As we note in some of the suggestions that follow, there are a number of ways to accelerate or delay income that may make sense for you, depending on where your income sits relative to the various thresholds listed above.

The portfolio goes back to 2016 so it captures a lot of different market conditions including a couple of crashes for Bitcoin. If I change the date to start in 2018, the numbers get a little more interesting. The idea behind that is less as an isolated bet on asymmetry and more about the potential impact on portfolio stats.

The point is that the factor, in the above case it's low volatility, has generally kept up with market cap weighting (MCW) with only 80% of the drawdown (his number). There was some sort of market event in Sept/Oct 2016 where low volatility funds went down quite a bit more than MCW, but again that was only a month and half.

If it can generate that sort of total return which is yet to be proven, and if, I say if, it delivers that sort of number with less volatility than the broad market then its attractiveness improves. The WisdomTree PutWrite Strategy Fund (PUTW) has a much different implementation of the strategy and the numbers aren't great.

I would also note that managed futures did worse in 2016 than 2018. There's probably a number in the 40-60% range in RSSY, the rest in cash, to see whether my theory will turn out to be right or wrong. Where RSSY is levered up 100/100, I don't think the correct comparison is putting everything into RSSY versus 100% into VBAIX.

Also, this number is exclusive of college expenses, which are now averaging $54,880 annually for private schools and $26,820 for public schools. This number becomes concerning because the 2016 Consumer Finance Survey points out that approximately two-thirds of all households with young children have no savings.

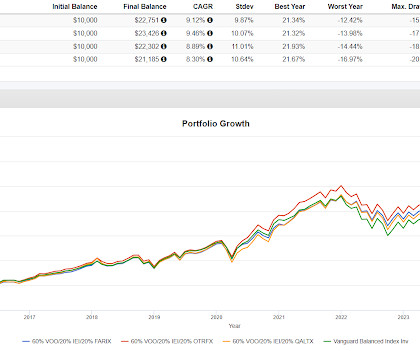

The six year numbers benefit from going down much less in 2022. An obvious flaw in the replication we did is that it is just a snapshot based on what the Natixis portfolio looks like today, the portfolio suite goes back to 2016. It is of course much simpler than the Natixis Portfolio.

Mon, 01/04/2016 - 13:57. In 2013, she applied it to the small number of privately held companies with a market value over $1 billion to denote their rarity. Demand for initial public offerings, while declining in number this year, has also facilitated exits at favorable prices. This is also where unicorns fit in.

OTRFX had a phenomenal 2020, it also had a strong 2016 and settled in with the pack the rest of the time. The Calmar Ratios are good for all of them but the kurtosis numbers are not which is a strike against relying on them as low vol, total bond replacements. Here's how they've done compared to the iShares 3-7 Year Treasury ETF (IEI).

equity funds in 2016 alone. The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common.

equity funds in 2016 alone. The term “active share” measures the degree to which a portfolio’s holdings differ from those of its benchmark, taking into account the number of stocks in the portfolio but not in the index and the difference in weightings of those stocks held in common. Assuring "Average".

Midyear Planning Tools for 2016. Thu, 06/16/2016 - 15:22. Yet despite a heavy dose of recent market volatility, the planning environment in 2016 is relatively stable. Yet despite a heavy dose of recent market volatility, the planning environment in 2016 is relatively stable. Planning Tool: GRAT.

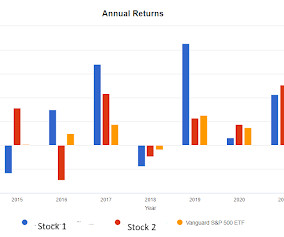

Being able to sit in a name when it is lagging, like the blue bar in 2015 or the red bar in 2016, requires a lot of patience but that patience is more easily found when you think in terms of stocks being long duration assets regardless of whether 18 years is the right number or not. Additionally on this point.

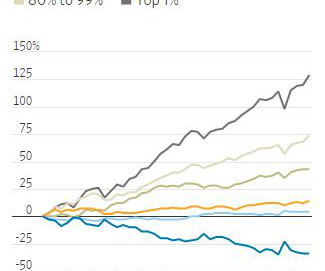

The Bloomberg article included a couple of quotes about dialing down the equity exposure in retirement which has been the default approach but that chart shows why dialing down is a bad idea. The simplest example would be the person to retired at the end of 2007 and then 12 months later, the stock market was 39% lower.

These numbers are so incomprehensibly large that they lack any meaning. From February 2013 to November 2016, there were 3.6 The median retirement account balance of people ages 56 to 61 is just $25,000. Things are (obviously) tough for low-income earners In 2016, 2.2 It's like saying that Pluto is 4.67 The top 0.1%

2016 Year-End Planning Letter. Sat, 11/19/2016 - 15:45. . However, the current policy environment remains relatively steady, at least through the end of 2016. As we noted in our midyear letter, it is helpful to build long-term plans on a foundation of stable, incremental yearly steps. Takeaways.

These numbers are very easy to manipulate depending on what story you want to tell Standards of living are much higher today than they were in 1972 What about benefits that don't show up in wages? By 2016, the top 10 percent took 48 percent. For example: Is the average American better off today than they were four decades ago?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content