This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Previously, he served terms on the FSP National Board of Directors from 2011 through 2016. He is the author of several books, including Free Throws for Financial Professionals: Winning Principles for Unlocking Business Success, Above the Clouds: Winning Strategies from 30,000 Feet, and The New Rules of RetirementPlanning.

As owners of financial planning firms approach retirement, some may decide to sell to an external buyer, while others may plan for an internal succession. Sometimes, this succession plan can include the owner's child, providing an opportunity to keep the business in the family.

When you get it wrong, it crushes your retirementplans. My own track record at making big calls is pretty damned good, but none of our clients wants me slinging around their retirement monies based on my gut instinct. The less it matters, the easier it is to be bold and outside of the mainstream.4

Assuming that you have a financial plan with an investment strategy in place there is really nothing to do at this point. Ideally you’ve been rebalancing your portfolio along the way and your asset allocation is largely in line with your plan and your risk tolerance. If not perhaps you are taking more risk than you had planned.

Quoted in a Wall Street Journal article before the 2016 game, respected Wall Street analyst Robert Stoval said, “There is no intellectual backing for this sort of thing, except that it works.”. Related Posts: Five Things to do During a Stock Market Correction Is a $100,000 Per Year Retirement Doable? Take stock of where you are.

Two primary goals of the IRA were to provide a tax-advantaged retirementplan to employees of businesses that were unable to provide a pension plan; in addition, to provide a vehicle for preserving tax-deferred status of qualified plan assets at employment termination (rollovers). billion in the first year (1975).

Meeting with your clients outside of the office and getting them engaged with your community planning is crucial for establishing strong relationships. Whether retirementplanning, technology seminars, or education planning, community events are an efficient way to share your experience with others in your community.

Strategic Advisory Letter | 2015 Year-End Planning Checklist. As 2015 comes to a close, we remind our clients and friends of how important it is take time to review new tax rules, consider tax-saving opportunities and review investment and asset-protection plans before year’s end. Thu, 11/12/2015 - 11:10. tax bracket.

In 2016, it’s widely expected that the 2017 tax laws will revert. Tax planning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in tax planning, it’s important not to let the tax-tail wag the dog. Bonus depreciation was as high as 100% at one point.

Then from about 2013 to 2016, gold struggled and so too did PRPFX. The ten year numbers are awful for PRPFX because gold went down for about 4 years from 2013-2016. Here's how it did back to 2016. During the GFC and a little beyond, gold did very well and PRPFX outperformed by a mile.

Instead, they start piling up right when you plan to conceive. While the figure is stressful, financial planning for a baby can help you transition into parenthood smoothly. Here are some tips that can help you in planning for a baby financially: 1. This can shield you from having to take out loans or depleted savings.

The article shows being updated in 2016 but not by me, the URL has the 2004 time stamp. I wrote an article for Motley Fool in May of 2004 saying I didn't want to own the stock and spelled out why. Since then, the stock appears to actually be down.21 21 years later and it's down?

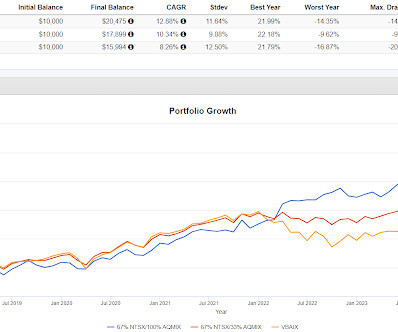

In the 11 full and partial years we can see that Portfolio 2 lagged by a lot in 2016 and 2020. You can also see a long run from 2016 to 2021 where it was pretty far behind 60/40. It also avoids interest rate risk and what I've been calling unreliable volatility from longer duration fixed income.

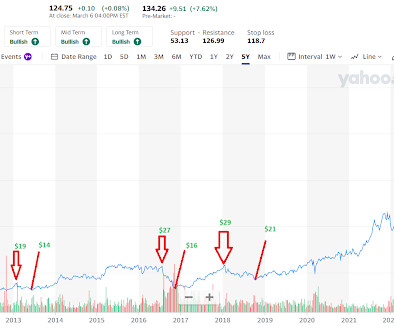

Dropping from $27 down to $16 like in 2016 is a very difficult thing to sit through. I added in price levels of a few peaks along with subsequent declines. There are plenty more than the few I drew into the chart but want to make a simple point about how difficult holding a stock can be. Sometimes the thesis does change and you should sell.

This goes back to 2016 to GBTC's apparent inception. In reading about this, what I think they do is allocate an even 20% to stocks, income (bonds), volatility, trend and gold/crypto. Here's the starting point. Here are the results.

It spent so much time running below Portfolio 2 because it lagged by a lot in 2016. Portfolio 1 outperformed in 6 of the 9 years studied with slightly less volatility. Portfolio 1 didn't really provide much cover in 2022 though because HCMDX was down 39% that year. compared to 7.35, had a standard deviation of 8.07 versus 10.32

Economist Roger Ibbotson and his team at Zebra Capital Management ran hypothetical return simulations from the years 1927 to 2016, which included both rising and falling yields. to 2016, a 60/40 stocks and bonds portfolio returned 7.6%, on average. A balanced retirement portfolio should have growth assets and income-producing assets.

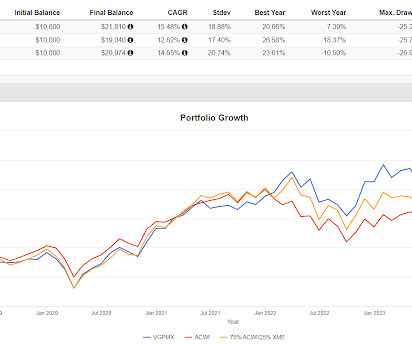

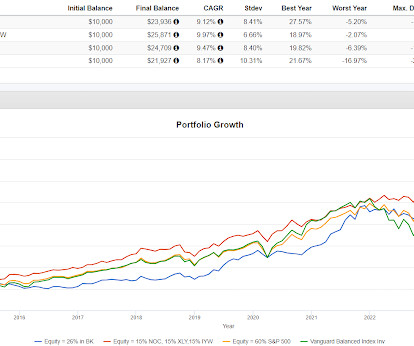

XME fell 50% in 2015 and then made it all back with a 106% gain in 2016. Blending 25% in with ACWI helped in 2022 but otherwise it's not much different than 100% in ACWI. I really am surprised this doesn't create an easily observed differentiated return stream.

John Authors at Bloomberg goes into better detail including a reference to the Bernstein paper from 2016 that likened indexing to Marxism. There has long been a sentiment that believes indexing is dumb money. If you are an indexer then this should not be the first time your hearing that.

The portfolio goes back to 2016 so it captures a lot of different market conditions including a couple of crashes for Bitcoin. Here's the first iteration, note that I usually talk about a 1% allocation to Bitcoin, realizing it could go to zero but I decided to use a 2% weighting for this post. And the results.

In 2016 though, MTUM lagged MCW by 700 basis points. Switching from MCW to SCHD now, after a great year is an example of chasing last year's winner that I have mentioned before. A more glaring example might be with iShares US Momentum ETF (MTUM). In 2015 it was up 8.93% versus 1.25 In 2020 MTUM was up 29.85% versus 18.37 percentage points.

There was some sort of market event in Sept/Oct 2016 where low volatility funds went down quite a bit more than MCW, but again that was only a month and half. During the 2020 Pandemic Crash, SPLV did a little worse than the S&P 500 and USMV did only slightly better but neither offered protection.

Gold was mostly in a downtrend from mid-2011 to early 2016. If you target 65% in equities via a simple equity index fund, then that fund will get the CAGRs you see above (or close to it).

Yeah, that lot that talks about terms like compounding, risk profile, returns, retirementplanning, budgeting, Investing, and whatnot! A Systematic Investment Plan (SIP) is an investment route offered by mutual funds, wherein multiple investors invest a fixed amount of money at regular intervals, say monthly or quarterly.

It lagged SPY in the up year of 2016 when it lagged by 130 basis points. In 10 full years plus an 11th partial year for 2022 it outperformed in six of those years. The lag in 2015 was a matter of basis points. The worst full year was 2018 when it was down 5.74% vs 4.55% for SPY and 2.82% for VBAIX.

Building a plan based on assuming an 11% payout forever is really going to hurt this guy if that is what he is saying. The way circuit breakers work has made a 1987 one day 20% crash almost impossible (it would play out differently) but a repeat of the Flash Crash of 2011 or 2016 would probably smack the hell out of QQQY.

The sizable outperformance of tech stocks between 2016 and 2021 created valuations that, in many respects, may not be sustainable in the current interest rate environment. The outsized influence of tech company earnings on the S&P 500 is important to understand.

Portfoliovisualizer has its CAGR at 3.44% going back to 2016 and comparing it to a 100% allocation to NTSX since NTSX' inception shows a CAGR of 2.32% versus 12.42 NFDIX has struggled since its inception and Yahoo shows it has having one star from Morningstar.

They deviated in 2022 for the better and also in 2016 when they all lagged VBAIX. BTAL is sort of anti-trend because it shorts high beta. The three versions in this backtest look like VBAIX almost all the time which is ok, VBAIX works almost all the time.

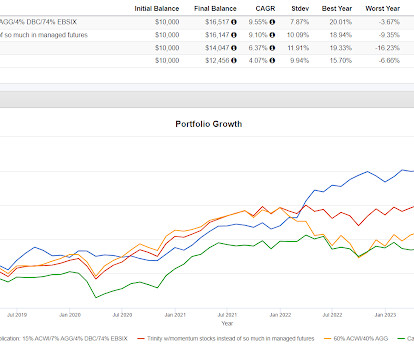

According to the Trinity performance data , from Nov 2016-March-2024, Trinity 3 compounded at 5.08% with a standard deviation of 8.61% and a max drawdown of 15.59%. Ok, it smooths out the ride but I think there are way to get a similar volatility profile but with a little more upcapture, using Trinity's allocation weightings.

The Cambria website reports performance from Nov 2016-March 2024. The second portfolio being near the top for the entire back test makes sense due to having 55% in equities. The portfolio I labeled as Trinity w/Momentum stocks used Trinity 4 as a starting point.

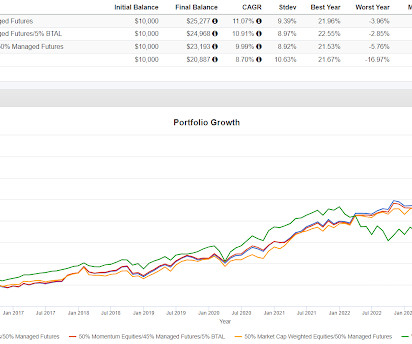

I would also note that managed futures did worse in 2016 than 2018. There's a good chance of getting essentially the same effect with much less risk of being vulnerable to something breaking or at least bending a lot like managed futures in 2018.

When we talk about allocating a lot to simplicity and hedging with a little complexity, it is important for anyone needing normal stock market growth for their plan to work to have plain equity exposure. Whatever allocation to equities they think they need, most of it should be in very simple, very plain holdings.

It lagged badly in 2016, 2019 and 2021. It had a big edge in 2020, which was probably also from Bitcoin. It held up better in 2022 which makes sense because it owns a bunch of stuff that is not equities or bonds. The other day I asked whether you could hang in with a portfolio that lagged badly the first year you implemented it.

An obvious flaw in the replication we did is that it is just a snapshot based on what the Natixis portfolio looks like today, the portfolio suite goes back to 2016. It is of course much simpler than the Natixis Portfolio. Anyone so interested could track it going forward though by closely following their page.

OTRFX had a phenomenal 2020, it also had a strong 2016 and settled in with the pack the rest of the time. Here's how they've done compared to the iShares 3-7 Year Treasury ETF (IEI). Here's the year by year with 2022 highlighted.

There is a mutual fund version with symbol ENHNX that goes back to 2016. DIVP looks like it owns value stocks that pay a growing dividend and sells call options. The ETF just started trading in March. The mutual fund website compares the fund to the CBOE BuyWrite Index.

equity funds in 2016 alone. We understand and appreciate this approach, which is particularly common among endowments, foundations and retirementplans for which tax considerations are not relevant. According to Morningstar (which tracks mutual funds and their performance), more than 80% of all actively managed U.S.

equity funds in 2016 alone. We understand and appreciate this approach, which is particularly common among endowments, foundations and retirementplans for which tax considerations are not relevant. According to Morningstar (which tracks mutual funds and their performance), more than 80% of all actively managed U.S.

Mon, 01/04/2016 - 13:57. Institutions, of course, represent the interests of millions of individual investors, whether through mutual funds, retirementplans, insurance companies or other investment accounts. Investment Perspectives | Unicorns: Beyond the Myth.

Midyear Planning Tools for 2016. Thu, 06/16/2016 - 15:22. Yet despite a heavy dose of recent market volatility, the planning environment in 2016 is relatively stable. Yet despite a heavy dose of recent market volatility, the planning environment in 2016 is relatively stable. Presidential election.

Plan participants ages 50 and older have a contribution limit of $7,500, which is commonly referred to as the “catch-up contribution.”. Rollovers: You can roll over money from a traditional IRA or another employer-sponsored retirementplan into a Roth IRA, but you may have to pay taxes on the amount rolled over.

Flow Financial Planning blogged about something it calls Coast FIRE. It's a play on FIRE which stands for financial independence/retire early. We've looked at this quite a few times favoring the idea of achieving some measure of financial independence but not so much actually retiring early. More quick hits.

With a cash buffer of two years or whatever, that sort of decline doesn't have to derail anyone's retirementplan. Looking year by year, portfolios 1 and 2 lagged by a lot in 2016, outperformed by a lot in 2022 (by going down much less) and 2023. That person would be in some trouble without a cash buffer.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content