This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This week, we speak with Elizabeth Burton , managing director and client investment strategist at Goldman Sachs Asset Management. She was named to CIO Magazone’s “40-Under-40” (2017) and received the Industry Innovation Award/Power 100 in 2019.

Throughout 2017, our meetings and conversations with clients very frequently focused on the topic of risk. While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Fri, 03/30/2018 - 11:57.

The “5% rule” was instituted in 1981 by the IRS; this rule requires private foundations to distribute at least 5% of portfolio assets each year, and over time this rule has been voluntarily adopted by nonprofits of all types. Each “shoestring” curve represents the expected outcomes for various allocation targets, assuming a given spend rate.

The “5% rule” was instituted in 1981 by the IRS; this rule requires private foundations to distribute at least 5% of portfolio assets each year, and over time this rule has been voluntarily adopted by nonprofits of all types. Each “shoestring” curve represents the expected outcomes for various allocation targets, assuming a given spend rate.

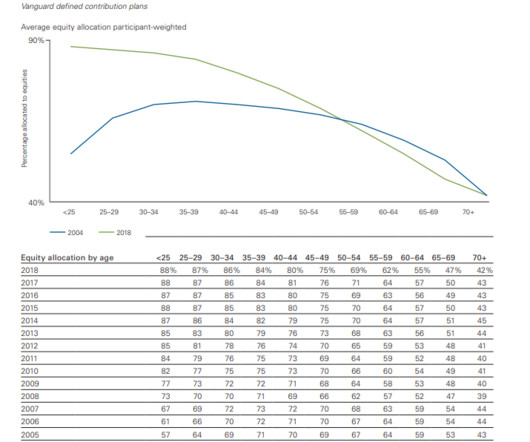

trillion in assets. They anticipate that by 2023 80% of all assets at Vanguard will be in an automatic investment program. There has been a pretty steep drop-off in participation for people under 25 years old, from 57% in 2014 to 38% in 2017. Vanguard is out with a new monster research report called How America Saves.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. stocks growing more expensive.

Thu, 06/01/2017 - 02:47. Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. We maintain a model portfolio internally to track the results of our assetallocation stances.

It's more like, the assetallocation idea is interesting, is there a way to get close? When tinkering with these things, don't be afraid to have a normal-ish allocation to equities. 25% in stocks means having to get a lot of growth out of other asset classes that probably not as growthy.

In this brief paper, we will touch on what we believe are some of the most important issues and questions—including the different types of assets, return potential, fees, liquidity, diversification, volatility and transparency—that investment committees must understand as they weigh adding alternatives to their portfolios. Source: BLOOMBERG.

In this brief paper, we will touch on what we believe are some of the most important issues and questions—including the different types of assets, return potential, fees, liquidity, diversification, volatility and transparency—that investment committees must understand as they weigh adding alternatives to their portfolios. Source: BLOOMBERG.

according to a 2017 survey by the American Council on Gift Annuities (ACGA), more than 4,000 nonprofit institutions offered CGA options to their donor bases. However, the management of underlying assets in a gift annuity pool is a different matter. CGAs are a fairly common option in the U.S.—according Treasury bonds), and 5% cash.

according to a 2017 survey by the American Council on Gift Annuities (ACGA), more than 4,000 nonprofit institutions offered CGA options to their donor bases. However, the management of underlying assets in a gift annuity pool is a different matter. The desired variability in the asset to liability ratio.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

Incremental Equity Risks Several evolving dynamics in the stock market, when taken together, suggest that risk levels have increased a bit over the last year or so: Valuations: To state the obvious, stock prices gained considerable ground during 2017 and are slightly higher so far in 2018. Concentration: Much of the U.S.

Several evolving dynamics in the stock market, when taken together, suggest that risk levels have increased a bit over the last year or so: Valuations: To state the obvious, stock prices gained considerable ground during 2017 and are slightly higher so far in 2018. Concentration: Much of the U.S. Risks in Bonds.

Starting Points achen Tue, 03/28/2017 - 14:11 The numbers tell a clear story about the growing number of investors interested in sustainable investing. Initial steps such as these can minimize disruption and help investors grow comfortable with values-based investing.

Tue, 03/28/2017 - 14:11. Assets in investments aligned to environmental, social or governance factors increased nearly fivefold between 2012 and 2016, according to US SIF Foundation. . . Starting Points. The numbers tell a clear story about the growing number of investors interested in sustainable investing.

At Carson Investment Research, we have moved our longer-term strategic assetallocations to their maximum equity overweight while continuing to favor U.S. The average return over rolling five-year periods from 1923 through 2017 is about 11% (before inflation). Here’s why.

An important tool in this regard is diversification, or spreading risk across various asset classes and investment opportunities, each of which has a different return profile. Like any other asset class, of course, bonds carry risks that must be managed in line with client objectives. While current economic conditions in the U.S.

An important tool in this regard is diversification, or spreading risk across various asset classes and investment opportunities, each of which has a different return profile. Like any other asset class, of course, bonds carry risks that must be managed in line with client objectives. While current economic conditions in the U.S.

But the drop in valuations experienced at year’s end, alongside higher bond yields, offer a foundation for better long-term return expectations across most asset classes. During both of these events, asset prices became disconnected from reasonable estimates of intrinsic value. and Canada.

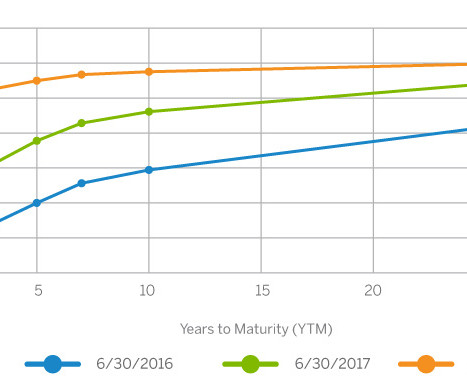

The most egregious example appears to be in 2015 (green line) when the Committee expected interest rates in 2017 to be above 3.5%, when in actuality they were closer to 0.50% that year. References to markets, asset classes, and sectors are generally regarding the corresponding market index.

ESG and the Stock-Picker’s Dilemma achen Fri, 09/22/2017 - 12:58 One of the greatest challenges that public equities investors face to integrating environmental, social, and governance (ESG) data into their decision making is the lack of proof that real – not hypothetical – investment strategies can use ESG factors to enhance performance.

Fri, 09/22/2017 - 12:58. This work builds on the Capital Asset Pricing Model developed in the 1960s.) Research firms lack standardization on the ESG issues they cover and the systems they use to quantify those issues into a score or rating for a company (Bose and Springsteel, 2017). ESG and the Stock-Picker’s Dilemma.

There never was a more docile and boring year than 2017. Our article that we linked to above followed the least volatile year in the history of the stock market. Read that sentence again if you must but for some context just let it sink in. Not one single month was down and there was zero volatility. Then… all hell broke loose in 2018.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. In our view, it’s not a question of whether , but under what circumstances.

Wed, 06/21/2017 - 12:35. Generally, index fund fees are low because management costs are minimal (investment judgment is not required to track an index) and administrative expenses are typically spread over a large asset base. are there better or worse moments in time to enact an indexing strategy) and choice of asset class (i.e.,

The transcript from this week’s, MiB: Mike Greene, Simplify Asset Management , is below. We have to pay attention to this, and we have to understand why this is potentially a risky asset. In that trade on a monthly basis, when you run that full strength, it gives the dynamics of something like the XIV, which rose 600% in 2017, right?

Diversification involves investing in a variety of asset classes, such as stocks, bonds, and cash, to spread out the risk and reduce the impact of market volatility. Rebalance their portfolio : Individuals should regularly rebalance their portfolio to maintain the desired assetallocation and minimize the risks.

We break down and assign each of the four “regions” with an asset class and then pick teams (stocks) that we think have the best chance at doing well relative to others. Betting on the right asset class or area of the world is usually going to bode better for you and also avoids having a collection of stocks that one has to follow.

By Doug Grim The single best day for the S&P 500 in 2017 was a rise of just 1.38 By Dina Isola Assetallocation explains 93.6% By Nick Maggiulli We believe there is an opportunity here, but we’re probably wrong By Corey Hoffstein Relative underperformance of sizable length and high degree, is actually quite normal.

Investment Perspectives | “Undoing” the Fed’s Balance Sheet achen Tue, 11/14/2017 - 16:18 These days, it seems like all eyes are on the Federal Reserve. As short-term interest rates on low-risk assets approached zero during the crisis, conventional monetary policy became ineffective at encouraging investment and stimulating the economy.

Tue, 11/14/2017 - 16:18. While this shift in monetary policy may ultimately have important implications for assetallocation and other investment decisions, we’re not convinced that its near-term impact will be particularly significant. By 2014, when QE officially ended, assets on the Fed’s balance sheet totaled $4.3

Mathieu Chabran is the co-founder of TIKEHAU Capital, a Paris-based alternative asset manager. They run over $40 billion worth of assets. I don’t know how relevant that is to asset management, but let’s talk a little bit about you were doing before you were being lauded by the French president. Well guess what?

In June 2017, Dent predicted a “ once in a lifetime ” crash in the stock market, the economy, and in real estate over the following three years. who became a professor at the University of Michigan before setting up his own asset management firm. 2017 : “[T]he most broadly overvalued moment in market history.”

Outlook for 2017 | Balance in an Uncertain Time achen Fri, 02/03/2017 - 14:19 With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. Provide our assetallocation perspective as it stands at the beginning of 2017—also based on a longer-term view.

Outlook for 2017 | Balance in an Uncertain Time. Fri, 02/03/2017 - 14:19. With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. Provide our assetallocation perspective as it stands at the beginning of 2017—also based on a longer-term view.

And if you look at the s and p today, 50% of it is asset light, innovation oriented healthcare and tech. Whereas in 1980, 70% of it was manufacturing asset intensive, et cetera. So, 00:44:55 [Speaker Changed] So well let me ask you a question about that asset light side. It’s a changing animal.

And it’s funny ’cause that was a pandemic purchase, a very inexpensive 2017 Panama four s, which everybody walked away. He wasn’t tactical assetallocator. It’s about long-term planning and strategic assetallocation and, and just understanding how markets work and how behavior comes into the mix.

We were talking about luck earlier, got introduced to a local asset manager outside of Boston who saw what I was working on and said, this is really interesting. And so as those assets grew, I’m now a young 20-year-old going out trying to go to other asset managers saying, Hey, I have this quantitative research.

What was the big — RITHOLTZ: 2017. And you know, the Fed can play a role in sort of backtracking sentiment in the short run, but the Fed can’t permanently increase the level of asset values. and so many different asset classes, and so many different types of constituents that they serve, right? DUTTA: Yeah.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content